Total spending grew 0.9% in June.

The positive vibes evident during our trading session yesterday have extended overnight with European and US equity indices higher on the day. Movements in rates and FX markets have been more subdued. The USD is a tad stronger in index terms with JPY the notable underperformer. AUD and NZD are also lower with the former not helped by a yesterday’s softer than expected monthly CPI print.

Events Round-Up

AU: CPI (y/y%), Feb: 6.8 vs 7.2 exp.

GE: GfK consumer confidence, Apr: -29.5 vs -30 exp.

US: Pending home sales (m/m%), Feb: 0.8 vs -3.0 exp.

The positive vibes evident during our trading session yesterday have extended overnight with European and US equity indices higher on the day. Movements in rates and FX markets have been more subdued, 10y UST yields are essentially unchanged at 3.55% while 10y Bunds are the notable movers up 4bps ahead Germany’s CPI tonight. The USD is a tad stronger in index terms with JPY the notable underperformer. AUD and NZD are also lower with the former not helped by a yesterday’s softer than expected monthly CPI print.

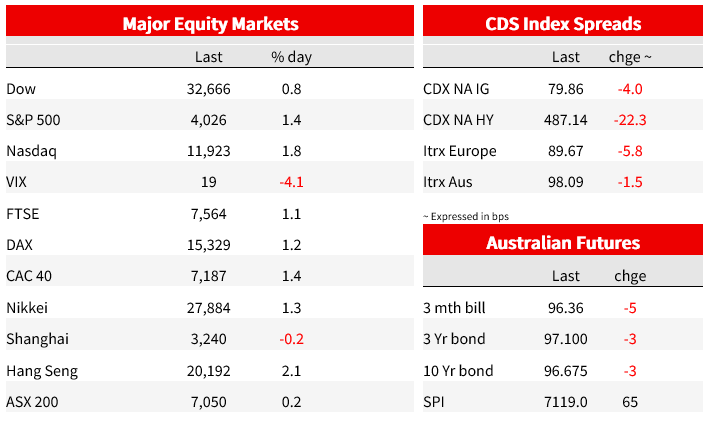

The lack of new news has seemingly been a positive for equity investors while gains seen during our APAC session extended into Europe and the US overnight. Yesterday Asian equities (particularly the tech sector) were boosted following the previous days news that Alibaba plans to split into six units and seek separate listings. Its Hong Kong-listed shares were 12% higher, tracking the previous night gains on Wall Street. Gains in Alibaba also sparked a rally in Chinese tech shares with many analysts speculating the Alibaba decision could instigate other big tech companies to follow a similar move, Alibaba’s plan is also expected to instigate an ease in regulatory crackdown from Beijing.

Main European equities indices closed higher on Wednesday, all up between1.07% and 1.6%. The improvement in risk appetite was also evident by the decline in the VIX index, after gapping lower at the open the VIX index has spent the whole session below 20. US equity indices also look set to close the day in positive territory with the S&P 500 currently up by 1.46%. All 11 sectors in the S&P 500 are trading in the green with IT (1.96%) , Real Estate (1.73%) and Consumer Discretionary (1.65%) leading the charge. Of note too and as a sign of an ease of concerns over the banking sector, the KBW index is up close to 1.5% as I type. Finally, not to miss out on the party, the NASDAQ +1.79% and with one day left in the month the index looks set to record its best quarter since 2020. Not bad given concerns of a banking crisis and expectations of an imminent US recession.

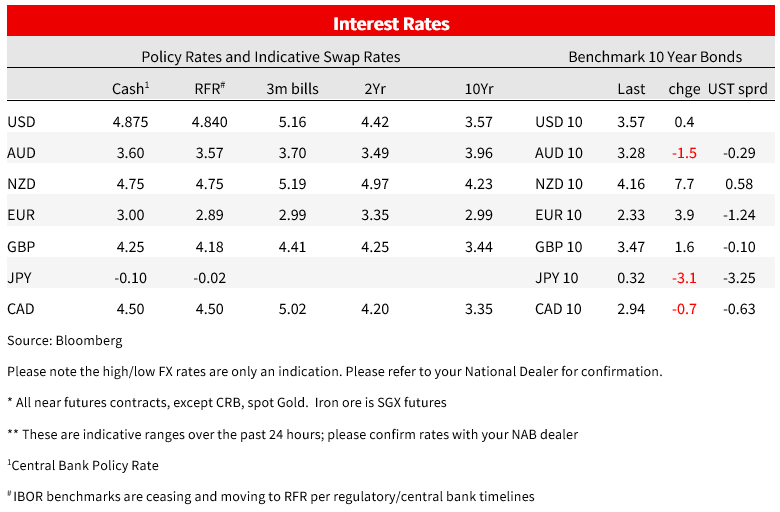

Core global yields have had a subdued overnight session with changes in the UST curve relative to levels this time yesterday limited to within 1bps. The 10y UST yield is unchanged at 3.56% while the 2y rate is 1bps lower at 4.08%. On the US data front, US pending home sales rose 0.8% in February, against expectations of a 3.0% decline. This is their third consecutive monthly increase suggesting the US housing market may have been starting to find its feet ahead of the recent banking turmoil. Sales were still down 21.1% y/y.

Speaking before lawmakers in Washington, Fed Chair Powell was asked when the central bank will stop raising interest rates. Powell noted that the Fed forecast shows another quarter percentage-point hike this year. Fed pricing expectations are little changed, with a roughly even chance of a 25bp hike priced for the next meeting in May and cuts priced by the end of the year.

ECB Lane also spoke overnight, his initial comment that Euro-area inflation was set to decline rapidly at year-end triggered a small rally in core European bonds, but then the moved morphed into a bear flattening with Lane noting the ECB will need to increase interest rates further if, as expected, recent tensions in the financial system stay contained . 2y Bunds ended the day 7bps higher at 2.63% while the 10y rate gained 4bps to 2.32%. The OIS market is pricing 19bps of hikes for the May 4th meeting with an effective cash rate seen picking at 3.88% by late October. In other words, the market is well priced for two 25bps hikes taking the deposit rate to 3.5% before year end with a small chance of a rate cut early next year.

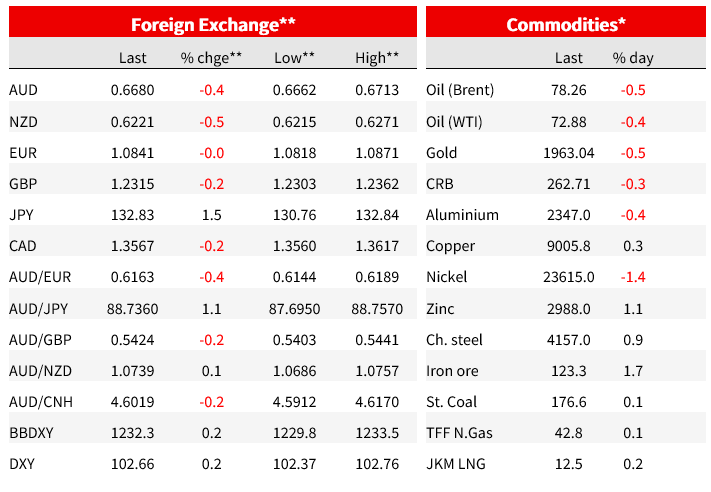

Moving onto FX, the USD is stronger in index terms with both BBDXY and DXY up by around 0.2% and within G10 pairs, JPY is the notable underperformer down ~1.5% with USD/JPY starting the new day ¥132.85. JPY has regained some of its safe-haven attribute in the recent bank turmoil, now with concerns easing somewhat, JPY is weaking along with an improvement in risk appetite. Yesterday, speaking before Parliament, BoJ’s new Deputy Governor Shinichi Uchida indicated the bank shouldn’t communicate its policy decision in advance including any changes surrounding its yield curve control program, as it’s decided by a policy board meeting. Uchida then concluded that the decision should come as a surprise adding that “Due to the nature of the yield curve control, it’s hard to get markets price in a change beforehand,”.

The euro is little changed at 1.084, showing little reaction to ECB Lane’s comments and the move up in Bund yields. CAD is the notable USD outperformer with an uptick in short dated Canadian bond yields supporting the loonie. Speaking overnight BoC Deputy Governor Toni Gravelle said the Bank of Canada is monitoring global financial system turmoil closely but doesn’t see anything concerning domestically.

The AUD ( -0.43% @0.6680) and NZD (-0.51% @0.6221) have struggled a little over the past 24 hours, but both continue to trade within recent ranges. Looking at the intraday chart the AUD was not helped by the softer than expected monthly CPI print with an early move above 0.67 proving short lived. Yesterday’s Australian monthly CPI indicator for February showed 6.8% annual inflation. It is a step down from January’s 7.4% and was noticeably lower than expectations at 7.2%. While only one month’s data, and incomplete coverage compared to the full quarterly CPI, for next week’s RBA meeting it leaves the risk of a pause. Other data like the recent employment data and the NAB business survey would suggest it is too early to pause. Market pricing is consistent with an RBA pause next week and a cut by the end of the year. AU rates and AUD fell post release.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.