Long-term signal vs. Short-term noise

Insight

Republican ‘red wave’ failed to materialise, but still expect slim House majority

The Republican ‘red wave’ failed to materialise on Tuesday. Republicans are only expected to gain a slim House majority, while control of the Senate looks like it won’t be known for some time with a run-off in Georgia – currently Republicans are on 49, Democrats on 48, and 3 races in Arizona, Georgia and Nevada are too close to call; Georgia is set for a run-off election on 6 December 2022. While the outcome is much closer than expected, it is still consistent with policy gridlock, but perhaps not as much debt ceiling angst as previously with moderate Republicans able to have some influence as well, and US military support for Ukraine also looks like it will be less contested in a close Congress.

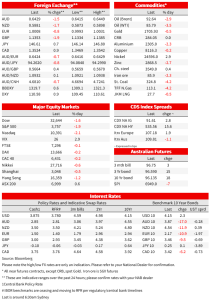

As for markets, risk appetite is certainly lower (at time of writing S&P500 -1.9% and USD DXY +0.9%; note US equities now close at 8.00am Sydney time), but this looks more like a partial reversal of recent moves ahead of US CPI tonight. Spill over from the meltdown being seen in crypto where sources suggest Binance seems unlikely to complete a de-facto bailout of FTX is also evident with NASDAQ -2.2%. For crypto the likely failure of FTX highlights that there is no lender of last resort in crypto! Unlike in state-issued fiat currencies where central banks play that role. Unsurprisingly big falls have been seen in the crypto space with Bitcoin -9.9% to $16,750, and Ethereum -13.0% to $1,190.

In rates, US Treasury yields are broadly flat. The 10yr is +2.3bps to 4.13% with a little bit of volatility given the lower risk appetite overnight (low was 4.09% before a 10yr auction which tailed more than three basis points above the when-issued yield with a fall in coverage and indirect bidding). 2yr yields are also barely moved at -2.4bps to 4.62%, and the 2/10s curve sits at -47.7bps. Underneath the nominals, the implied 10yr inflation breakeven fell -5.3bps to 2.44%, largely in sympathy with the fall in oil prices with WTI -3.5% to $85.79. Oil fell as US crude stockpiles rose 3.93 million barrels, climbing to the highest since July 2021, while Chinese growth concerns continue with covid cases on the rise and China still holding to zero-Covid in the near term. As for real yields, the 10yr TIP yield rose 7.0bps to 1.69%. The major driver for rates in the session ahead will be US CPI tonight.

As for FX, the USD is broadly stronger with DXY +0.9% and recovering some ground after three days of losses. GBP remains one of the more volatile major currencies and is down 1.9% overnight to below 1.14 (currently 1.1353). Both the AUD and NZD have seen losses of about 1.5-1.7% over the past 24 hours, though in levels the AUD at 0.6429 is still holding on the levels it saw late last week when Chinese re-opening rumours swept markets. As for the other majors, EUR -0.8% to 1.0008 and USD/JPY +0.7% to 146.61.

US growth looks still too strong to bring inflation down with the Atalnta Fed GDP Now estimate for Q4 revised up to 4.0% annualised from 3.6% last week. The upward revisions include data from last week’s payrolls report and from last night’s wholesale trade report (wholesale inventories were 0.6% m/m vs. 0.8% expected). The WSJ’s Fed Whisperer Timiraos (in remarks that are not sourced as far as your scribe can tell) noted some analysts “now, more are seriously considering whether the central bank’s target rate will rise as high as 6% before Fed officials take their foot off the brake—a level not reached since just before the dot-com bust in 2000, and one that could spell far more pain ahead for stocks and bonds”. (See WSJ: Some Investors Bet Fed Could Lift Rates to Two-Decade High). The ongoing resilience in the data and stickiness in inflation continue to point to the Fed hiking rates closer to 5% or higher. Markets currently price a peak of 5.09% by mid-2023.

There was little in the way of market-moving Fed commentary. The NY Fed’s Williams in Zurich commented that “longer-run inflation expectations in the United States have remained remarkably stable at levels broadly consistent with the [Federal Open Market Committee’s] longer-run goal” but did not comment further on monetary policy. The Fed’s Barkin, who we have heard a lot from recently, re-iterated his support for downshifting to the pace of hikes (“I like the idea of going slower for longer to a potentially higher place, because it will give you time to read the data and what you’re learning from contacts and react appropriately”). Barkin also continued to suggest the peak in rates “may well” peak higher than previously forecast and “getting to normal may lead to a downturn.” As noted above the market is already there with markets pricing in a peak of 5.09% by mid-2023. The question now is given the resilience in the data, are Fed officials thinking of an even higher peak.

In Australia, the RBA Deputy Governor Bullock’s remarks last night were not that different to the details given in the latest SoMP. In Q&A though (and in answer to a fee question from your scribe), Bullock highlighted the RBA is taking a different approach to other central banks (not doing a Volcker) and said, “We’re very committed to getting back down to target, but we have a flexible inflation target for a reason,” … “You could scorch the earth and get inflation back down very quickly – is that the right thing to do? Or is better to try and preserve some of the gains while you bring it back down?”. That said, when pressed on the credibility of the inflation target, Bullock noted: “If we have some particularly bad news on inflation, or for all the reasons we think we might be different on wages it turns out we’re not, then don’t doubt our resolve to increase your interest rates quite quickly.” (For details, see AUS: RBA’s Bullock emphasises flexibility in the RBA’s inflation target but elsewhere adds little on top of SoMP messaging).

There was little in the way of other data overnight. In Asia yesterday CPI and PPI printed in different directions, but both pointed to fairly subdued inflationary pressures as zero-Covid continues to hamper any stimulus measures from gaining traction. CPI rose 2.1% y/y vs. 2.4% expected, while the PPI was -1.3% y/y vs. -1.5% expected. As for Covid, infections are on the rise with cases in Beijing the highest in more than five months. China will have to confront the substantial cost of zero-Covid as infections continue to spread with community transmission on the rise according to The Beijing Center for Disease Control. The substantial economic cost will fuel speculation of China planning to pivot away from zero-Covid, though given the impending winter a more comprehensive pivot is probably still not likely until the Spring (March/April) according to most analysts.

NAB Markets Research Disclaimer

Long-term signal vs. Short-term noise

Insight

Join us as we discuss interest rates, general economic conditions, and the NAB AUD/USD forecast

Webinar

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.