A private sector improvement to support growth

Insight

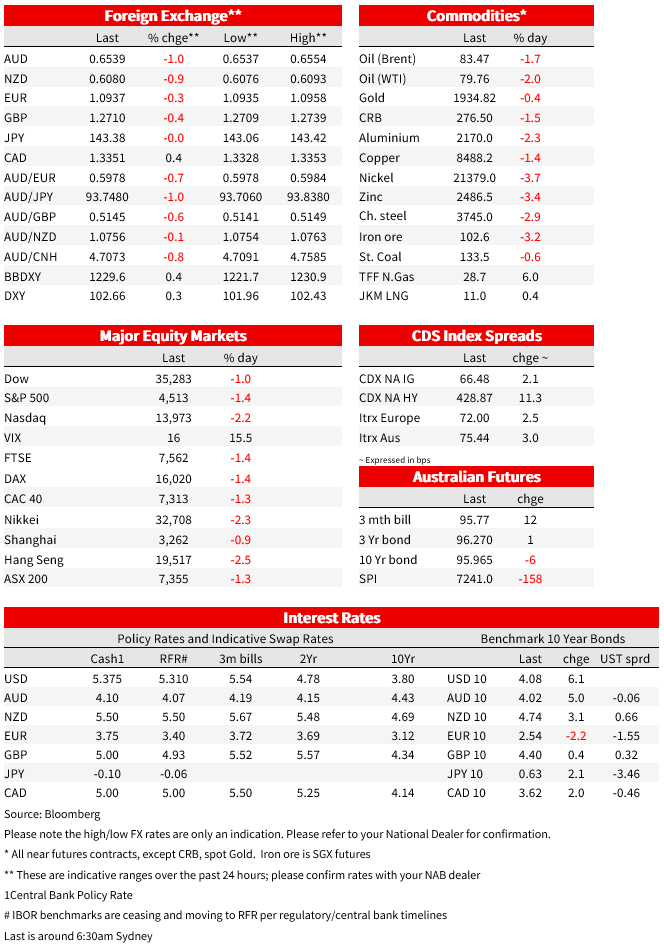

Yields rise, US 10yr hits 4.12% before easing back to 4.08%, highest since Nov 2022

Yields continued their climb overnight. One catalyst was a stronger than expected ADP Employment (324k vs. 190k expected and 455k previously), while the Treasury’s quarterly refunding plan showed greater than expected allocation to longer-term securities (note the plan for greater issuance in total was given earlier in the week). The US 10yr yield rose to a high of 4.12%, before paring back to 4.08%, and is up 6.1bps over the past 24 hours. A similar lift in 2 year yields to 4.94% was fully reversed latter in the session with 2yr yields actually -3bps on the day to 4.87%. Yield curves steepened with 2/10 now at ‑80.5bps, having moved from -108bps in early July. The nominal moves have been reflected in real yields with the 10yr TIP yield +4.9bps to 1.71%, and the implied breakeven is broadly steady at 2.36%. US Fed pricing in the near term was little changed (around a 34% chance of a 25bp hike by November), though pricing of cuts was extended slightly with 128bps worth of cuts by the end of H2 2024, from 122bps yesterday.

Risk assets were under pressure given the backdrop of higher yields , while some profit taking in equities was cited given the strong rally (note the S&P500 had rallied some 26% from its low of 2022). The S&P500 was -1.4% with some rotation from tech to defensiveness evident (consumer staples +0.3% vs. tech -2.6%; note NASDAQ was -2.2%). Earnings continue to be a support with around 82% having positive surprises according to FactSet. The US ratings downgrade by Fitch to AA+ from AAA didn’t seem to have much of a market reaction, apart from umbrage shown by economists who cited the inconsistency given the strength in the economy, and the financial and security umbrella provided by the US. Modern Monetary Theorists also cited the mantra that if a country borrows in its own currency, it will never actually default involuntarily as long as it controls the printing press (little comfort given the flip side of that is inflation). Fitch now joins S&P with its AA+ rating (note S&P did its downgrade 12 years ago). What the downgrade could do though is kickstart divisions around government spending – a confrontation could be likely given spending bills will be needed within 59 days.

As for the data, ADP Employment appeared to be the main driver. On this measure employment rose by a much larger than expected 324k in July vs. 190k expected. That suggests upside risks to Friday’s Payrolls. However, analysts continue to note the usual health warning that these figures are a poor indicator of official payrolls (last month’s ADP figure over-shot the official figure by a massive 348k). The wages components of the ADP report were more friendly, with workers who stayed in their jobs seeing a 6.2% pay increase, the weakest since November 2021 and for those who changed jobs the median pay rise was 10.2%, the weakest in two years. The other driver of course was Treasury’s quarterly refunding plan. The plan for much greater bond issuance for the quarter ahead was given earlier this week, with $1 trillion of new supply, but the allocation of $103b for longer-term securities beginning next week was slightly larger than expected ($103bn, up from $96bn). The other factor cited for yields was some hedging flow given corporate issuance.

In FX, it was all about USD strength with DXY +0.3%. USD/JPY was insulated given the risk-off mood and was -0.0% to 143.38 despite the move higher in yields. Global risk proxies of the AUD (-1.0% to 0.6539) and NZD (-0.9% to 0.6080) fell sharply, though most of the fall in the NZD occurred during APAC following the mixed NZ labour market report (more on that below). The AUD is the weakest of all majors, and is trading at a two month low. As for other pairs, EUR -0.3% and GBP -0.4%.

Meanwhile in NZ, labour market data showed a strong 1.0% q/q lift in employment growth in Q2, enabled by a strong increase in labour supply, supported by net migration. The unemployment rate rose 2 ticks to 3.6% to its highest level in two years. The slightly easier than expected labour market conditions was also reflected in private sector labour cost inflation slightly undershooting expectations at 1.1% q/q. The overall message was a still-tight labour market but a slight easing pressure on wages, supporting the RBNZ’s on-hold policy stance. The market appeared to be positioned for a positive surprise to the data, so the softer figures triggered lower rates and a weaker NZD. By the end of the day the curve was steeper, with the 2-year swap rate down 3bps to 5.48% and the 10-year rate was up 3bps to 4.68%. NZGBs also showed a steeper curve bias.

Coming up:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

A private sector improvement to support growth

Insight

Online retail sales growth accelerated 1.1% in April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.