Total spending grew 0.9% in June.

Mid-morning in Friday’s US trading day, Bob Kaplan said he may rethink his call for the Fed to quickly start to taper its $120 billion per month in bond purchases if it looks like the spread of the coronavirus delta variant is slowing economic growth. This didn’t have a big impact on bonds, but we can date the start of the run-up in US equity indices and a pull back in the USD to his comments hitting the screens, testament to the ongoing sensitivity the currency and risk markets are exhibiting to the question of when QE tapering starts.

https://soundcloud.com/user-291029717/kaplans-hawkish-wings-are-clipped?in=user-291029717/sets/the-morning-call

Mid-morning in Friday’s US trading day, Dallas Federal Reserve President Bob Kaplan, who together with St. Louis Fed President James Bullard is currently one of the two most hawkish FOMC members, said he may rethink his call for the Fed to quickly start to taper its $120 billion per month in bond purchases if it looks like the spread of the coronavirus delta variant is slowing economic growth. “The thing that I am going to be watching very carefully over the next month, before the next [Fed] meeting, is [whether] it is having a more material impact on slowing demand and slowing GDP growth. I’m going to keep an open mind on that, and if it is having a more negative effect that might cause me to adjust my views somewhat from ones that I’ve stated,” he said.

This didn’t have a big impact on bonds, but we can date the start of the run-up in US equity indices and a pull back in the USD to his comments hitting the screens, testament to the ongoing sensitivity the currency and risk markets are exhibiting to the question of when QE tapering starts. Arguably the FX market exhibited a form of ‘taper tantrum’ of its own last week following the release mid-week of the July FOMC Minutes hinting that a decision on tapering was close. Of course, if tapering is to come later than otherwise because of the impact the spread of the delta covid variant is having on US (and global) economic activity and to which even the most ardent Fed hawks can subscribe to, this can just as easily play out USD positive as negative, from a risk sentiment/safe-haven USD demand perspective.

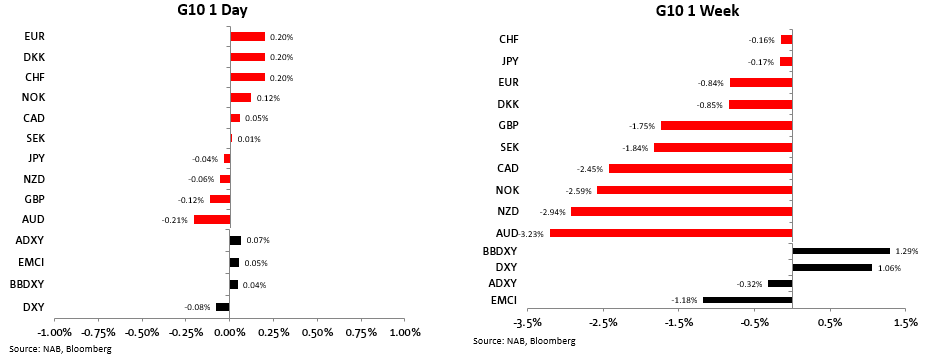

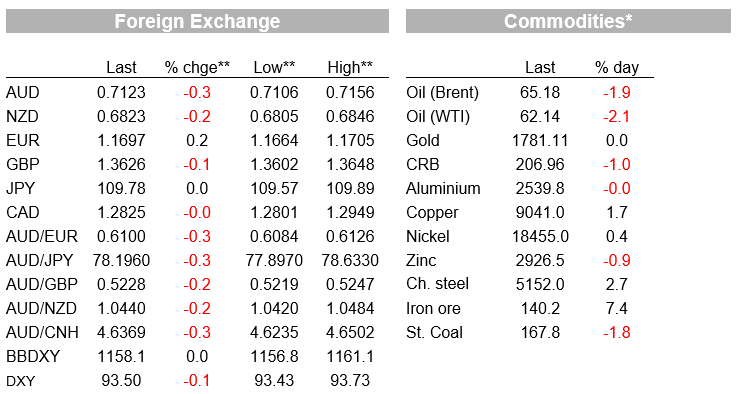

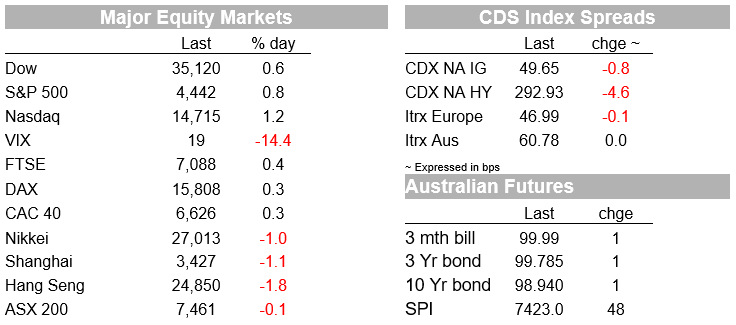

Let’s see what Fed chair Jay Powell has to say when he speaks at the (now virtual) Kansas City Fed annual symposium at 10am US Eastern Time this Friday , on the topic of the economic outlook. Anticipation of his speech, and whether he too will play up near term downside economic risks due to the spread of the delta covid variant, has the potential to see somewhat less tumultuous market activity this week. This is after a very negative APAC session during which both the Hang Seng and Shanghai Composite indices lost the best part of 2% and the AUD came perilously close to shifting down onto yet another new ‘handle’ (0.70) having begun the week not far off 0.7400. AUD made a new YTD low of 0.7106 offshore and the late Friday recovery was anaemic to say the least, such that it remains premature to call an end to this down move. Certainly the weekend news of new record numbers of covid cases in New South Wales on both Friday and Saturday, both in excess of 800, has done nothing to improve sentiment towards the AUD at the start of the APAC week. Ditto the NZD with New Zealand reporting 21 new cases across Saturday and Sunday.

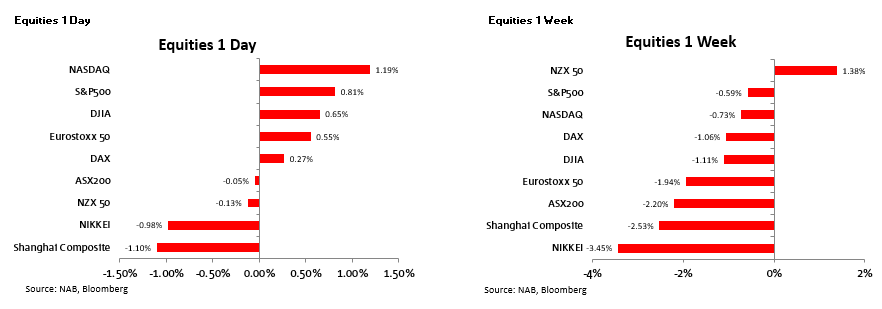

So in the end Friday’s northern hemisphere equity markets didn’t display any of the earlier APAC session weakness, the Eurostoxx 50 finishing +0.6% , the S&P500 +0.8% and the Nasdaq +1.2%. Some signs of sector rotation into defensive and technology stocks were evident (e.g. utilities and IT fared best within the S&P) though the domestic demand-centric Russell 2000 rose by 1.6% to be the best performing US index, so it was not all about rotation. On the week, The Hang Seng and ASX 300 were the worst performing indices globally, both off by more tha 5%. On the Hong Kong and Shanghai stock markets, investors remain wary about the regulatory crackdown by the Chinese authorities, with Xinhua reporting on Friday that a new data protection law had been passed, the latest in a string of regulatory actions aimed largely at the tech sector.

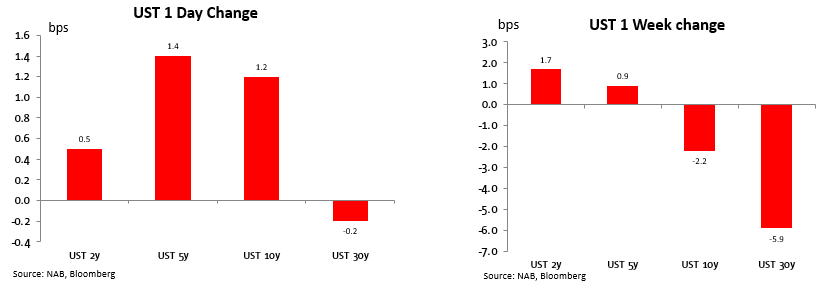

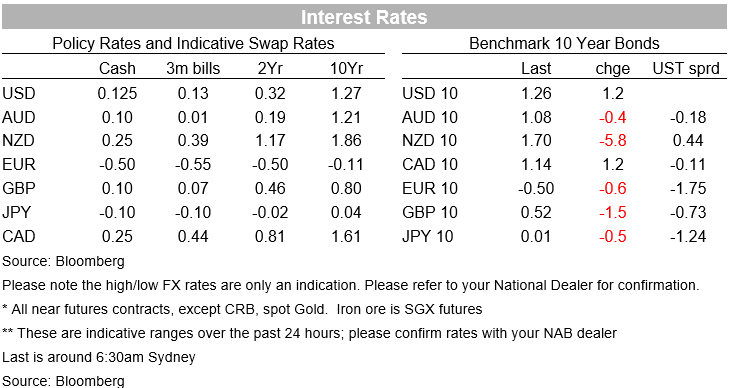

In bonds , not much movement in Treasuries anywhere along the curve Friday (the belly faring worse with yield rises of 1.4 and 1.2% in 5s and 10s respectively, while on the week the curve flattened, 2/10s by 4bps and 2/30s by 7.5%. (30-year -6bps). The (negative) AU-US 10 year spread widened by a further 12bps to -19.5bps.

FX moves in the 24 hours to Friday’s NY close ended up being quite small, topped and tailed by a 0.2% gain for EUR/USD and 0.2% loss for AUD/USD, the former bringing the DXY dollar index off its week’s highs but still up more than 1% in the week (and the broader BBDXY by a bigger 1.3% and where some contribution came from the back up in USD/CNH through 6.50, a 1% fall in KRW and more so – given its 10% weight in the index, the 2.5% rise in USD/MXN.

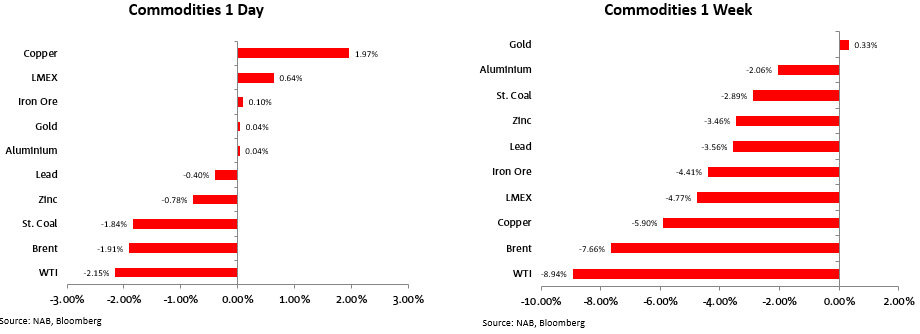

A torrid week for commodities is well illustrated in the below chart, where only gold managed a (small) gain and loses led by crude where WTI was off 9% and Brent 7.7%. Copper’s rally on Friday limited its loss on the week to 5.9%, still the worse performing base, or ferrous, metal (iron ore futures (Singapore) -4.4% after a fairy flat performance on Friday.

Finally, news over the weekend courtesy of Bloomberg that U.S. Treasury Secretary Janet Yellen has told senior White House advisers that she supports reappointing Jerome Powell as Federal Reserve chai r, according to people familiar with the matter, a move that greatly increases his chance for a second term. President Joe Biden hasn’t made a decision yet and is likely to make his choice around Labor Day (6 Sep) the people said.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.