Online retail sales growth slowed in May following a fairly strong April

Insight

Hopes for a deal on the debt ceiling improved.

“Had to have high, high hopes for a living. Didn’t know how but I always had a feeling. I was gonna be that one in a million. Always had high, high hopes.” – Panic! At The Disco

NZ: PPI output(q/q%), Q1: 0.3 vs. 0.9 prev.

AU: Employment change (k), Apr: -4 vs. 25 exp.

AU: Unemployment rate (%), Apr: 3.7 vs. 3.5 exp.

US: Initial jobless claims (k), wk to May-13: 242 vs. 251 exp.

US: Philly Fed business outlook, May: -10.4 vs. -20.0 exp.

US: Existing home sales (m/m%), Apr: -3.4 vs. -3.2 exp.

House Speaker Kevin McCarthy and Senate Majority Leader Chuck Schumer were making plans for votes in the coming days on a bipartisan deal and McCarthy said the House could vote on a deal on the debt ceiling as soon as next week. A word of caution from McCarthy ally and Financial Services Chairman Patrick McHenry that the two sides are “not close to being done ” failed to enduringly temper rising expectations a deal will be done. US equities, yields, and the dollar were each higher. US jobless claims reversed last week’s rise, and the Fed’s Logan sounded unconvinced the case for a pause was yet made with June rate hike bets moving higher to around one third priced, well up from the near zero chance discounted a week ago.

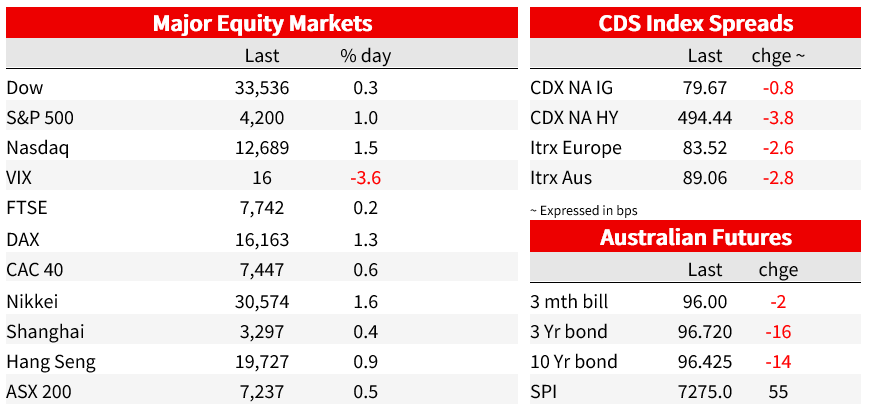

The S&P500 rose 0.9% to close at their highest level since 25 August and the Nasdaq outperformed, up 1.5%. In Europe, the Euro Stoxx 600 was 0.4% higher, while the Nikkei 225 rose 1.6%. Gains were led by IT and Communication Services. The Nasdaq 100 closed at its highest level in more than a year as large tech companies helped drive markets higher.

US yields were higher across the curve. The 10yr yield rose 9bp to 3.65% to their highest since 15 March and up a 27bp over the last 5 trading sessions. The 2yr was 10bp higher at 4.25%. June rate hike bets were increased, now pricing a 38% chance of a June hike compared to 20% yesterday while cuts were pared, January 2024 pricing now around 4.45 from 4.33 yesterday. The case for pausing is not yet clear for Dallas Fed’s Logan, who said that “ the data in coming weeks could yet show that it is appropriate to skip a meeting. As of today, though, we aren’t there yet.” As for the role of banking, Logan said that “even now, they say the main reason for the latest tightening is restrictive monetary policy, not stress in the banking system.” Separately, Jefferson sounded much more patient, emphasising the tightening already in place and the lags of monetary policy, “a year is not a long enough period for demand to feel the full effect of higher interest rates.” Both speakers lamented the lack of progress on inflation after stripping out energy and food. Chair Powell speaks alongside former chair Bernanke on a panel tonight.

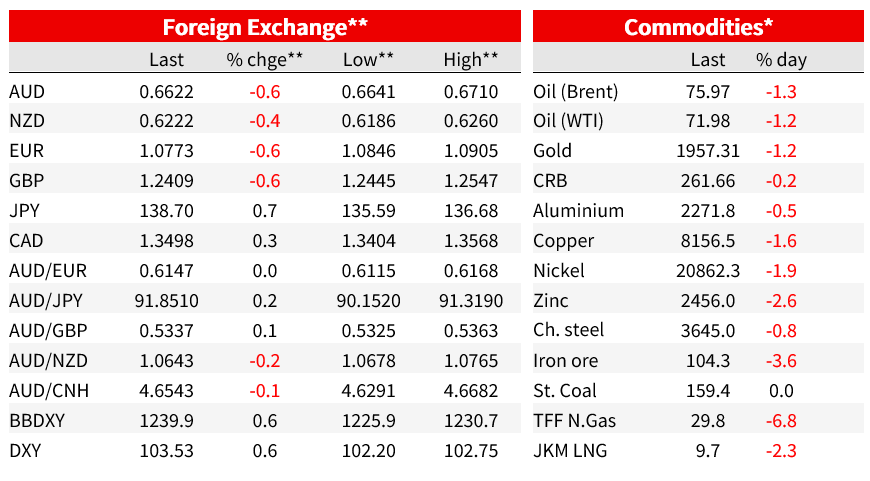

The US dollar was broadly stronger, up another 0.6% on the DXY to 103.53 for its third straight daily gain . That takes the dollar index up 2.2% from intraday lows 10 days ago and to its highest levels since 20 March. Positive risk sentiment on buoyed hopes for a debt-limit saw 0.7% declines in the yen and the franc, but USD strength was broad-based. The dollar was higher against all G10 currencies; the euro was 0.6% lower to 1.0773. The AUD was down 0.6% to 0.6622. The softer local data yesterday (see below) saw a short-lived 0.5% spike lower before retracing, with the intraday lows of 0.6605 coming early in the US session alongside the broadly stronger US dollar.

In US data, the jump in initial claims the prior week was reversed with a drop of 22k back to 242k this week, below expectations for 251k. Massachusetts had reported issues with a number of fraudulent claims and alone accounted for most of last week’s lift and this week’s decline, and similar issues elsewhere may be further complicating the picture from this indicator. Some other timely indicators including Challenger layoffs and NFIB hiring intentions do continue to suggest some softening in the tight US labour market is on the horizon. But for jobless claims, if you leave last week’s surprising number aside, the trend looks as much like sideways from the 245k in early March than it does a trend higher , and excluding Massachusetts, initial claims have been heading lower recently. Continuing claims also dipped slightly to 1799k, down from an early April peak of 1861k, and are no higher than they were through March. In other US data, the Philly Fed manufacturing index rose to -10.4 from -31.3, above consensus for -19.8. The upside surprise on the Philly Fed contrasts Monday’s weaker than expected NY Fed index in the patchwork of regional surveys so far.

Locally, employment data yesterday disappointed at -4k against +25k expected . The unemployment rate also ticked higher to 3.7% vs 3.5% expected (though a less notable 3.54 to 3.66 unrounded). The unemployment rate is back to where it was in January, and a word of caution on the month-to-month numbers is negative prints in December and January were followed by strong 50k+ gains in February and March, and the April data may have been confounded by Easter occurring wholly in the survey reference period. Hours worked up 2.6% m/m and a dip in the underemployment rate certainly don’t paint the same picture as the headlines.

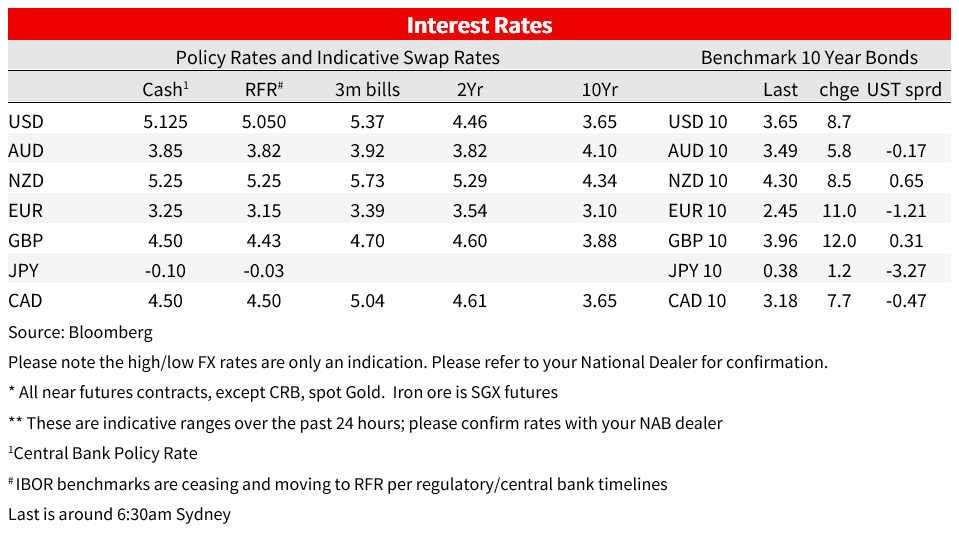

Combined with the WPI data yesterday, for the RBA the data flow this week has been marginally on the softer side, but still broadly consistent with their May forecasts. They make it hard to imagine the RBA would opt to raise rates again as soon as June having previously slowed the cadence of hikes by pausing in April, but they are far from conclusive the RBA is done at 3.85%. AUD 3yrs briefly dipped about 8bp lower on the data before retracing and 3yr futures continued to move lower alongside US Treasuries , with implied yields 10bp higher over the day to 3.28%. Futures markets now imply a 63% chance of a hike by September, a touch higher than a day prior.

The NZ Budget showed a significant deterioration in the fiscal accounts compared to the half-year update, reflecting a weaker economy generating a shortfall in tax revenue, mixed in with higher spending. The accounts show larger underlying operating deficits of 1.8% of GDP for the current fiscal year and next year, while rising capex adds to the pressure on rising debt. Our colleagues at BNZ Economics added in an additional 25bps to its RBNZ projections , now seeing two 25bps hikes taking the OCR to 5.75% in July. NZ rates were higher across the board, with OIS pricing for August up 10bps to 5.79%, taking its gain for the week so far to 28bps.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.