Long-term signal vs. Short-term noise

Insight

Markets broadly held onto Tuesday’s wild moves, which were driven by US Fed Chair Powell’s Senate Testimony. Overnight Powell spoke again to the House.

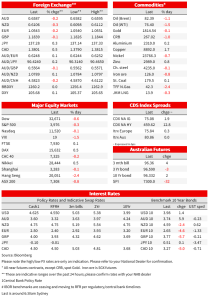

Markets broadly held onto Tuesday’s wild moves, which were driven by US Fed Chair Powell’s Senate Testimony. Overnight Powell spoke again to the House. There was one important change to that testimony, an ad lib to his opening remarks that were otherwise identical to Tuesday of: “I stress that no decision has been made on this ” in regards to how much interest rates could rise in March – payrolls and CPI being important here. While markets initially did react, moves have been largely unwound with yields broadly where they were in late Asia yesterday (e.g. US 2yr 5.06% and 10yr 3.98%). Data was second-tier, but strong with JOLTS (10824k vs. 10546k expected) and ADP Employment (242k vs. 200k expected) beating. Fed Funds pricing inched higher with a 50bp hike in March now 71% priced, up from 63% yesterday. While terminal is now pegged at 5.69%, up from 5.62% yesterday. US banks are now starting to call for a 50bp rise in March with Citigroup the latest. Equities have been choppy with the S&P500 currently trading -0.2% as we head into the close. The USD (DXY) has been little changed +0.1% at 105.65, so too most pairs; AUD -0.1% to 0.6587. Bucking the hawkishness, the BoC kept rates on hold as expected.

First to US Fed Chair Powell’s House Testimony. There was only one real change of substance and that was Powell emphasising the Fed was not pre-committed to a certain sized hike in March. Chair Powell inserted ad lib into his opening remarks that were otherwise identical to what he delivered to the Senate on Tuesday. Powell added “I stress that no decision has been made on this,”, and then continued with “but if the totality of the data were to indicate that faster tightening is warranted, we would be prepared to increase the pace of rate hikes.”. In testimony he also said payrolls and CPI are “going to be important in our assessment” however, “ we have not made any decision about the March meeting. We’re not on a pre-set path”. Importantly Powell continued with remarks saying that the Fed was likely to lift rates higher this year than previously expected. For your scribe the most important takeaway was the lack of pushback from Democrats on Fed rate hikes, suggestive of a still broad political consensus for rate hikes given the persistence of elevated inflation. Of course that also means greater risk of recession, and in this respect the 2/10s curve inverted further to -109.4bps (see WSJ: Jerome Powell Says Data Will Determine Size of Next Rate Increase).

Data flow was stronger than expected. ADP Employment was 242k vs. 200k expected, from 119k previously. ADP of course is far from infallible as far as payrolls on Friday where consensus sits at 225k. JOLTS were very strong with job openings 10.824m vs. 10.546k expected, and the prior month was also revised up to 11.234 from 11.012k. Taken as a share of unemployed, there still remains 1.9 job openings per unemployed person in the US, reflective of a still very tight labour market, and Chair Powell has previously said he wants this rate closer to 1. Within the details, openings did fall sharply in IT, construction and real-estate (the sectors where tighter policy is being felt), but rose in leisure-and-hospitality and retail, where consumer spending remains resilient. Layoffs did increase, but remained below pre-pandemic. Across the pond, European GDP growth was revised down a tenth in Q4 to 0.0% q/q from 0.1%, raising the prospect of a technical recession. German Retail Sales were also weak at -0.3% m/m against +2.3% expected, though Industrial production though was stronger (3.5% m/m vs 1.4% expected).

Bucking the hawkish rhetoric by the US Fed, the BoC kept rates on hold at 4½% as widely expected. The BoC though did keep the door open to further hikes if necessary. In the post-Meeting Statement the BoC noted that “the latest data remains in line with the Bank’s expectation that CPI inflation will come down to around 3% in the middle of this year. Year-over-year measures of core inflation ticked down to about 5%, and 3-month measures are around 3½%” (see BoC: Bank of Canada maintains policy rate, continues quantitative tightening ). The less hawkish rhetoric compared to the US Fed across the border, probably contributed to some CAD weakness with USD/CAD +0.5% to 1.3799. Markets continue to price the BoC moving again with 33bps of hikes priced by September, or around 1.3 x 25bp hikes. In FX in general it has been relatively quiet with the USD (DXY) up just 0.1%. Over the past 24 hours the AUD is -0.1% to 0.6590, ditto NZD -0.2% to 0.6110. As for the other majors: GBP -0.1% to 1.1841, EUR -0.2% to 1.0548, USD/Yen +0.3% to 137.25.

Finally in Australia, RBA Governor spoke at the AFR Business Summit yesterday. We wrote on this extensively yesterday, noting that NAB continues to see the RBA hiking in April and May. In Q&A, asked about the case for a pause next month, Governor Lowe had an open mind, and that if Employment, the Monthly CPI Indicator, Retail Sales, and Business Surveys collectively make the case for a pause “they will do that.” Given the RBA expects more tightening is necessary, our interpretation is the data flow would need to be a fair bit softer than expected to make that case. If employment rebounds as we expect, a hike is likely in April. And if CPI remains sticky as we think, another is likely in May. For your scribe, the more interesting bits where the emphasis that the RBA is still trying to achieve a soft landing and continues to place an emphasis on preserving gains in the labour market. To do this, the RBA is using the full flexibility in the inflation target, though if the RBA can’t forecast inflation getting to 3% by mid-2025 then the RBA would have to be more hawkish. This of course runs the risk of the RBA again falling behind the curve, and as well as that people thinking the inflation target has moved higher to 3% plus, instead of the 2-3% target (an inverse echo of Lowe’s ‘2 point something’ comments pre-pandemic which was cited by some as lowering inflation expectations in Australia).

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Long-term signal vs. Short-term noise

Insight

Join us as we discuss interest rates, general economic conditions, and the NAB AUD/USD forecast

Webinar

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.