Coming in for landing in a heavy cross wind

Insight

Hawkish comments from ECB’s Holzmann send European yields higher in an otherwise quiet night for news flow

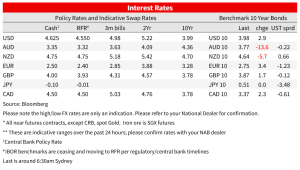

Contrasting perspectives from ECB speakers were the main news in an otherwise quiet start to the week. German yields were higher, boosted by comments by Austria’s Holzmann that restrictive rates for the euro area start at 4%. His colleague, Chief Economist Lane, was less strident, warning against policymakers being on ‘autopilot’.

European core yields were higher across the curve . German 2yr bund yields were 10bp higher to 3.30%, while the 10 yr was up just 3bp to 2.74%, though after reversing an earlier rally down to 2.64% intraday alongside the move higher in short end yields. That was also reflected in market pricing for the ECB, which now sees 159bp of further hikes this year, from 151bp at the end of last week. There is now a 70% chance of a follow up 50bp increase in May priced in, with the peak in the deposit rate now priced at 4.08%.

With 50bp well-signalled and well-priced for next week, focus is on the path for rates from there. ECB commentary highlighted the difference of opinion, but comments from hawk Holzmann were the ones getting market attention. He assumes that core inflation will remain around its current level through the first half of the year, and in that case expects “we’ll hike rates by half a percentage point four more times this year.” Holzmann said that only at 4% “would we roughly get into the restrictive area. ” That messaging contrasted less hawkish comments from chief economist Lane, who highlight the cumulative impact of hikes that have already occurred and that while current information suggests further hikes beyond March, “Exactly what we do in May will be very data dependent.” Meanwhile, Portugal’s Centeno highlighted that headline inflation was undershooting the ECB’s forecasts and that officials should not rush to conclusions on other gauges, like the higher core inflation data.

US yields reversed course after heading lower into the early European session. The US 10yr yield dipped below 3.9% before rising back to 3.97%, up 2bp on the day. Focus now turns to Fed Chair Powell in front of the Senate Banking Panel tonight from 2am Sydney time and the House Financial Service Committee tomorrow night.

In currency markets, higher European rates have helped the euro to the top of the G10 leader board on the day. The euro was 0.4% higher to 1.0676. That helped the USD down 0.2% on the DXY, though the US dollar gained against the AUD and NZD. The AUD was 0.7% lower to 0.6723. The NZD and AUD have underperformed following the weekend news of China setting a growth target of only ‘around 5%’ this year. The target should be an easy beat bouncing out of a COVID impacts 2022, fueling doubts about the appetite for infrastructure-led stimulus amid longer-term efforts to shift growth drivers in favour of the consumer. China also projected only a 5.5% increase in fiscal expenditure this year, lower than the pre-pandemic norm and which would result in the lowest ratio of spending to gross domestic product in 11 years.

In equity markets, the S&P500 is up 0.2% heading into the last hour of trading. The S&P500 had extended last weeks gains, up as much as 0.8% intraday, before paring gains alongside the move higher in US yields. Communications and IT stocks led gains, offset by a slump in materials stocks led by metals and mining. Energy and materials were also the underperformers in an overall 0.6% gain in the ASX 200 yesterday. Iron ore and coal prices were also a little lower, weighed by fears around the demand outlook in China, the world’s largest consumer of raw materials. The Nasdaq was 0.2% higher. In Europe, the Euro Stoxx 50 gained 0.4%.

In economic news, data releases were firmly second tier but Eurozone investor confidence and retail sales were on the weak side of expectations while US factory orders and durable goods were broadly in line. The NY Fed’s Global Supply Chain Pressure index fell back below its long run average in February from peaks four standard deviations above average in December 2021. The index integrates a number of largely well told data points about the easing supply chain situation including less shipping congestion, an easing of parts shortages, shorter delivery times and weaker consumer demand, with the NY Fed concluding that “global supply chain conditions have returned to normal.” The data are consistent with ongoing disinflationary pressure across goods, but say little about the battle against services sector inflation.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.