NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Dovish Fed Official (Daly) flips to looking at accelerating tapering and to hikes in 2022

https://soundcloud.com/user-291029717/is-the-us-getting-too-hot-to-handle?in=user-291029717/sets/the-morning-call

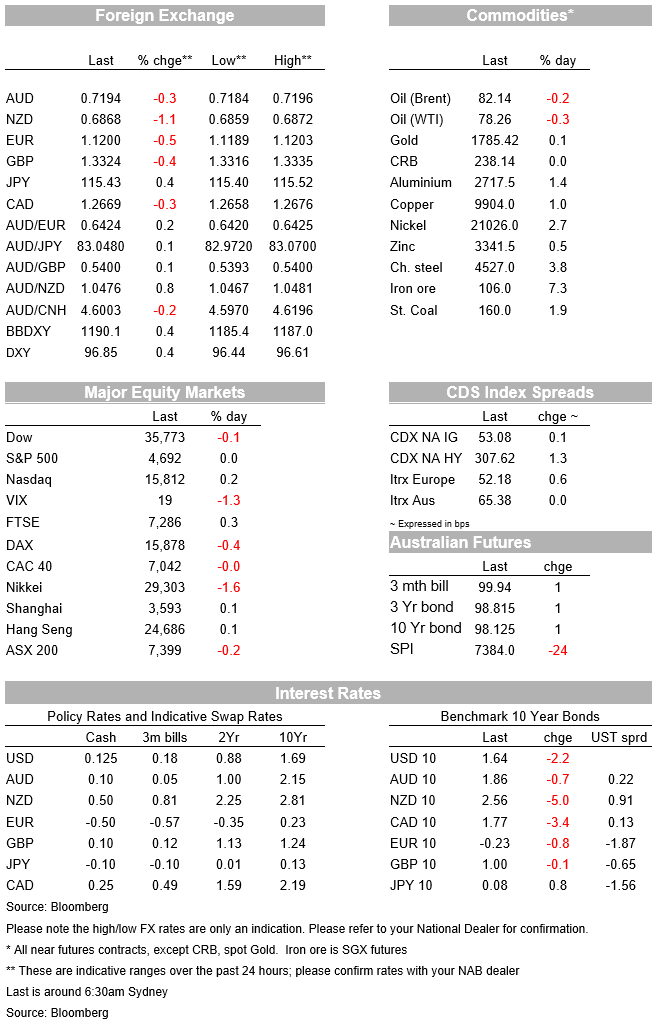

The US economy retained its titanium status overnight with a slew of better than expected data pointing to a re-acceleration in growth in Q4. Notably US Jobless Claims (199k vs. 260k) fell to their lowest level since November 1969 and although seasonal factors likely exaggerated the fall, the overall message is still the same. The slew of better than expected data saw the Atlanta Fed’s GDP Now estimate rise to 8.6% annualised for Q4, well up on the 2.1% recorded for Q3. Yields rose in the wake of the data with the moves led by the short-end. Over the past 24hours US 2yr yields are up 3.3bps to 0.64% with the 2/10s curve flattening by 5.5bps to 100.1bps. The 10yr yield ended lower by 2.2bps to 1.64% with reported squaring up of some short positions ahead of Thanksgiving. The implied inflation breakeven was unchanged at 2.62% with real yields drifting lower to -0.9975%. Slightly hawkish comments from the normally dovish Daly was also a factor. The USD rose again with the DXY +0.4% and at a 16m high.

First to the slew of economic data. US Jobless Claims fell to 199k, well below the 260k consensus and 270k recorded the prior week. Favourable seasonal factors likely exaggerated the extent of the fall, but the overall message of a strong labour market as seen in JOLTS is still there. Separately released job ads data from Indeed showed the level of ads are 52% above pre-pandemic February 2020 levels. Personal Income/Spending data was also stronger than expected with income +0.5% m/m (consensus 0.2%) and spending +1.3% m/m (consensus 1.0%). Clearly the US consumer is spending despite concerns around inflation and stands in contrast to the final University of Michigan Consumer Sentiment numbers which had the 5-10yr inflation expectation revised higher to 3.0% (from 2.9%) with consumer sentiment at 67.4% (consensus 66.9) still not recovering from its sharp fall in August. Other data out included durable goods orders with the core series lifting 0.5% m/m as expected and the trade deficit coming in lower driven a rebound in expects (deficit $82.9bn vs. 95 expected)

Interestingly the PCE figures confirmed inflation pressures appear to be broadening with the separately released Dallas Fed Trimmed Mean PCE lifting to 2.6% y/y from 2.3%, its highest rate since 2008. Note the headline core PCE was as expected at 4.1% y/y. The broadening of inflation pressures is important and has been one factor driving more FOMC officials to consider whether to accelerate the taper profile and whether to lift rates multiple times in 2022. The Fed’s Daly was the latest on the road to Damascus conversion, noting: “the inflation numbers, after coming down for a few months on the monthly basis, the CPI monthly numbers were high again…And so if that continues, then those are the things that would say, looks like we need faster tapering”. Daly also said she was “leaning towards” the need to raise rates at the end of next year and “ wouldn’t surprise me at all if it’s one or two by the latter part of next year”.

The FOMC Minutes which were just released as your scribe is typing re-iterated a similar theme with “some” participants at the November meeting already seeing the case for a faster taper than what was decided, and that the commitment to re-visit the taper profile was real with the FOMC prepared to “adjust the stance of policy as appropriate in response to changes in the Committee’s outlook for the labor market and inflation”. Importantly the FOMC not only saw the possibility of a faster taper profile, but they would also be prepared to “ raise the target range for the federal funds rate sooner than participants currently anticipated if inflation continued to run higher than levels consistent with the Committee’s objectives” (see FOMC Minutes and the Fed’s Daly for more).

In other overnight news, Olaf Scholz, the current Finance Minister, looks set to become the next German Chancellor, after coalition negotiations amongst a three-way alliance of the Social Democrats, Greens and Free Democrats. A three-party government is a first for Germany and it remains to be seen how well it can function, but a key proposal includes returning to the constitutional debt limits by 2023 and climate change policies will be a top agenda item. After yesterday’s move by the US and others to release oil from their strategic reserves amid high oil prices, the WSJ reports that Saudi Arabia and Russia are considering a move to pause their OPEC-led agreed production increases. Brent crude pushed higher, to USD83 per barrel before falling back to flat on the day, after yesterday’s solid 3+% increase.

Strong US data and higher short rates have given the USD another boost, seeing the key dollar indices up 0.4% to a fresh 16-month high. EUR has broken below 1.12, with the US data and the underwhelming Germany IFO survey reinforcing the positive US versus Eurozone economic surprise relativity of late. USD/JPY printed a 4½-year high about 115.50, while GBP printed a new low for the year near 1.3320.

The commodity currencies, excluding the NZD, have shown a little resilience overnight, but this still sees the AUD down to around 0.7190. The NZD weakened after yesterday’s RBNZ MPS and USD strength has dragged it lower overnight, currently trading near its lows for the day below 0.6860, but ahead of the low for the year in August of 0.6805, a level which will be widely seen as technical support. Key NZD crosses are all lower. As for the RBNZ, there were no surprises in the 25bps hike. The RBNZ noted that the OCR would likely need to be raised above its neutral rate, seen to be about 2%, and projected a terminal OCR of 2.6%. MPC discussed whether a faster tightening path was required and considered whether a 50bps hike was appropriate at this meeting. But the Bank noted the uncertainty about how the country adapts to living with COVID19 across the country and the tightening in monetary conditions already evident in higher mortgage and business lending rates. With the market pricing in a 34% chance of a larger 50bps hike going into the meeting, the natural response was a decent rally in rates, led by the short end of the curve.

Domestically we have Capex and ABS Payrolls data which are unlikely to be market moving. ABS Payrolls should show a sharp recovery in jobs with NSW, VIC and ACT coming out of lockdown in October. Offshore it is very quiet given the US Thanksgiving Holiday with only a smattering of ECB and BoE speakers. Details below:

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.