Online retail sales growth slowed in May following a fairly strong April

Insight

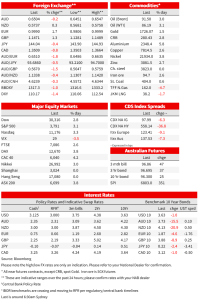

Yesterday 25bps RBA cash rate rise, defied the broad consensus among economists and investors (~45bps was priced in for the meeting) but which was justified by the Board in part on the premise that “the cash rate has been increased substantially in a short period of time”.

October and Q4 has certainly got off to a good start for risk assets after a miserable September. While the moves up in equities (and down in bond yields) might yet prove to be no more than the product of poor poisoning/extreme equity market bearishness into the end of Q3 and bad (short) positioning in bonds, there are undeniably a few kernels of (US) data – JOLTS the latest – playing to the view the Fed could be done tightening before Christmas. The USD is hating the risk rally and pull-back in US Treasury yields, the fall in the DXY index since last Wednesday’s new cycle high comparable to what we saw back in May (-3.6%) and July/early August (-4.3%) – both of which proved to be false downside breaks from the prevailing uptrend.

Yesterday 25bps RBA cash rate rise, defied the broad consensus among economists and investors (~45bps was priced in for the meeting) but which was justified by the Board in part on the premise that “the cash rate has been increased substantially in a short period of time”. It elicited a dramatic fall in local bonds yields but only a limited reaction in the AUD. AUD/USD initially fell from just above 0.6500 to a low of just above 0.6450 but ended the Sydney day virtually unchanged before rallying to a high just shy of 0.6550 in London. Surprising, but perhaps not as much when we consider that in most instances where central banks (bar the Fed) have exceeded market expectations on the hawkish side in policy decisions for much of this year, they have tended to be rewarded with weaker not stronger currencies on the day.

On one argument, growth expectations (not now so bad in the case of the Australia?) matter as much as yield considerations when it comes to currencies. In truth, the rapidly weakening USD has something to do with the AUDs relative resilience. Looking across the whole G10 currency spectrum this morning, AUD/USD is the only currency not to have risen against the USD (currently -0.3% heading into the New York close, against gains of 1.6% for EUR/USD, 1.2% for GBP/USD and 0.4% for the NZD. So, yield considerations clearly do count for something

The USD’s significant move lower since making a new 20+ year high last Wednesday, is an entirely logical response to the combination of smartly lower US bond yields and much improved risk sentiment following, for example, the 17% high-to-low drop in the S&P 500 between mid-August and end September. Higher yields and deteriorating risk sentiment have after all been the key fundamental drivers of the USD’s rally dating right back to mid-2021. In context though, the 4.1% drop in the DXY index since last Wednesday’s high is comparable to the May (-3.6%) and July though early August sell offs (-4.3%) both of which of course proved to be false breaks to the downside. Others more technically expert than this mere macro mortal may beg to differ, but simply looking at the trend lines, not enough damage has yet been done to the dollar to enable a top to be called with a reasonable degree of confidence.

There is no denying incoming US economic data is having a hand in equity, bond and currency moves so far this week. Following Monday’s weaker than expected ISM Manufacturing survey, overnight the JOLTS US job openings report sprang a big downside surprise , August openings falling to 10.05 million from a slightly revised 11.17mn in July. This was the biggest monthly fall since April 2020. It’s a release that historically has attracted more attention from the Fed than markets (it used to be a Janet Yellen favourite) but the size of the sheer fall couldn’t be ignored, especially given Fed Chair Powell’s recent focus on the job openings-to-unemployed ratio. This fell from 1.97 (i.e., almost two job openings per unemployed person) to 1.67 in August, the first meaningful sign of some cracks in the labour market. To be clear, the absolute levels are still consistent with a very tight labour market and the data can be prone to significant revision, but the Fed will undoubtedly welcome the tentative signs of easing demand for labour.

In the bond market , US Treasury rates were significantly lower at one point, the 2-year rate falling from 4.11% to 3.99% and 10s from 3.64% to 3.56%, but these moves have mostly reversed over the past few hours, 2s currently back at 4.1% (so down just 1bps ion the day) and 10s at 3.62% (0-2bps). Europe and the UK both saw lower rates overnight, the UK 2-year rate falling another 10bps as the rebound in the GBP caused the market to scale back its expectations for a jumbo rate hike by the BoE in November (‘only’ 110bps now priced in for that meeting, from above 1.5% at one-point last week). The latest signs of a U-Turn on government policy, following the decision not to proceed with the cut in the top rate of income tax from 45% to 40%, is that the lifting of the cap on bankers bonuses (an EU initiative back when Britain was a member) may not now go ahead. Blind Freddy could have told the British PM and Chancellor that was never going to be a vote winner.

In equities, another ‘jolt’ higher has come from new that Elon Musk will now proceed with his previously planned purchase of Twitter and reportedly at the originally agreed price. Twitter’s share price is currently +21% on the day, leading the NASDAQ to a 3.3% gain while the S&P500 has just closed in new York up 3.1% All S&P500 subsectors are in the green, with IT +3.3%, financials +3.8% and consumer discretionaries, the recent underperformer on the deepening recession worries, +3.6%. But it is energy (+4.4%) that leads the pack, in conjunction with a 3% jump in crude prices, this on news that tonight’s OPEC+ meeting of oil ministers is looking to agree a production cut of as much as 2 million barrels per day.

NAB Markets Research Disclaimer

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.