Online retail sales growth slowed in May following a fairly strong April

Insight

The US has been out for Veterans Day, though stock markets have been open and have recouped a little of their pre and post US CPI losses

https://soundcloud.com/user-291029717/have-a-little-faith?in=user-291029717/sets/the-morning-call

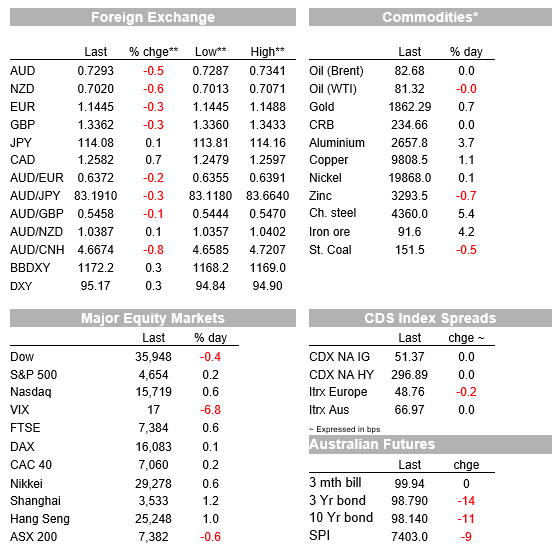

The US has been out for Veterans Day, though stock markets have been open and have recouped a little of their pre and post US CPI losses, the S&P currently +0.2% and the NASDAQ +0.7%, the latter despite the more acute interest rate sensitivity of the tech/growth sector and where Treasury futures – which have been trading – have seen implied 10-year yields lift a little further (3-4bps) on top of the big post-CPI jump. European stocks were mostly higher Thursday but not by much, following gains for most APAC bourses yesterday. The more interesting moves overnight have been in currencies and commodities , which have each gone their own way in so far as commodities are mostly higher – and some very smartly so – while commodity currencies have underperformed, not just against a strengthening USD but against all other G10 currencies.

The improvement in sentiment after the earlier US CPI-hit looks to owe something to developments in China and where, incidentally, the conclusion of yesterday’s sixth CCP plenum saw President Xi Jinping deliver the first ‘doctrine’ on Communist Party history by a Chinese leader in 40 years, giving him a mandate to potentially rule for life. The Central Committee called on the country to “unite around the party with Xi at the core,” implement his doctrine to strive for party goals set through 2049 and realize “the great rejuvenation of the Chinese nation,” the communique said, according to the Xinhua news agency Getting the group of 400 mostly male party elites, including state leaders, military chiefs, provincial bosses and top academics, to endorse his vision sends a strong signal Xi has the power base to clinch a precedent-defying third term next year (Bloomberg reporting).

Of more immediate market relevance have been reports (Wall Street Journal) that Chinese authorities are taking some steps to support the real estate market, including allowing firms in the sector to raise funds in the Chinese interbank market and are considering easing the rules to let struggling developers sell off assets to avoid defaults and hits to the broader economy. The WSJ says that the PBoC is considering opening a pathway for financially strained property firms to unload projects by allowing the buyers, likely state-owned firms, to take over the assets without having the projects’ associated debt affect their own debt ratios. Together with news that Evergrande had made a $148.1m of coupon payments on two USD bonds over the past few days, just before the end of the 30-day grace period, commodity prices have had a very good Thursday. This includes aluminium up 3.7%, copper +1.1%, Singapore iron ore futures +4.2% and steel futures +5.4%.

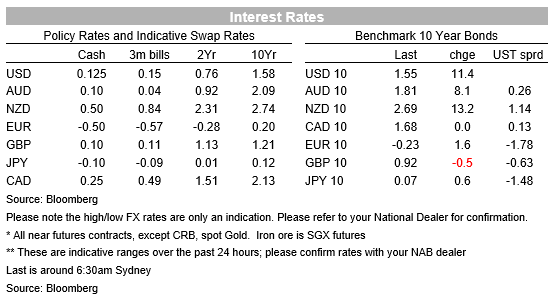

Higher commodity prices have evidently been of no help whatsoever to commodity-linked currencies, with AUD (-0.5%), NZD (-0.7%) and CAD (-0.8%) siting firmly at the bottom the G10 scoreboard , with losses for other currencies more in the 0.2-0.3% range. Here, we probably needn’t look behind the extension of the USD’s post-CPI spurt higher, and which sees the DXY index up though 95 (high of 95.2) for the first time since last July last year. In NAB’s FX Strategy team’s FX forecast revisions last month we lifted out near term USD outlook to have DXY at 95 by year-end (and AUD/USD at 0.72), revisions that are currently looking quite prescient; but there is a lot of water to flow under the bridge between now and then, so premature to call victory just yet.

In other currency news, the SNB’s Andrea Maechler has just been out saying that the CHF remains high and that it is always prepared to use FX intervention, but perhaps more telling, she says that while price pressures in Switzerland ‘remain modest’, a strong Franc helps dampen inflation. This suggests more tolerance of prevailing EUR/CHF level in the current 1.05-1.06 level (which is pretty much where we have it through the next couple of years, as per the aforementioned recent FX forecast revisions).

The main economic news overnight has been UK Q3 (and September monthly) GDP . GDP grew by 13% on the quarter after the 5.5% re-opening bounce, a little shy of the 1.5% consensus forecast. September alone at +0.6% was a little stronger than the 0.4% expected, but this was offset by a 0.2% downward revision to August (to 0.2%). So the level pretty much as expected at the start of the December quarter, though the detail of the Q3 report show consumption and investment both somewhat undershot expectations. GBP was a touch weaker after the report, while 10-year gilt yields were 0.2bps lower, in contrast to gains across the rest of Europe averaging 1-2bps.

Yesterday’s Australian Labour Force Survey shows employment falling, by 46k, against expectations for a rise, while unemployment also rose 0.6 points to 5.2% from 4.6%, above the 4.8% consensus. Our economist argue more positive numbers will come next month, given stay at home orders were lifted from mid-October (NSW 11 October; ACT 15 October; VIC 21 October). Encouragingly there were signs of improvement ahead of the easing of restrictions with the participation rate lifting 0.1 to 64.7% as more people actively searched for work, while employment rose in NSW (+22k) as firms prepared for re-opening. Note the headline decline in employment was driven by VIC (-50k). Underpinning our expectations of a sharp rebound in employment is that the level of people who are ‘attached to a job’ has been little changed during the most recent lockdowns (-0.2% non-seasonally adjusted), despite the sharp falls in employment (-2.3%).

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.