Total spending grew 0.9% in June.

The US and Australia have both reported dour job numbers, although markets were braced to expect it.

https://soundcloud.com/user-291029717/job-woes-trump-tensions-and-chinas-rebound?in=user-291029717/sets/the-morning-call

Used to feel we had it made. Used to feel we could sail away….It’s so funny how we don’t talk anymore – Cliff Richard

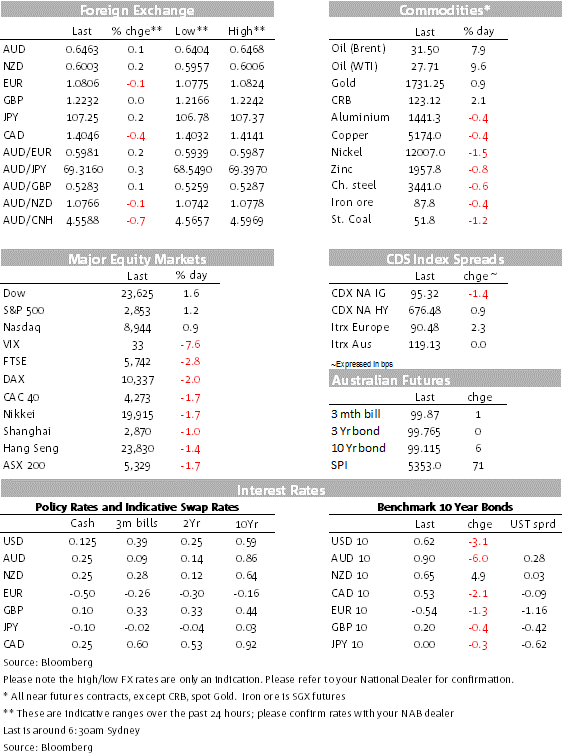

A bigger than expected US jobless claims number along with souring US-China vibes weighed on US equities at the open, but later in the session US banks led a recovery helping US equity indices close in the green. A late reversal in the USD has aided the AUD and NZD recover yesterday’s losses. The UST curve bear flattened with the 30y bond down 5bps to 1.30% and oil prices enjoy a strong rebound.

There used to be a time when President Trump and President Xi wrote beautiful letters to each other. Back in January, Trump talked about his love for Xi, but now he seems to be losing that loving feeling. In a Fox news interview, President Trump said he didn’t want to talk to President Xi right now and he wondered out aloud what would happen if the US cut off its “whole relationship” with China, “…you’d save $500m”. Trump was also “looking at” Chinese companies that trade on US bourses but do not follow US accounting rules. This has followed recent news of the US extending its ban on Huawei for another year, Trump blaming China for the “plague” (COVID19), and the US retirement fund for federal workers deferring a change in its new benchmark for international equities that would include Chinese stocks.

Heightening US-China trade tensions didn’t help market sentiment while a weaker than expected US jobless claims number also played into the US equity underperformance in the early stage of the NY session. US initial jobless claims for last week were higher than expected, taking the cumulative total to 36m workers over the past eight weeks. That the trend rate of increase is slowing is only a small consolation to the dire state of the US labour market. US rates have drifted lower, seeing the US 10-year Treasury getting down near 0.60%, now currently just above that level and down 4bps on the day.

Germany projected a bigger than expected fall in tax revenues (€98bn), raising doubts over Germany’s willingness to contribute money for an EU fiscal stimulus, the Stoxx Europe 600 Index closed 2.2% down, its biggest two-day drop in two months with all sub sectors in the red.

Equities enjoy a recovery with financial stocks leading the charge. Wells Fargo (+7.79%) was the outstanding outperformer within financials while the energy sector was also boosted by a decent rebound in oil prices ( WTI +9.2% and Brent +6.78%). News that OPEC+ reduced exports by 5.96m/b a day for the first 14 days of May, according to Petro-Logistics helped the positive vibes in oil. Meanwhile the move up in financial was less clear although talks of further stimulus potentially played a part. White House press secretary Kayleigh McEnany told Fox News that President Trump is open to more coronavirus relief legislation, but he’s opposed to the stimulus measure drafted by House Democrats.

It was an up and then down session for the USD, leaving it little changed in index terms. DXY now trades at 100.28 and BBDXY is at 1253. Of note the USD is broadly weaker against EM FX (EMCI +0.44%) with MXN (1.32%) and BRL (1.22%) the outperformers.

CAD is at the top of the leader board +0.36% to 1.405. The move up in oil prices has been one supporting factor for the Loonie while a cautiously optimistic BoC report also helped. In its annual Financial System Review the BoC noted that Canada’s financial system remains resilient even in the face of the Covid-19 pandemic and moves to keep credit markets functioning have been largely effective, though risks remain.

Yesterday the AUD came under pressure following a labour market report that had a better than expected headline number masking very weak underlying information. Australia’s Unemployment rate only rose to 6.2% from 5.3% vs. 8.2% expected (NAB 9%) but ABS says that if those who were measured as having left the labour force in April were instead counted as part of the workforce, unemployment would have hit 9.6%. Furthermore, hours worked fell by 9%, so not only there has been a marked increase in people not working, on aggregate people that still have jobs are also working less. Overnight the AUD traded down to a low of 0.6404, but late in the session the improvement in risk appetite and broad USD weakness helped the pair more than erase its losses over the previous 24hrs. The AUD now trades at 0.6462 (0.20%) and remains well entrenched within its 0.6337-0.6570 range held since April 24.

Job ads plunged by 65% y/y in April, as the country entered the severe alert level 4 lockdown. But the feature of the day was the NZ Budget, which showed that the government wasn’t holding back with its COVID19 fiscal response, with an additional $50b of spending on top of the $12b already announced. This takes the total response to some 20% of current nominal GDP (and ultimately larger on this metric, as the economy will be some 20% smaller at its nadir).

Under normal circumstances, prospects of such a large fiscal easing would be NZD-positive. After a down and up session NZD now trades at 0.6002, up 0.20% over the past 24 hours. The move lower in the NZD over the past couple of days has broken the slight upward trend (evident in higher lows over the past couple of months), but the pair is still well within the familiar 0.5840-0.6170 range.

Bank of England Governor Bailey said that the Bank isn’t currently considering lowering interest rates below zero, as it would prove difficult for banks. The BoE joins the other group of wise central banks – the Fed and RBA – deciding that negative rates can do more harm than good, with the experience of the euro area and Sweden noteworthy in this regard. Bloomberg noted comments by BoJ Governor Kuroda yesterday that lowering interest rates (taking the policy rate below zero) was lower down the pecking order as he rattled off the Bank’s further possible policy options, with rates coming after further QE and market operations.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.