Online retail sales growth slowed in May following a fairly strong April

Insight

Volatility has come roaring back in Thursday’s offshore session.

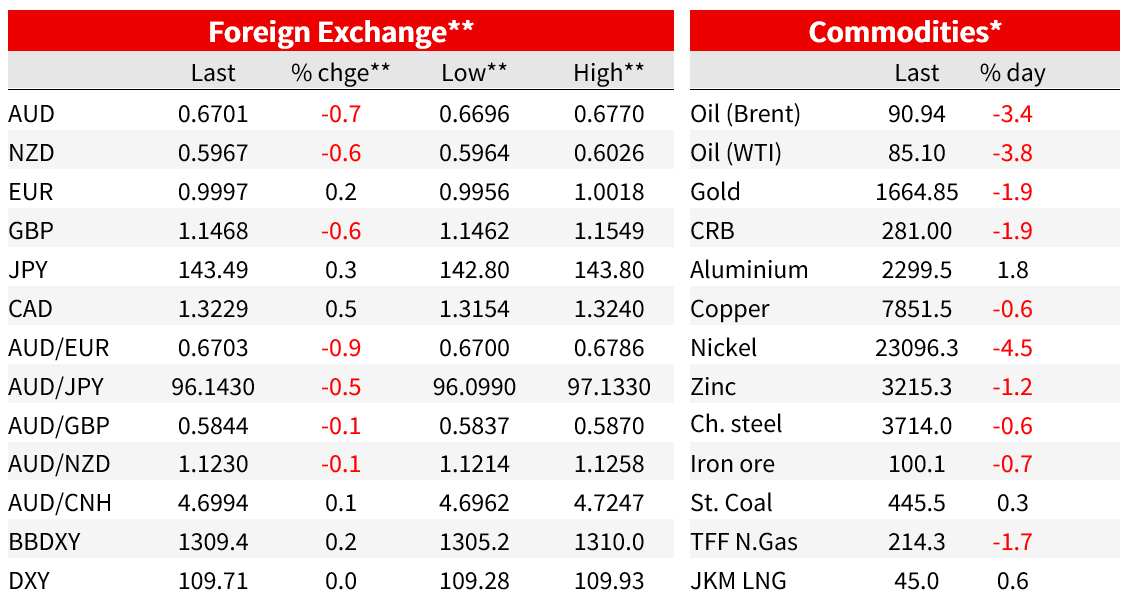

Following the hiatus in market volatility on Wednesday in the aftermath of Tuesday’s CPI-related ructions across all asset classes, volatility has come roaring back in Thursday’s offshore session, no more so than in AUD/USD which is back below 0.67 having traded above 0.69 in front of US CPI. USD/CNH punching up though 7.0 during the London morning is the proximate cause, while commodity currencies in general have suffered under the weight of near-4% falls in oil prices – also gas (more so in the US than Europe). One factor here has been the averting of a US railroad workers strike which had it gone ahead threatened to seriously disrupt coal deliveries to power plants.

We’ve had a lot of US data overnight, but it’s been a very mixed bag with none of it proving to be especially market moving (summarised above). Most interesting perhaps has been the Atlanta Fed’s GDP Nowcasting unit lowering its latest estimate for Q3 GDP estimate to just 0.5% from 1.3% previously (and a prevailing Bloomberg market consensus of 1.4%). Three consecutive quarters of negative US GDP anyone? Retail sales was the top tier release and where headline sales at 0.3% against a fall of 0.1% expected were flattered by auto sales (where higher prices had a hand) while the ex-autos and gas, and control group, measures fell short of expectations at 0.3% and 0.0% respectively (lower gas prices one factor here). Meanwhile, latest weekly jobless claims at just 213k, with the prior week revised down to 218k, confirms a still red-hot US labour market.

ECB Governing Council members have been out in force (Guindos, Makhlouf, Centeno) with something of a spread along the hawk-dove spectrum. Vice President Luis de Guidons urges ‘determined action’ to combat record inflation while warning that growth is set to slow ‘substantially’, also noting euro deprecation adds to inflation pressures. Fellow GC member Gabriel Makhlouf says it’s ‘absolutely necessary’ to be raising rates and that persistent inflation is damaging to economic stability. Portugal’s central bank chief Mario Centeno is much more measured, saying monetary policy should be predictable and move in small stops, and that he sees no sign of inflation expectations becoming unmoored. He’s likely to be outvoted when the ECB next meets, with the hawks clearly in the box seat at present.

To markets, and FX has been lively, commodity price and the Chinese Renminbi the primary drivers. Oil is pulling up a little late in late New York trading from 4%+ intra-day falls but WTI crude is still down $3.75 on the day and Brent -$3.50 . US prompt gas prices were off around 10% (and the European TTF benchmark earlier closed 3%). As well as the tentative settlement of the US railroad workers dispute which threatened to disrupt coal deliveries, comments from the Department of Energy that it doesn’t have a particular price level in mind to replenish the Strategic Petroleum Reserve, plus deepening concern about demand destruction implicit in a global economic slowdown, have created something a of a perfect (one-day) storm for energy prices. Commodity price slippage is not confined to energy though, with Nickel off 4.5%, copper down almost 1% and ion ore futures -0.8% (aluminium bucks the trend, +1.6%).

USD/CNH rose through 7.0 around mid-day London time Thursday and has not really looked back since, finishing in New York around 7.0150 and the onshore CNY earlier closing at 6.9950. Today’s CNY fix will be particularly interesting, and doubtless Chinese policy banks will be active on the left-hand side of the spread during the China day. The read-through to AUD and NZD from CNH above 7 is obvious on the tick charts and means NZD/USD has fallen to a new 2 ½-year low of 0.5964 while the AUD/USD low of 0.6696 still leaves it 15 pips or so above its mid-July 2 ½-year low.

History shows than once verbal warnings prove ineffective in arresting undesirable JPY moves, “rate checks” are the next move. In Japan, the Ministry of Finance (MoF) makes the intervention decision and the BoJ does the actual buying or selling. A verbal check doesn’t necessarily mean intervention is imminent, but certainly increases the risk. On the day, the rate check was enough to spook the market with USD/JPY falling almost 1% to ¥143.1855 currently, after falling to an overnight low of ¥142.5545.

USD/CAD has also posted its highest level since March 2020. Losses for all three currencies have only been eclipsed by the NOK, a full 1% lower on the day. EUR (and CHF) in contrast are both slightly up on the day (falling energy prices a boon not a blight for the Eurozone of course) and this has limited the rise in the DXY USD index to less than 0.1%. USD/JPY is higher, +0.3%, but less than might have bene expected given the latest rise in US Treasury yields, so there is evidently a bit of caution heading into the weekend (and next week’s BoJ meeting) regarding the risk of FX intervention, however ephemeral the impact on USD/JPY a burst BoJ selling – under instruction from MoF – would likely prove.

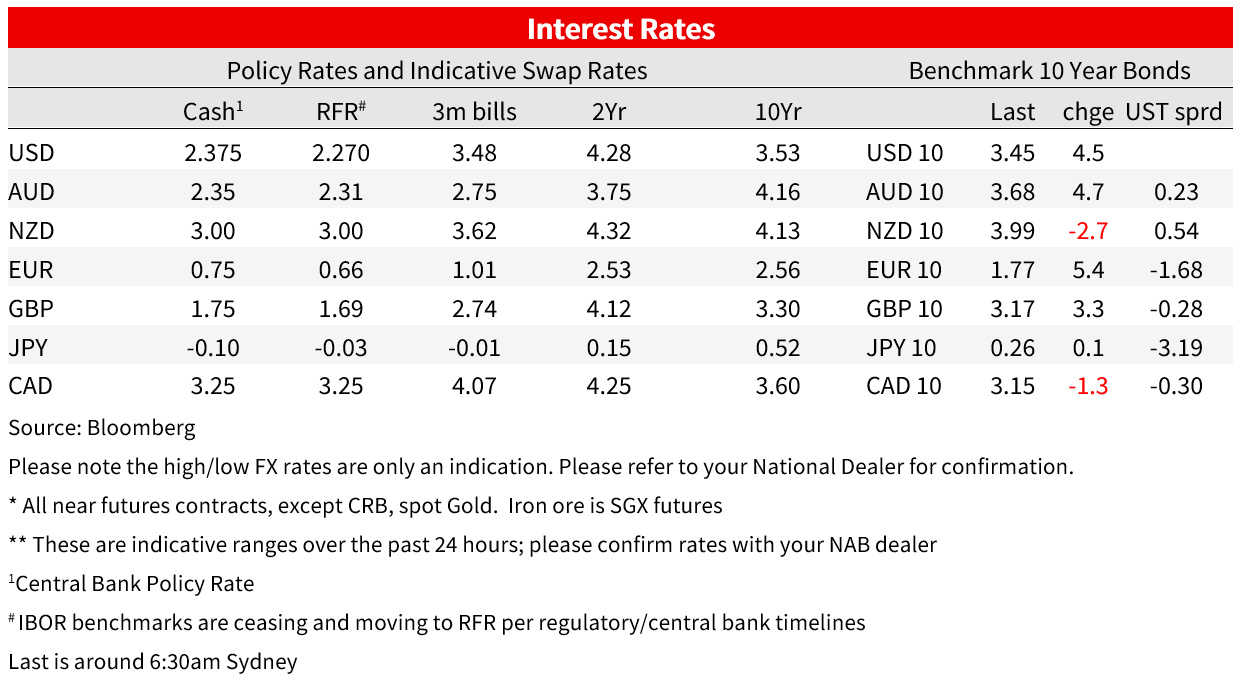

The back-up in US Treasury yields amounts to 4.5bps for the 10-year to 3.45% and 7.4bps for the 2-year taking it to a new cycle high of 3.863%, with Fed Funds futures pricing now pricing the terminal Funds rate at a touch under 4.5% (4.46% in March 2023). Also, to note is that US 30-year mortgage rate climbed above 6% last week (6.02% average) from 5.89% the week before and to their highest since November 2008. More pain ahead for the US housing market because of this.

GBP is up around 0.45% to 1.1539, a small recovery after plunging over two big figures the day before. Yesterday went Sydney was preparing to go home, the UK August headline CPI edge back below 10% (9.9%) with the pullback in vehicle fuel helpful. Elsewhere, food inflation was 10.8% after 10.4%. The more labour intensive services inflation came at 5.9% after 5.7%. Good inflation news, albeit still elevated and after yesterday’s solid labour market stats, the market is now pricing 68.7bps of BoE hike next week.

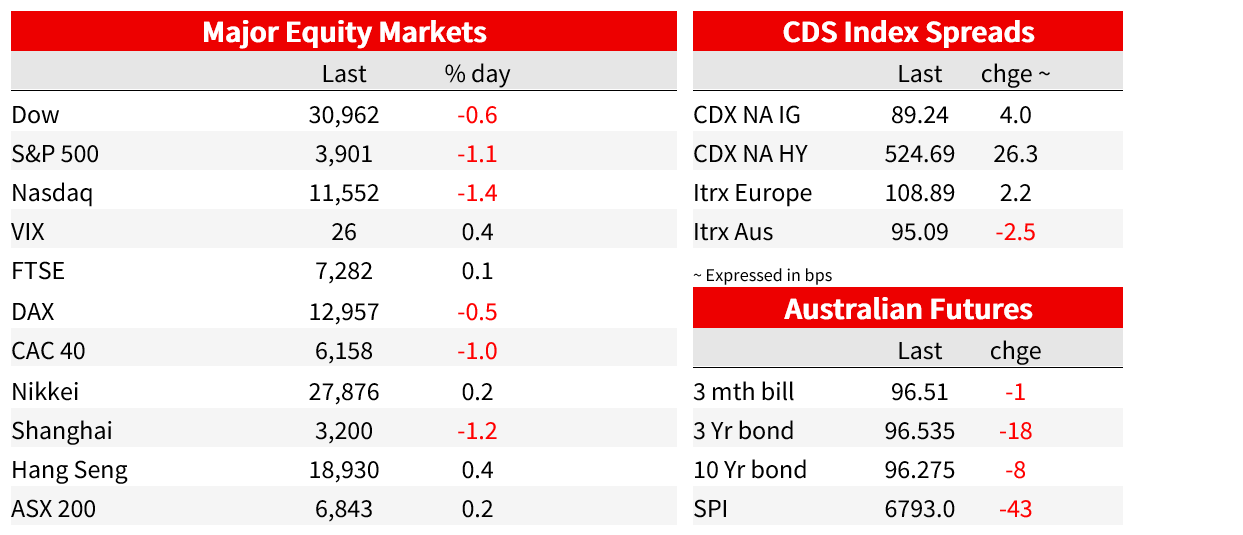

Equity markets closed in New York with the S&P500 down 1.1% (up from an intra-day low of -1.5%) and the NASDAQ -1.4% (had been -1.9% earlier). Higher Treasury yields hurt the IT sector most and hence the NASDAQ relative to the S&P (IT -2.4% within the latter) while the energy price falls saw the energy subsector perform worst of all (-2.5%).

Finally, all we have seen regarding the Putin-Xi meeting in Uzbekistan are reported comments that President Putin told his Chinese counterpart Xi Jinping he understands Beijing’s “questions and concerns” about his invasion of Ukraine and that Xi said the two countries could “inject stability and positive energy to a world in chaos.” Right.

NAB Markets Research Disclaimer

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.