A private sector improvement to support growth

Insight

Hawkish ECB rhetoric post 50bps rate rise spooks risk markets

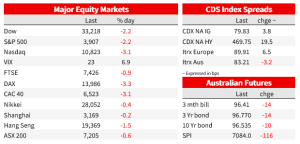

It has been a big night in markets, with the modestly ‘risk-off’ reaction to the Fed on Wednesday from what was seen as a slightly more hawkish than expected set of outcomes, greatly exacerbated by the messaging out of the ECB’s meeting. Rates were raised by 50bps as expected but the Governing Council warned of ‘significant’ rate rises still to come and President Lagarde later made clear that meant further 50-point moves were to be expected and that the mark needed to adjust its pricing for the ECB’s terminal rate higher (it has). US equities are coming into the close showing loses of +/-3%, the longer end of the US Treasury market has caught a safe haven bid (but not the short end, where yields are higher) and the USD is showing a gain of 1% in BBDXY index terms. AUD/USD, which traded as high as 0.6893 on Wednesday, has fallen to as low as 0.6680.

No less than seven central banks have handed down policy decisions during the course of Thursday (and I might have missed one or two more) five of them raising rates by 50bps (ECB, BoE, SNB, Denmark and Mexico), one by 0.25% (Norges Bank) and one (Taiwan) by just 0.235%. These were all as expected. The accompanying commentary from the ECB. Including President Lagarde has been responsible for much of the subsequent market reactions.

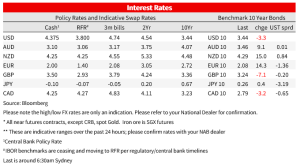

The ECB delivered the anticipated 50bps hike in the deposit rate to 2.0%, dialled down from 75bps at each of the previous two meetings, and indicated in the post-meeting Statement that interest rates will still have to rise “significantly” at a steady pace. Bloomberg subsequently reported that more than a third of the Governing Council pushed for a larger 75bps hike at the meeting.

ECB President Lagarde didn’t mince words, saying “anybody who thinks that this is a pivot for the ECB is wrong…we should expect to raise interest rates at a 50bps pace for a period of time ” and compared the outlook to the Fed, where she said the ECB “had more ground to cover”, implying that she saw the policy rate needing to be raised by at least another 100bps, after the Fed’s projection of 75bps more. On top of this, quantitative tightening will begin from March at an initial rate of €15b per month until the end of June, with the pace after that yet to be determined. This was not a hawkish developments though, at least relative to expectations, being well flagged and with some thought that QT could begin sooner than March.

Post ECB, money market moved pricing for the terminal policy rate lifted to 3.10% (In September 2023) from 2.84% the day before. Two-year Schatz yields are up 22bps on the day and 10-year Bunds by 14bps, so very pronounced bearish curve flattening. EUR/USD jumped to as high as 1.0735 after Lagarde’s 50-point comments hit the wires but has subsequently retreated to a little over 1.06 as the USD catches a strong safe haven bid in conjunction with sharp falls for US equities.

The Bank of England also hiked by 50bps to 3.5%, as expected, but with a split vote three ways, six members voting for 50bps, one more hawkish at 75bps and two more dovish at unchanged (no-one for 25bps). The forward guidance noted “the majority of the committee judged that…further increases in Bank Rate might be required”. While there was no explicit repeat of previous BoE commentary that in its view market pricing for the BoE’s terminal rate was too high, we did see the market slightly paring back its terminal Bank Rate pricing, from a prior 4.57% in September 2023 to 4.52% (in June and July), while 2-year gilt yields ended Thursday 6bps lower, in sharp contrast to much higher Eurozone equivalents and too higher US Treasury yields. GBP has, after the ultra-risk sensitive AUD, been among the worse currency performers overnight, GBP/USD currently -1.9% on Wednesday’s New York close, versus a 2.3% drop in AUD/USD over the same period.

US data releases were mostly weaker than expected. Retail sales fell by 0.6% m/m in November, the largest fall in 11 months, and ex auto and gas sales fell 0.2%. After adjusting for inflation, the figures are even weaker. Industrial production fell 0.2%, boosted by higher utilities, with manufacturing production even weaker at minus 0.6 m/m. The Empire (New York State) Manufacturing, admittedly a small survey, was very much weaker than expected at -11.2 from 4.5 last month, while the Philly Fed index rose to -13.8 against a rise to -10 expected, with new orders slumping to -25.8. Initial jobless claims went against the grain of weaker data, coming in at an improved 211k, but likely impacted by seasonal factors around the Thanksgiving holiday. Continuing claims, the better lead indicator of the labour market, were unchanged at 1,671k (only very marginally lower than expected) and still signalling a turn down waiting in the wings.

US equities, with more than half an hour of trading still to come, are currently showing losses of 2.4% for the S&P500 and 3% for the NASDAQ. IT and Communications Serives are the worse two performing sub-sectors of the S&P, down by 3.5% and 3.8% respectively. APAC regional equities look set for a very poor run into the weekend.

NAB Markets Research Disclaimer

A private sector improvement to support growth

Insight

Online retail sales growth accelerated 1.1% in April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.