Total spending grew 0.9% in June.

US equities fail to bounce after Monday, with the S&P500 down -0.1 ahead of the FOMC.

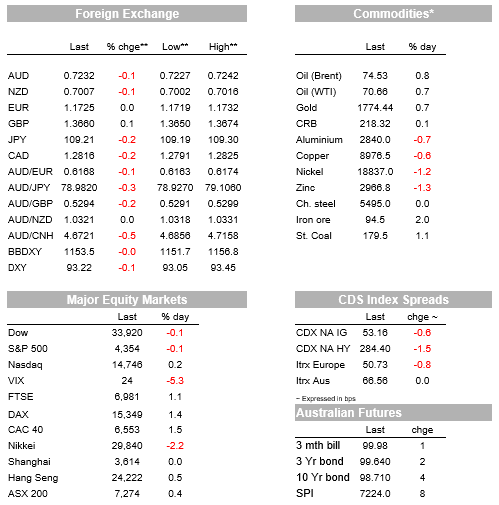

Markets appear to have settled a little after Monday’s sell-off, with equities in Asia and Europe bouncing (Hang Seng +0.5% and Eurostoxx50 +1.3%). US equities though have failed to hold onto their initial bounce with the S&P500 closing down -0.1% after initially opening up 0.8%. A Bloomberg red headline around when New York opened stating Evergrande missed interest payments due Monday to at least two banks looks to have weighed – note this was well telegraphed by China’s housing regulator last week. Market sentiment thus remains fragile ahead of the FOMC today and also ahead of Evergrande’s interest payments on two bonds worth $119.5m, due on Thursday. Overall though it appears market fears of an Evergrande’s ‘Lehman’ moment fears have calmed as analysts put their faith in China’s authorities to undertake an orderly restructuring. Meanwhile for the FOMC today, even though a tapering announcement is not expected, the dot plot may deliver a hawkish surprise and require Powell to be dovish and push back in the press conference.

Somewhat fragile risk sentiment is evident in FX with safe-haven currencies stronger again with USD/Yen -0.2% to 109.21 and USD/CHF -0.4% to 0.9236. The USD meanwhile gyrated in line with equities to be flat in broad index terms (BBDXY -0.0%). Other major FX pairs were little changed against the dollar with EUR +0.0% to 1.1727 and GBP 0.2% to 1.3666. Commodity currencies were slightly weaker with the AUD -0.1% to 0.7232 along with the NZD -0.1% to 0.7007. The softness in the NZD also came in the wake of speaking notes from the RBNZ’s Hawkesby who pushed back on the prospects of a 50bps hike in October by noting in times of uncertainty “central banks globally tend to follow a smoothed path and keep their policy rate unchanged or move in 25 basis point increments”. The Loonie though saw modest gains with USD/CAD -0.2% as PM Trudeau was re-elected as PM in a minority government (he had hoped for a majority).

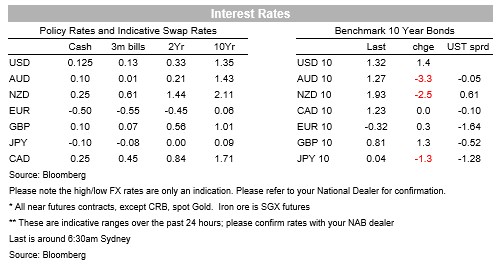

Rates markets ahead of the FOMC (Thursday 4.00am Sydney time) have been quiet. US 10yr yields are little changed at +1.2bps to 1.32%. While the consensus is for no taper announcement and for this to be delayed until November or October, there are some fears of a hawkish surprise which centre around the dot plot. There is a low bar to see a 2022 hike being pencilled in (only 2-3 people need to shift the median given 7/18 had a hike pencilled in for 2022), while the Fed will also have dots for 2024 which will give an indication of the steepness of the potential hiking cycle. Your scribe will be looking at the 5s30s curve closely in the wake of the meeting which has flattened considerably over recent weeks and is currently sitting at 102bps which is around the lowest levels since August 2020. Most of the flattening has occurred in the long end space. A 20Y Treasury auction overnight is illustrative receiving good support and stopping through mid and seeing 20Y outperform the 10Y and 30Y very slightly.

As for data it has been a relatively quiet night. The OECD released its latest forecasts, but these are never market moving. Global growth forecasts remained strong and little changed, at 5.7% this year and 4.5% next year. But there were widespread upward revisions to inflation projections, with core CPI inflation for the G20 raised by 0.3% for both forecast years to 2.1% and 2.2% respectively, and with headline rates up to 3.7% and 3.9% respectively, the latter revised up 0.5%. The OECD warned that while “ clear guidance is needed about the horizon and extent to which any inflation overshooting will be tolerated, and the planned timing and sequencing of eventual moves towards monetary policy normalisation”, arguably a shot at the US Fed where some analysts have criticised the vagueness associated with the average inflation targeting framework and shortfalls to maximum employment approach(see OECD Economic Outlook for details). The US also had second-tier Housing Starts/Permits which were much stronger than expected (Starts 3.9% m/m vs. 1.0 expected; Permits +6.0% m/m vs. -1.8% expected). Volatile multifamily dwellings drove the beat.

Finally in NZ, Assistant Governor Hawkesby’s speech notes pushed back on notions of a 50bps hike at the October meeting. Hawkesby explained the Bank’s “least regrets” approach to uncertainty and the market’s takeaway was that the hurdle for a 50bps move next month to kick off the tightening cycle was much higher. Hawkesby noted that when there is a typical amount of uncertainty, “ central banks globally tend to follow a smoothed path and keep their policy rate unchanged or move in 25 basis point increments” (see Hawkesby: A “least regrets” approach to uncertainty for details). In the wake of the speech OIS pricing for the October meeting fell by over 7bps to just under 0.50%, more or less fully pricing a 25bps hike and no chance of a 50bps move. This flowed through the rest of the curve, seeing the 2-year swap rate down 6bps to 1.43%, and a flatter curve, with the 10-year swap rate down only 2bps to 2.11%. Longer term rates were more affected by global forces. NZGB yields were lower across the curve, with 5 and 10-year rates down 3bps.

Finally the Riksbank met overnight leaving policy settings unchanged and pointed to steadfast faith in transitory inflation, forecasting a pace above 3% in the short term but maintaining there are “no plans whatsoever” to tighten policy in 2022.

Today it’s all about the FOMC which makes its decision today (Thursday 4.00am Sydney time). There are also two other central banks meeting including the BoJ and the PBoC – no changes expected for either. For Australia there is a speech by the RBAs Bullock on “The Housing Market and Financial Stability”. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.