Total spending grew 0.9% in June.

Risk aversion has dominated the start of the new week amid heighted geopolitical tensions and a market disillusioned by credible BoE support for the Gilts market.

Nothing of note

Risk aversion has dominated the start of the new week amid heighted geopolitical tensions and a market disillusioned by credible BoE support for the Gilts market. US equities have extended their decline for a fourth day, UK Gilts have led a sell off in core global bond yields with UST Futures suggesting 10y UST yields should reopen close to 4%. The USD is broadly stronger on safe-haven flows with a perfect storm hitting the AUD, as market catch up with the weak China economic news over the weekend plus news of new US semiconductor restrictions on China’ coupled with Russia’s retaliation after the Crimea bridge attack over the weekend.

The US has been on holidays (along with many countries in the Americas) Celebrating Columbus day. A US holiday is usually a recipe for a quite start to a new week for markets, but not the case this time. US equities market were open with the S&P 500 extending its decline by a fourth consecutive day, closing the day down 0.75% after trading down to an intraday low of 1.42% while the NASDAQ has closed -1.04% lower. Meanwhile in Europe the Stoxx 600 index closed down by 0.4% while yesterday China CSI 300 ended the day 2.21% lower.

The risk aversion in the air has not been helped by geopolitical tensions while comments from JP Morgan CEO Jamie Dimon have not helped sentiment in the US equity market either. Speaking to CNBC, Dimon said the US economy was actually still doing well, but warned a “very, very, serious” mix of headwinds was likely to tip the US and global economy into recession by the middle of next year, which is increasingly becoming the consensus view. Dimon added that the S&P500 could fall by “another easy 20%”.

After news over the weekend of an attack on a key bridge to Crimea that Russian President Vladimir Putin blamed on Ukraine, on Monday Russian forces hit Kyiv and other Ukrainian cities with missile strikes. President Putin also warned of a harsh response if Kyiv were to conduct further “terrorist attacks”. The Russia Ukraine war appears to be escalating with Ukrainian officials noting the strikes reflected Russia’s growing desperation as the war’s momentum shifts in Kyiv’s favour.

Overnight, sentiment has also not been helped by a big core global bond sell off led by UK Gilts, notwithstanding a flurry of announcements designed to calm UK debt markets . With the US out and yields there set to bounce sharply when the US reopens, it is notable that UK 10-yr yields closed up by 23 bps on the day to 4.47%, and at one point coming close to matching the 4.60% spike high seen on 27 Sep when the markets went into meltdown. As widely anticipated by media outlets, UK Chancellor Kwarteng announced that he would deliver a full set of economic and fiscal forecasts, alongside the Office for Budget Responsibility (OBR) independent forecasts on 31 October . This is a few weeks ahead of schedule and will allow the BoE to incorporate the forecasts into its 3rd of November policy decision.

Perhaps in anticipation of some volatility ahead of the end of its emergency Gilt buying facility, the BoE announced a series of measures presumably aimed at easing market concerns, although arguably details have disappointed. Early in the UK morning the BoE launch a temporary repo facility through to 10 November, advising that it would now allow a broad range of collateral including investment grade corporate bonds, to help banks/pension funds caught in an LDI liquidity trap to access funds. Rather than having to sell Gilts to raise cash for margin calls, these funds can pledge Gilt holdings rather than sell them. The BoE also said that it would increase the daily amounts it was willing to buy in long-dated bonds ( to £10bn from £5bn) before ending the program as scheduled on Friday.

When the BoE Gilt facility was announced late in September, UK Gilts yields plunged judging the BoE support as an effective tool, but yields have been rising in recent days after it became evident the Bank was buying far less than the £5 billion a day., a possible sign that the program wasn’t working as intended. The WSJ noted the BoE only bought £853 million of gilts on Monday. So, it seem that there has been a combination of disappointment among investors who had expected the BOE to extend the bond-buying facility while at the same time as one commentator noted, “There’s a message to pension funds and potential sellers that the window is closing and they need to hurry up.”.

Meanwhile in FX land, risk aversion has resulted in a USD bid supported by safe haven flows. USD indices are up around 0.2% with AUD and NZD leading the G10 declines against the greenback. For the AUD and NZD (to a lesser extent), the start of the new week has been something of a perfect storm. Both antipodean currencies are risk sensitive and highly sensitive to China economic fortunes. Chinese markets back from a week-long holiday had to catch up to the very weak Caixin Services/Composite PMI released on Saturday – (latter down to 48.5 from 53.0) plus news the Biden administration on Friday announcement of new restrictions on China’s access to US semiconductor technology. The yuan weakened even after the central bank maintained its support for the currency with a stronger- than-expected fixing for a 28th day, semiconductors share in Asia sold off with the Philadelphia Stock Exchange Semiconductor Index falling as much as 4.6%, building on Friday’s decline of 6.1%. The market now await retaliation from China.

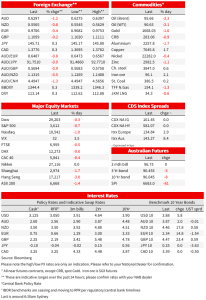

Overall, the combo geopolitical tensions and softer China economic data plus broad risk aversion has weighed on the AUD with the pair opening the new day below 63c ( down over 1% over the past 24 hours) while NZD is not far behind, down 0.8% to 0.5566.

Looking at other pairs, EUR and GBP are modestly weaker, trading at 0.9715 and 1.1070 respectively. USD/JPY is trading up to 145.7, close to the peak level seen in September ahead of the MoF currency intervention. After dusting off USD20b, the MoF will no doubt be ready to enter the market again when USD/JPY breaks up through 146.

NAB Markets Research Disclaimer

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.