Online retail sales growth slowed in May following a fairly strong April

Insight

The Euro lost ground on Friday as President Lagarde refused to commit to any schedule for talking tapering.

https://soundcloud.com/user-291029717/lagardes-tapering-reluctance-vaccines-winning-against-mutations?in=user-291029717/sets/the-morning-call

“You held me down, but I got up (hey); Already brushing off the dust; You hear my voice, you hear that sound; Like thunder, gonna shake the ground”, Katy Perry 2013

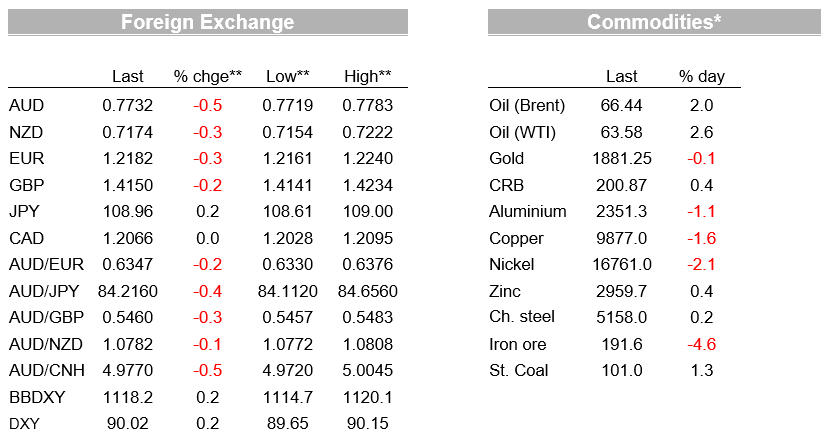

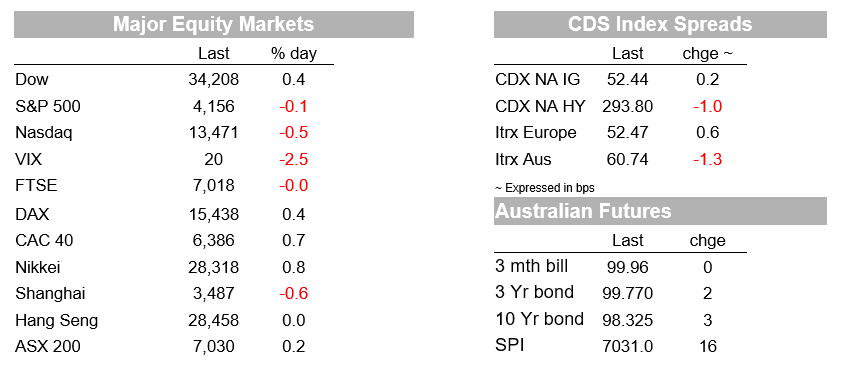

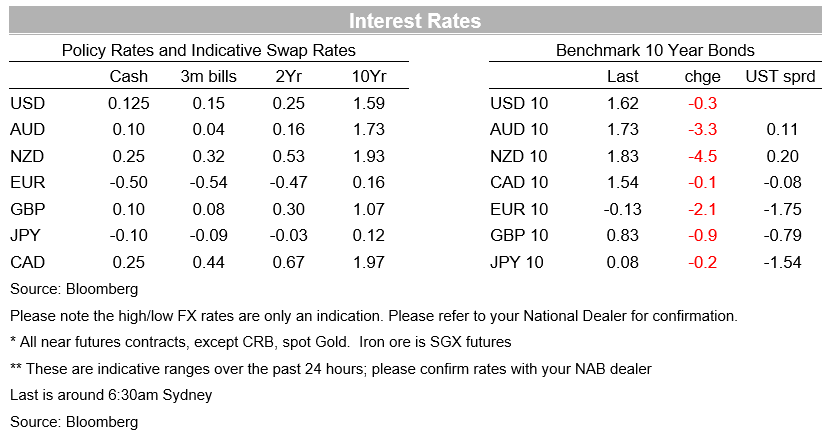

The services sector on both sides of the Atlantic came roaring back in April with the Services PMIs hitting all-time highs in the US and in the Eurozone was at its highest level since 2018. There was little reaction to the data with a more favourable outlook already well priced. Equities were little moved with the S&P500 -0.1%, to end the week down -0.4%. US yields were also little moved on both the day and the week with the 10yr at 1.62%. Looking at breakevens and real yields though reveals an interesting dynamic over the past week with 10yr implied inflation breakevens down -9.6bps to 2.45% and 10yr real yields up +8.6bps to -0.83%. It appears US markets are at least anticipating the Fed to react to inflation surprises and the Fed’s Harker was the latest official wanting to talk about tapering “sooner rather than later”. In contrast, ECB President Lagarde on Friday said it was “far too early” to be talking about tapering, with the EUR falling in response by -0.3% to 1.2182. Lagarde’s comments also appears to have precipitated broad USD strength with BBDXY +0.2%, though across the week BBDXY is down -0.3%. The AUD (-0.5%) and NZD (-0.3%) were again near the bottom of G10FX with the AUD currently trading at 0.7730. As we open for the week eyes will remain on the crypto space with Bitcoin down some 13% to $33,500 as China wards off crypto and the US seeks transparency in Crypto transactions.

First to the economic data. The Services PMI in the EZ, UK and US was overwhelmingly positive and points to activity quickly rebounding as virus restrictions ease. The Eurozone PMI rose to 55.1 against 52.5 expected and 50.5 previously. Manufacturing was also remained strong at 62.8 against 62.5 expected. Across the channel a similar theme was seen in the UK with the Services PMI which rose to 61.8, marginally below the 62.2 consensus. Across the pond the US Services PMI rise to 70.1 against 64.3 expected and 64.7 previously. The rise in the US Services PMI takes it to its highest level in the history of the series that dates back to 2009, while the Eurozone Services PMI is the highest since 2018. The key takeaway for scribe from the PMIs was the reports of input price pressure being passed onto final prices. In the US output prices charged was at the highest since 2009 with record rates of inflation recorded for both goods and services (see US Markit PMI for details). Prices pressure was also elevated in the Eurozone with service sector costs the highest since 2018 and manufacturing the highest in the history of the series. Importantly, average prices charged for goods and services rose at the highest pace since 2002, which is as far as the data goes back in Europe (see EZ Market PMI for details ). Interestingly and playing to supply chain disruptions, Markit also noted activity would have been even stronger had firms not been constrained by supply shortages, including difficulty finding labour.

For markets, the PMIs then should keep inflation fears alive and plays into the view of central banks needing to normalise policy earlier than their official guidance suggests. Philadelphia Fed President Harker echoed that theme on Friday, supporting the need for a tapering discussion “sooner rather than later ”. Importantly Harker appears to have had a ‘Road to Damascus’ conversion on tapering given just two weeks ago he was following the FOMC script of it being too early. That suggests Harker has taken some signal from the recent CPI print and suggest if CPI were to surprise again to the upside, more Fed officials may join. An August Jackson Hole tapering announcement may be looking slightly more likely. Tapering talk had little impact on US yields with the US 10-year rate barely moved on Friday, ending the week at 1.62%. While remaining well contained within its existing 1.50%-1.70% range, there is an interesting dynamic playing out over the past week with 10yr implied inflation breakevens down -9.6bps to 2.45% and 10yr real yields up +8.6bps to -0.83%. Markets it seems are betting the Fed will react to future inflation surprises.

In Europe in contrast ECB President Lagarde pushed back on taper talk. Responding to a question of whether the ECB might taper its bond buying in response to the improved economic outlook, Lagarde replied that “it’s far too early and it’s actually unnecessary to debate longer-term issues”. The market seemed to interpret the comments as suggesting the ECB may not taper its bond buying at its upcoming June meeting. The EUR dropped from around 1.2220 to 1.2180 immediately after Lagarde’s comments, ending the day -0.3% at 1.2182.

The AUD (-0.5%) and NZD (-0.3%) fell in sympathy with the weakness in the EUR. The NZD fell 1.1% last week, ending the week at around 0.7170, the second worst-performing of the G10 currencies (after the oil-sensitive NOK), while the AUD was down 0.5% on the week. The pullback in commodity prices explains the underperformance in the commodity currencies last week, even as the USD itself was generally weaker (Bloomberg DXY -0.3% last week)..

On US fiscal stimulus, the sharp rebound in the US economy continues to reduce the chance of further stimulus. The Biden administration has reduced the size of their proposed infrastructure bill in order to gain support, from $2.3bn to $1.7bn. Republicans and Democratic Senator Manchin continue to push back against the overall size and scope of the package as well as the proposal to increase corporate tax rates to fund it.

Finally vaccine news on Friday and on the weekend was very encouraging with vaccines said to be effective against the India mutation. A study by Public Health England found the Pfizer-BioNTech vaccine was 88% effective against symptomatic disease from the B.1.617.2 variant two weeks after the second dose, while two doses of the AstraZeneca vaccine was 60% effective. The high degree of efficacy as seen the UK continue with its easing of virus restrictions. Meanwhile Israel is said to end all local COVID-19 restrictions after vaccinations in the over 50years category reached 92%. Israel’s international borders though will remain partially closed with a trial to let in a small group of vaccinated tourists beginning. The US is also almost at the same stage with 73.9% of its over 65 years population now fully vaccinated and 49.6% of its total over 18 years population now vaccinated.

Domestically the pre-GDP partials of Construction Work Done and Capital Expenditure are out this week. Neither are expected to be particularly market moving with the consensus for construction at 2.0% q/q and capital expenditure at 2.1%. Forward looking indicators of capital expenditure remain very strong with capacity utilisation at record highs and intentions from the NAB Business Survey also at elevated levels.

Internationally the big pieces for the week are the German IFO on Tuesday, RBNZ meeting on Wednesday (no change), China Industrial Profits on Thursday and the US PCE Deflators on Friday. The US PCE Deflators will be closely watched for any signs of enduring inflationary pressures with consensus for Core at 0.6% m/m and 2.9% y/y, coming on the heels of the Core CPI which printed at 0.9% m/m. The RBNZ meeting will also be watched closely with our BNZ colleagues suggesting the RBNZ will acknowledge the recent strength in economic data, including an unemployment rate which is tracking well below its previous forecast, but retain its cautious messaging around the policy outlook. The clear risk is of course the RBNZ tones down its dovish rhetoric.

It is very quiet domestically with nothing of note scheduled. Offshore it is also very quiet with NZ Retail Sales, BoE officials in front of the Treasury Select Committee, while in the US Fed speakers are on the circuit with the Fed’s Brainard, Mester, Bostic and George all at separate events. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.