Coming in for landing in a heavy cross wind

Insight

Strong earnings continue to outweigh Delta concerns with the S&P500 reaching a new record high, So far 87% of companies reporting have beaten expectations and if maintained would be the strongest earnings beat since 2008.

https://soundcloud.com/user-291029717/high-hopes-big-concerns-and-fewer-babies?in=user-291029717/sets/the-morning-call

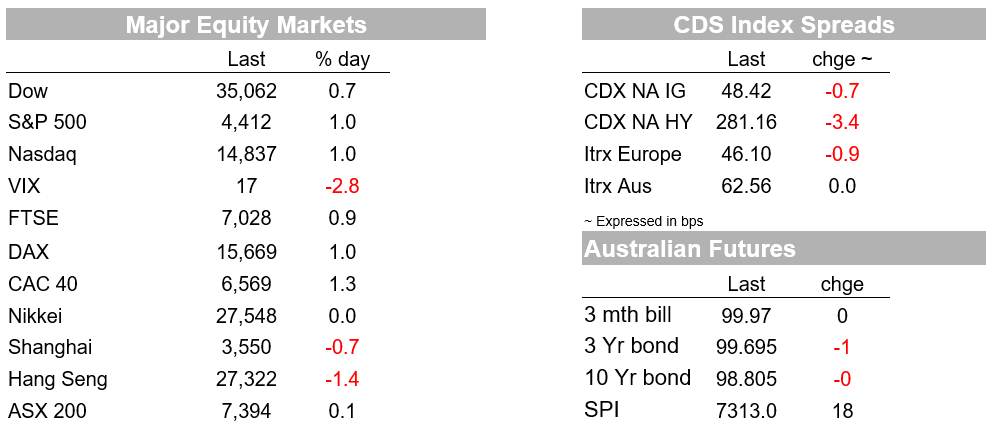

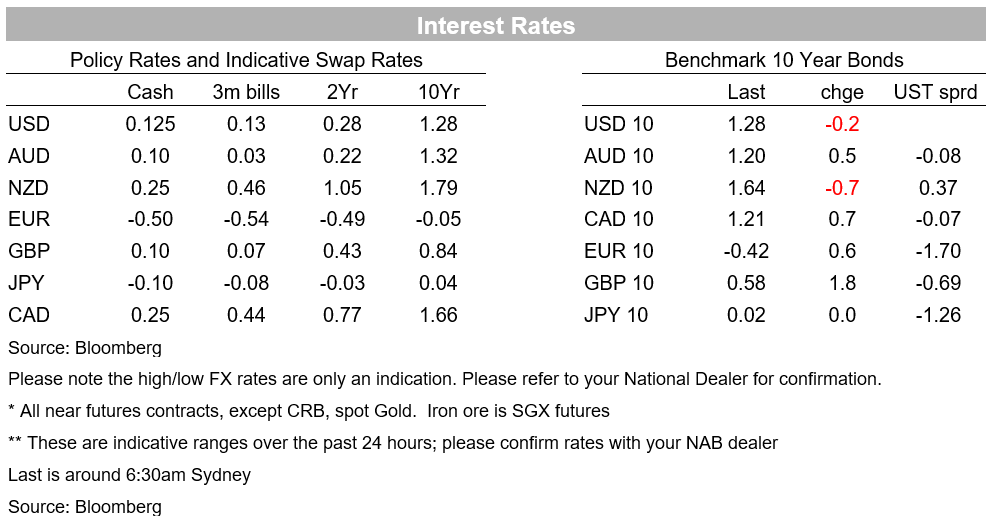

Strong earnings continue to outweigh Delta concerns with the S&P500 reaching a new record high , closing up 1.0% on Friday and 2.0% on the week. Strong earnings by Twitter (+3.0%) and Snap (+23.8%) highlight that firms are paying up for digital advertising amid the strong rebound, which should flow through to strong earnings for Alphabet (+3.6%) and Facebook (+5.3%) this week. So far 87% of companies reporting have beaten expectations and if maintained would be the strongest earnings beat since 2008 (note 165 S&P500 companies report this week – see below for details). Delta variant concerns though persist and notably bond markets continue to trade with a cautious tone. US 10 year yields were little changed on Friday at 1.28% and while for the week are only down 1bps, they did reach a low of 1.13% last week. Aside from Delta concerns, the key themes for this week will be the FOMC announcement, US and European Q2 GDP figures, as well as earnings. As for Australia we have Q2 CPI figures on Wednesday, though virus numbers will overshadow with Sydney in a protracted lockdown that will persist into August.

Likely to dominate Delta news was an Israeli study that showed vaccine effectiveness declines with time and provided updated estimates of vaccine effectiveness. While Pfizer/BioNTech vaccine was found to be 91.4% effective in avoiding serious illness, it was only 39% effective in preventing against infection (albeit mildly). Importantly effectiveness in preventing infection fell to just 16% for those vaccinated in January, compared to 75% for those vaccinated in April. The three broad implications are that a high percentage of the population needs to be vaccinated, social distancing restrictions may need to continue for fully vaccinated people until the country-wide vaccination threshold lifts enough, and booster shots may be required. It is within this context that the US’ Chief Medical Officer Fauci is looking to recommend mask mandates for fully vaccinated people and that some Americans may need booster shots. For developed economies that likely pushes back the full recovery by a quarter as countries seek to lift vaccination rates (COVID passes/passports are being used in Europe to encourage this), but for emerging markets the recovery may take longer.

Economic data was generally strong on Friday with the PMIs supporting the notion that European growth may be set to overtake the US in Q3. The Eurozone Composite PMI reached its highest level since 2000 at 60.6 (vs. 60 expected). The services index rose to a 15-year high at 60.4 (vs. 59.3 expected), while manufacturing dipped slightly to a still very high 62.6 from 63.4. The US Services PMI in contrast eased back to 59.8 from 64.6 and 64.5 expected. While the US PMI is less well followed then the ISM, the PMIs do suggest a pick-up in European growth into Q3. IHS Markit cautioned that while the PMIs painted a positive picture, there were signs the spread of the delta variant was starting to dampen business expectations for the year ahead which will be important to watch for global activity going forward. The usual supply chain anecdotes and pricing pressures were notable and Intel on Friday also noted that it expected the global semiconductor shortage to stretch into 2023, in contrast to the more optimistic take from TMSC.

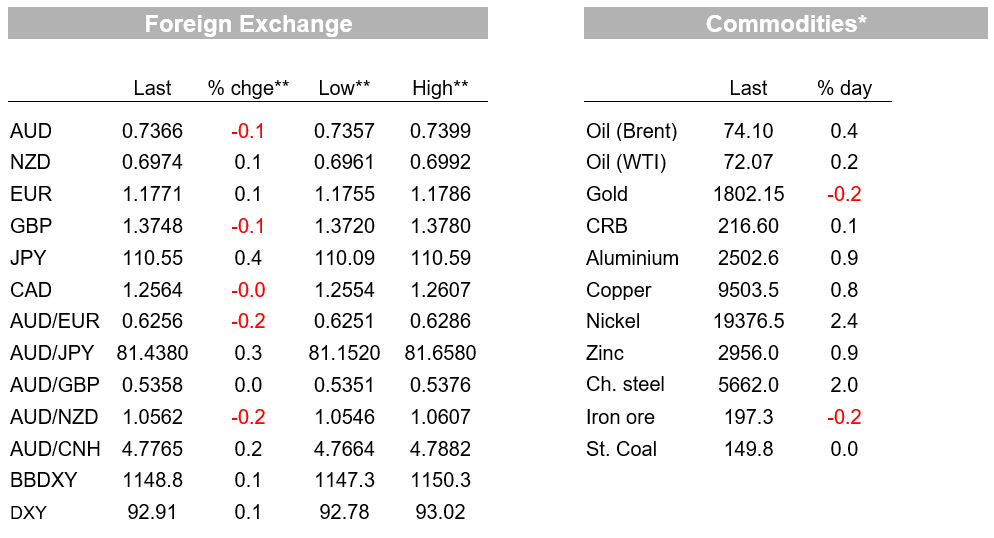

FX moves were minimal on Friday, with all currencies except the JPY moving less than 0.2%. The Bloomberg USD index (BBDXY) was up 0.1% on Friday and 0.25% on the week; it continues to hover near its highest level since early April. On the week, the AUD was the worst performer, down 0.5% to around 0.7365, amidst the ongoing lockdowns in Greater Sydney, Victoria and South Australia. The JPY was close behind last week, down 0.4%, reflecting more positive risk appetite and higher equity markets. The NZD ended last week around 0.6975, little changed on Friday but down 0.35% on the week.

A busy week this week with Australian Q2 CPI and virus numbers, while offshore the focus is on the FOMC, and then in terms of data Q2 GDP figures for the Eurozone and the US. Earnings also continues. Details below:

A quiet day domestically with nothing scheduled. Offshore it is also a very quiet start to the week in what is a big week for data, events and earnings. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.