Price growth edges lower despite reasonable economy

Insight

Eurozone PMIs spring upside surprise, supporting EUR and holding USD in check

https://soundcloud.com/user-291029717/happy-tales-from-euroland?in=user-291029717/sets/the-morning-call

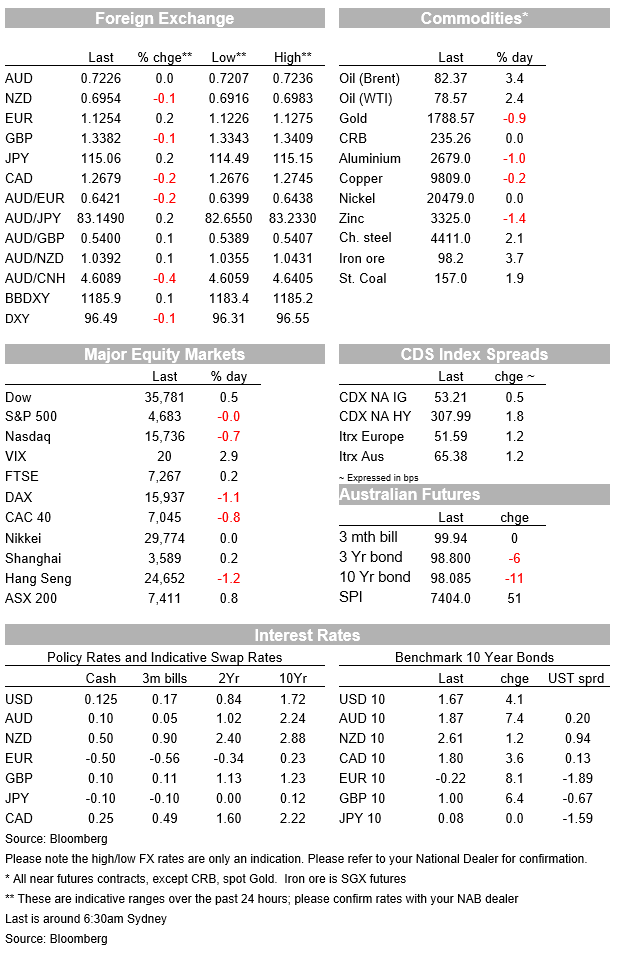

In contrast to the US where incoming November Markit PMIs were either unchanged (Manufacturing) or fell (Services) Eurozone PMIs were stronger than expected across the board , and in all case bar German manufacturing, up on October. This has helped steady the EUR/USD rate and in doing so kept the (DXY) USD rise in check, unchanged on Monday’s NY close at 96.5. 10-year bond yields are up again in the US (US 10s by 3.6bps though 2s are down by 2.6bps) and even more so in Europe, weighing heavily on the NASDAQ (-1.0%) but less so on the S&P 500 (-0.3%) while Covid-19 developments across northern Europe have hurt European stocks (Eurostoxx 50 -1.3%). The VIX is around 20 and if it closes above, this will be the first time in almost six weeks. The RBNZ is at midday AEST, where the local money market ascribes a 34% chance to a 50bp rise in the OCR.

In yesterday’s missive, we played up the likelihood of further divergence in the direction of travel of US versus Eurozone PMIs as prone to add further fuel to the USD rally, on top of the support drawn from the latest rise in US bond yields, some of which attributable to the news that President Biden was reappointing Jay Powell to a second term as Fed chair. Well, the facts got in the way of that particular story, with incoming Eurozone PMIs displaying unexpected resilience or outright strength, summarised in the pan-Eurozone Services PMI printing 56.6 up from 54.6 last time (53.5 expected) and for Manufacturing 58.6 from 58.3 (57.4 expected). The only individual reading down on October was for German manufacturing (57.6 from 57.8) but this was still better than expected and a very healthy level in absolute terms, so no signs as yet of a big hit from China’s slowdown on German export demand.

The bottom line is that Eurozone economies are for the most part dealing with ongoing supply chain disruptions and rising covid infection rates much better than earlier in late 2020 and earlier this year, though it has to be said that these surveys will have been taken prior to the announcement of Austria’s full lockdown and what lies ahead for other Eurozone economies, including Germany (and where, for example, most Christmas market have now been closed).

The equivalent US PMIs – less influential than the ISM surveys it has to be said – were either weaker than expected and down on October (Services 57.0 from 58.4) or up but no more than expected (manufacturing 59.1 from 58.4). In other US economic news the Richmond Fed Manufacturing index slipped to 11 from 12, as expected.

The Eurozone PMIs data helped lift the EUR/USD exchange rate from around 1.1240 to 1.1275, though the move was also supported by comments from ECB Executive Board member Isabel Schnabel, who said EZ inflation risks were skew to the upside and that the ECB shouldn’t pre-commit on policy over too long a time span, albeit she said it wa plausible inflation would be below 2% in the medium term. Later, ECB Governing Council member Klaus Kno t told Bloomberg TV he didn’t see lockdowns as altering plans for winding down ECB stimulus and that while he doesn’t see a rate rise until after 2022, current supply shocks may not be short lived and that if the market is right on inflation, it’s also right on rates.

The EUR’s modest revival has held the DXY USD index in check around 96.5, while with the exception of SEK (-0.6%) G10 currency movements elsewhere has been modest, ranging from 0.15% for NOK to -0.2% for GBP (if you want excitement in currency markets right now, look no further than the Turkish Lira, which fell another 12.5% yesterday to bring its month to date loss to 35%. This as President Erdogan continues to defend the CBTs rate cuts (on his edict) and to equate high inflation to high interest rates.

NOK outperformance in G10 FX comes on a day where the US announced release of 50 million barrels of oil from the US Strategic Petroleum Reserve, together with smaller releases from China, Japan and Korea (totalling perhaps 15-20 million barrels). This has seen Brent crude futures just settle for the day at $82.31, up 3.3% or $2.61. The release, widely expected, is the proverbial drop in a bucket (amounting to about 16 hours’ worth of daily crude oil consumption, which currently runs at close at 100 million barrels a day, and might just lead OPEC+ producers to scale back a bit on what they were planning to pump.

The other commodity mover of note in the last 24-hours has been iron ore , where futures in China and Singapore went ‘limit up’ (~5%) yesterday on hopes that easing of curbs of China property developers, rising margins for steel producers, and signs that the China’s authorities are, or are about to, add some fiscal and monetary support to the broader economy, will add to demand for steel making inputs. Impact on the AUD? Zilch, and here we note that the day-today correlations between iron ore prices and the AUD is very often zero, or even negative, albeit the sharp fall in iron ore in the first half of November clearly had a hand in the fall back in AUD/USD from above 0.75.

GBP is an underperformer overnight, -0.2% despite mixed but slightly better than expected UK PMIs (Services 58.6 from 59.1, manufacturing 58.2 from 57.8) while the BoE’s Haskel, seen to be a dove on the MPC, said that he’s concerned about second round effects of current high inflation and that rates would have to increase if the jobs market remained tight, but that he wanted to wait to normalize rates until the recovery was entrenched. Note there is one more jobs report before the BoE MPC’s next meeting in December.

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.