Total spending grew 0.9% in June.

Risk off again overnight as recession fears intensify

https://soundcloud.com/user-291029717/freaking-out-over-inflation?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

Overview Barely Breathing

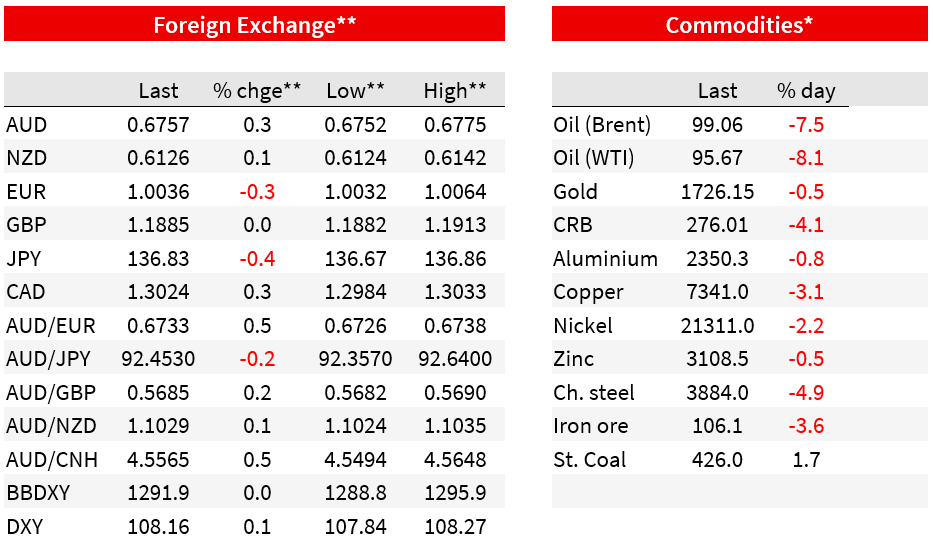

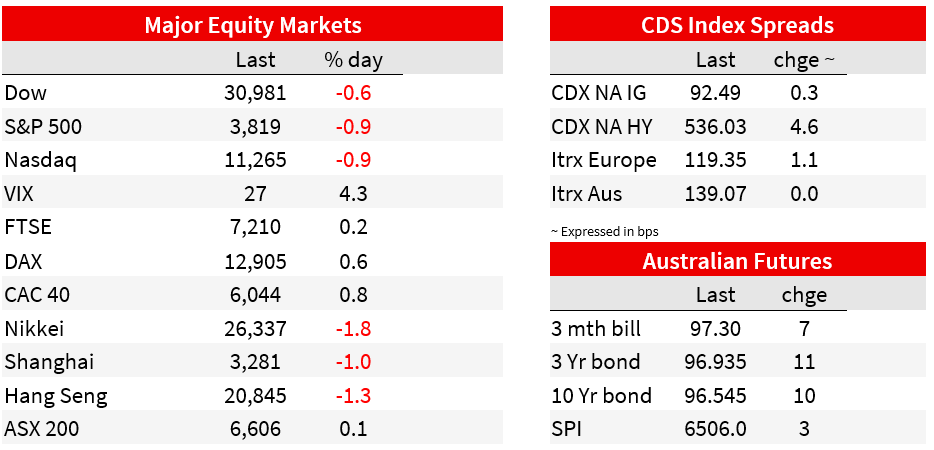

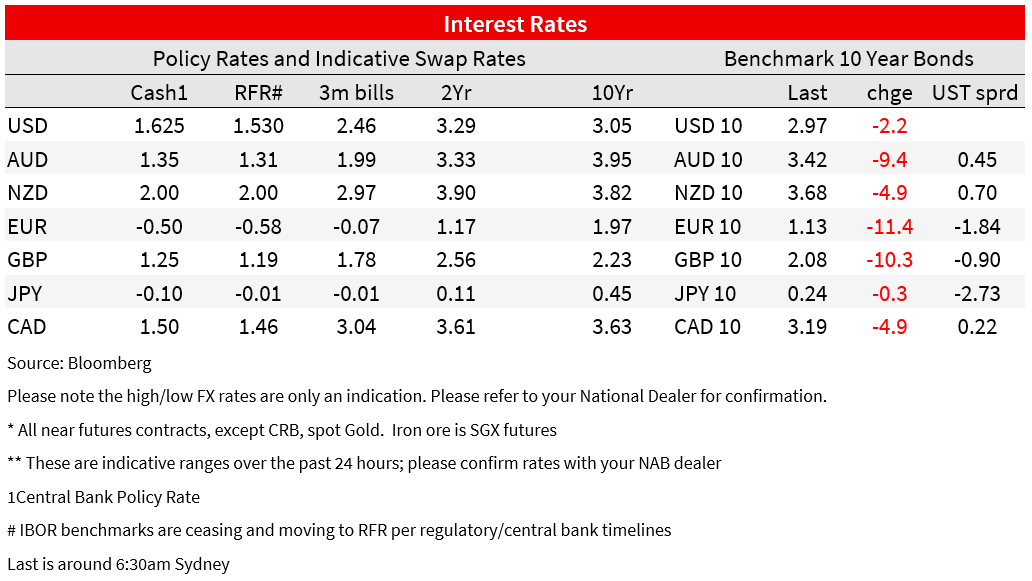

Risk off again overnight as recession fears intensify. US equities fell in volatile trade with the S&P500 -0.9%, reversing earlier gains of 0.5% near the open. Oil plunged with the front contract for Brent -7.4% to $99.21. Bonds rallied hard in Europe with the German 10yr Bund -11.4bp 1.13%, to be at its lowest level since the end of May and now down some 80bps from its recent peak. Across the pond US 10yr yields did hit a low of 2.89%, but retraced to be only down ‑2.2bps to 2.97%. Curve inversion in 2/10s remains at -8.1bps, while a surge in 3m bill yields of 15bps has seen the 3m/10yr flatten to a still positive 77bps. While economic data has been mostly second-tier, dire business surveys did exacerbate price action with the German ZEW Survey slumping to its lowest level since November 2011 (-53.8 vs. -40.5 expected). The main uncertainty for Europe steams around the Nord Stream gas pipeline and whether gas flows resume once the maintenance period ends on 21 July.

Given heightened uncertainty in Europe, EUR continues to come under pressure. The EUR came within a whisker of trading at parity with Bloomberg data suggesting it touched 1.00003 before rebounding, now about 1.0050 – evidently parity holding for now. Recession fears are greater in Germany than elsewhere, given the country’s reliance on Russian gas to fuel its industry. A prolonged cut to the gas supply would halt a lot of economic activity, sending the country deep into recession. Germany’s Economy Minister Habeck is worried Russia will find an excuse to impede gas flows once maintenance is completed. The date 21 July should be marked in everyone’s calendars. That date also happens to be the day of the next ECB meeting. Either of these events are key risk events. Russia playing gas politics by not switching on the gas supply would likely see the EUR lurch much lower while the ECB is expected to kick off a rate hike cycle with a 25bps hike and its forward guidance will be important.

Some acknowledgement of recession risk also came from the Fed overnight. The Fed’s Barkin (non-voter) noted “I definitely see signs of softening” with this most “pronounced in lower income households”. Still the US could skirt a downturn in a soft landing, but much of that came down to whether controlling inflation required “demand destruction ” as opposed to inflation easing as improvements in labour supply and lower global commodity prices feed through. Barkin also backed the Chair Powell for a 50-75bp hike at the July meeting. A Fed research paper out also discussed recession risk more openly, extrapolating the expected hike cycle to their ABC models and noting this would see a 35% chance of a recession in 2023, and if a restrictive stance of policy were to be in place in early 2023 a 60% chance of recession which is generally followed by a recession (see FEDS Note: Monetary Policy, Inflation Outlook, and Recession Probabilities).

Reflecting recession fears Brent oil prices have fallen by 7.4% with Brent now trading below $100 per barrel at $99.21 and WTI below $95.71. Also a factor is China’s growing COVID19 case numbers noted as possible causes. Meanwhile the physical oil market itself remains tight. OPEC published its first outlook for 2023 and noted that it expects global oil demand growth to exceed the increase in supplies by 1 million barrels a day. Separately, OPEC production data showed that the cartel’s output continued to run below target in June, at more than 1 million barrels per day, raising concerns about whether it is capable of increasing supply. Meanwhile Libya’s production continues to be interrupted amid ongoing domestic political tensions.

US data was second-tier with only the NFIB small business survey, while corporate earnings were positive. The index dropped to 89.5 against 92.5 expected, its lowest since January 2013, but is hard to interpret given its strong Republican bias. The index though does highlight growing anxiety and also helped feed recession fears. The earnings season also started (though the banks report later in the week) with PepsiCo reporting a better-than-expected quarterly profit and revenue and raising its revenue outlook for the year. American Airlines also said it expects total revenue in the second quarter to top 2019 levels with its stock up nearly 10%.

Finally, in FX the USD after hitting a fresh 20-year high of 108.5 last night, reversed course to end broadly unchanged with the EUR holding marginally above parity to currently trades at 1.0034 . Overall the supremacy of the USD is clear in this environment with Europe subject to gas woes, the UK in political turmoil, and in Japan the BoJ doesn’t look like it is shifting on YCC until its 2% inflation target is achieved. Speaking of Japan US Treasury Secretary Yellen suggested no appetite for currency intervention to prop up a weak yen saying that G7 countries should have market-determined exchange rates and “only in rare circumstances is intervention warranted and we did not discussion intervention”. A joint statement said that “we will continue to consult closely on exchange markets and cooperate as appropriate on currency issues”. The reversal in USD strength did see both the AUD (+0.3%) and NZD (+0.1%) after hitting lows of 0.6770 and 0.6153 respectively.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.