We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Share markets are riding high again in the US despite a triple whammy of disappointing reports.

https://soundcloud.com/user-291029717/inflation-confidence-and-retail-merely-temporary?in=user-291029717/sets/the-morning-call

And this is where I go, just when it rains – Elbow

US and European equity markets added to their Thursday gains, ending the week on a positive note. The increase in risk appetite came along notwithstanding underwhelming US data releases, pointing to a pullback in consumers appetite and sentiment together with a great rise in inflation expectations. Longer dated UST yields declined on Friday, although not enough to reverse the curve steepening recorded over the week. The USD was broadly weaker on Friday, but the AUD was still the underperformer on the week.

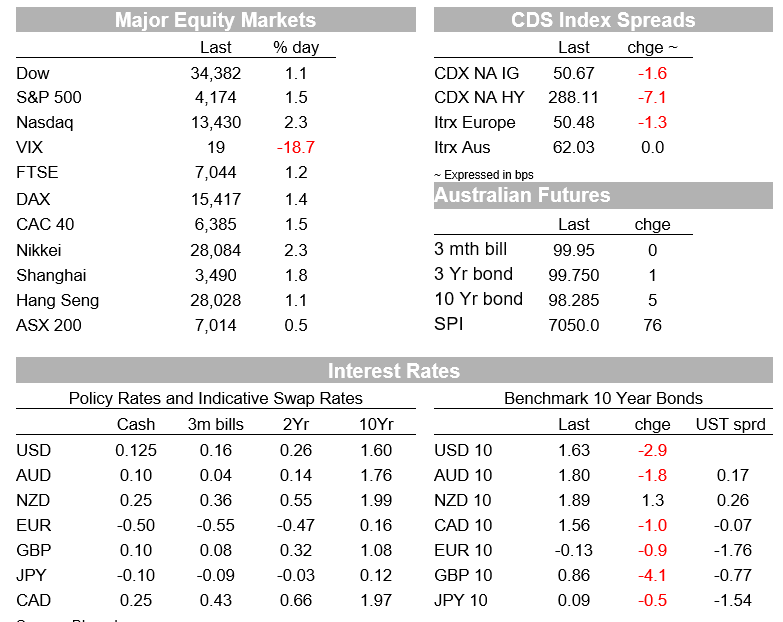

Last week was volatile week for markets. The VIX index ( a measure of expected volatility in the S&P 500) started the week at 18 and it ended the week at the same level, but half way through the week it traded to a high of 28.93 following the higher than expected US CPI print on Wednesday night. On Friday we got a set of data gauging the pulse of the US consumer, but this time the market took the bad news in its stride. Thus bad consumer news is good news as it forces the Fed to keep the stimulatory punchbowl well liquified.

April US retail sales were unchanged, below the consensus for a rise of +1.0% while the core measure (Sales ex-autos) fell 0.8%, well below the +0.6% expected by markets. One caveat to the data was that the March numbers were revised upwards, so the level of sales remained extraordinarily high. The market seemingly read the April weakness as payback for the strong March print with the reopening of the economy suggesting a rebound in spending should be expected in May.

The University of Michigan preliminary consumer sentiment fell 8 points to 82.8, against expectations of a 2 point rise to 90 . Declines in both the expectations index (down 5.1 points) and the current conditions index (down 6.4 points) depressed the headline, with a combination of the end of the stimulus payment flow, higher gasoline prices, and a wobbling stock market noted as potential culprits. Of note, both short-term and long-term inflation expectations shot up, the latter rising to 3.1%, its highest level in a decade.

The data release leaves us none the wiser. On the one side, we have the Fed’s view, apparently embraced by equity investors, implying there is nothing to see here, given that base effects and reopening dynamics mean we should expect volatility in the data and no one said reopening was going to be cheap. On the other side of the argument is rising concerns that inflation is becoming unanchored with a decline in consumer sentiment a reflection of the negative impact inflation is having on disposable income. So at what point does higher inflation become problematic for policy?

For now, the message from the Fed remains unchanged, even Fed Kaplan who recently suggested now was the time to talk about tapering, sounded a little bit more guarded on Friday. Noting that it’s going to take a while to resolve supply-demand imbalances in both labour and commodity supplies. Kaplan believes it would be appropriate to begin discussing erring QE once it becomes clearer that we’re escaping the pandemic and making substantial economic progress. Fed Mester, which traditionally has also been on the hawkish side, kept to the script, arguing that Fed policy was in a good place right now, and that volatility month-to-month is something we should expect, adding “this is not the time to be adjusting anything on policy…it really is a time for watchful waiting, seeing how the recovery evolves”.

So with the Fed committed to its stimulatory policy, equity investors bought the dip again, extending Thursday’s gains into Friday. The S&P500 showed a strong gain of 1.5%, following the previous day’s 1.2% recovery. The index still ended down 1.4% for the week, not fully making up the early-week losses . The NASDAQ gain 2.32% on Friday but still ended the week down 2.34%. Chips gave a lift to the technology sector, extending gains in the wake of a Reuters report that lawmakers in Washington are close to unveiling a $52 bn proposal to aid US microchip production. The funding proposal is expected to be included in bill the Senate will take up this week. In Europe, the Stoxx Europe 600 Index advanced 1.2% while Shanghai Composite was the outperformer on the week, up over 2%.

US Treasuries were already well supported prior to those US data releases and tracked sideways after they printed, the 10-year rate closing the day down 3bps at 1.63%. Friday saw a decent bull flattening of the UST curve, but this was not enough to reverse the curve bear steepening recorded over the week. The 30y bond led the rise over the week climbing 6bps in the past five days, ending the week at 2.34%. Relative to levels at the start of May, the 10y UST Note is about 2bps lower month to date, but over this period the break even component is 14bps higher, so a stepper UST curve and an increase in inflation expectations has been the theme so far in May.

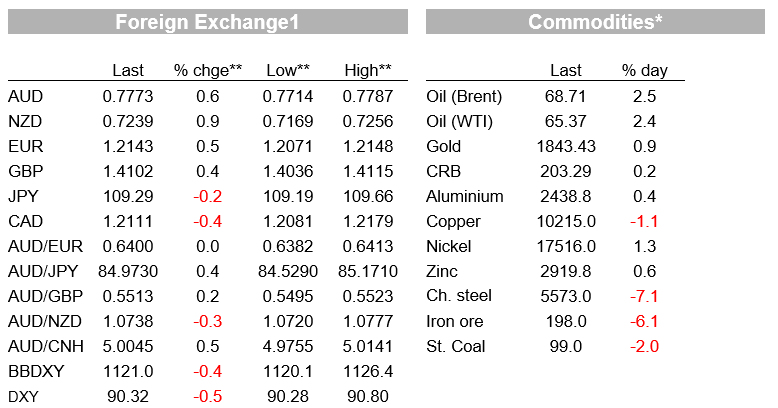

Moving onto FX, the stronger risk backdrop saw the USD give up more of its post-CPI shock gains and it was lower on Friday against all the key majors, with the BDXY index falling 0.4%. The NZD was one of the best performers, gaining 1% on Friday night and closing the week around 0.7250, moderating its weekly loss to 0.4%.

The AUD also managed to outperform the USD on Friday, gaining 0.55% on the day and ending the week at 0.7771. Looking at the week, however, the AUD is the G10 underperformer, down 0.93%, with concerns around China’s intentions on cooling iron prices a hindering factor following Premier Li Keqiang comments on the bulk commodity halfway through the week. Iron ore prices on the Singapore exchange closed the week at $198, well down from the mid-week peak above $230. From a historical perspective, prices of course remain at extremely elevated levels and some cooling is probably not a bad thing.

GBP was the outperformer on the week, up almost 1% ad ending the week just above the 1.41 mark. Meanwhile the euro was little changed on Friday and on the week and it starts the week at 1.2141.

Oil prices continued their rebound on Friday, gaining over 2% on the day and closing the week up around 0.8%. Copper had a down day on Friday and like other metals lost a bit of ground over the week, although prices remain close to recent highs.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.