Confidence and Conditions Lift

Insight

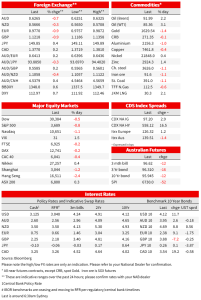

Yields rose to fresh cycle highs and risk appetite soured. US equities were lower, halting a 2-day rally despite relatively upbeat earnings from the likes of Netflix and United Airlines.

Yields rose to fresh cycle highs and risk appetite soured. US equities were lower, halting a 2-day rally despite relatively upbeat earnings from the likes of Netflix and United Airlines. Yields globally have pushed higher with the US 10yr yield up 12bp to 4.12%. UK and Canadian inflation data each surprised marginally on the high side of expectations.

The S&P500 was 0.7% lower. Energy was the only sector in the green, while declines were led by Real Estate and Financials. That’s despite reasonably upbeat earnings, including from Netflix jumped 12% after it said it gained 2.4 million new subscribers last quarter. European indexes were generally a little lower, though the Euro Stoxx 50 managed a 0.2% gain.

US rates pushed higher across the curve. The 2-year and 10-year Treasuries are both up 12bps to 4.55% and 4.12% respectively to fresh cycle highs and levels not seen since late 2007. Fed Fund futures have also continued to push higher and now peak at just under 5% in the first half of next year, up from expectations of 4.5% at the beginning of the month. The German 10yr was 9bp higher to 2.38%, the 2yr up 13bp to 2.08%, above 2% for the first time this cycle.

Not helping the cause for rates markets was hawkish commentary from the Fed’s Kashkari and ECB’s Vasle. Kashkari said that “if we don’t see progress in underlying inflation, or core inflation, I don’t see why I would advocate stopping at 4.5% or 4.75%, or something like that” suggesting that some evidence of relief in the inflation data would need to be in hand before pausing, even at levels of the policy rate that are restrictive. “ Core services inflation — which is the stickiest of all — keeps climbing, and we keep getting surprised on the upside” As for the ECB, Governing Council Member Vasle declared in favour of two more 75bp hikes over the remaining two meetings of this year. Markets are pricing high chance of 75bp from the ECB next week, with 73bp priced.

UK gilts were the exception to the global push higher in yields. 10yr guilts losing 7bp to trade at 3.98%. Deputy Governor Cunliffe testified to a parliamentary committee and noted that “the LDI episode I hope is behind us,” echoing comments made yesterday that LDI funds report they are better prepared for shocks. He said the October 31 fiscal statement will be important for the BoE Decision in November and he is confident of gilt market conditions to begin QT.

The outperformance of gilts came despite slightly hotter than expected UK inflation. UK inflation was 10.1% y/y in September from 9.9% in August and against expectations for a 10.0% rise. The monthly number was 0.5% vs 0.4% expected and the core rate rose to 6.5%y/y. Food inflation was again a large driver, up 1.1% in the month and 14.8% y/y. The September numbers are usually used for increasing benefits and pensions the following April. The data again highlights that before the mini-budget event, the BOE still had an inflation problem to deal with.

Canadian inflation data also provided no relief from a string of recent global inflation upside surprises , coming at 6.9% from 7.0% and against 6.7% expected. The monthly read came in at 0.1% m/m (-0.1% expected). A third consecutive month of fuel price decreases helped flatter the headline numbers. BoC governor Tiff Macklem said earlier this month that there was “more to be done” to cool inflation, given he has not seen “clear evidence” that underlying inflation had subsided. The data overnight certainly isn’t providing it.

In currency markets, the USD jumped 0.7% on the DXY and was higher against all G10 currencies. The AUD lost 0.7% to 0.6265 after hitting an intraday low of 0.6251. The CAD outperformed, though still lost 0.2% against the dollar, supported by the rates reaction to inflation data. Market pricing for next week’s BoC meeting moved 15bp higher, with 71bp now priced for October and a peak of 4.4% in March.

GBP was 0.9% lower, not helped by lower UK rates. UK politics are again in the headlines, with Home Secretary Braverman forced to quit after a security breach (using her personal email for official business) and chatter that other Cabinet Ministers may be looking to resign to force PM Truss to step down.

Finally on the yen, USD/JPY continues to push higher, edging closer to 150, up 0.4% to 149.85. The ever-lurking threat of official FX intervention perhaps slowing the pace we might otherwise have seen given higher global rates.

Confidence and Conditions Lift

Insight

Online retail sales growth slowed in May following a fairly strong April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.