S&P 500 rout set to extend for a fourth day in a row

UK Gilts lead sell off in core global bonds.10y gilts +17bps, 10y UST +10bps

German IFO improves for a third consecutive month

US Homebuilders (NAHB) survey falls again, against expectations for an improvement

USD mildly softer. AUD (almost) back above 67c

Coming Up: NZ Business Survey, RBA Minutes, CH LPR, BoJ, US Housing starts

Events Round-Up

NZ: Westpac consumer confidence, Q4: 75.6 vs. 87.6 prev. NZ: Performance of services index, Nov: 53.7 vs. 57.1 prev. GE: IFO business climate, Dec: 88.6 vs. 87.5 exp. US: NAHB housing market index, Dec: 31 vs. 34 exp.

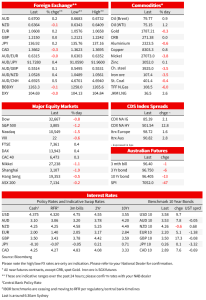

Against a backdrop of diminishing liquidity, all major US equity indices are trading in the red with S&P 500 set to extend its current route to a fourth day in a row. Rise in core global yields has not helped sentiment with UK Gilts leading the move. 10y UK Gilts closed 17bps higher while 10y UST yields are up by 10bps. Consolidation is the theme within FX with the USD a tad softer while the AUD tries to settle around 67c.

Equity sentiment has not been helped by a decent sell-off in core global bonds. The move up yield has been led by a bear flattening of the UK Gilts curve with the 2y tenor up 18bps to 3.59% while the 10y is up 17bps to 3.48%. The market is seemingly still digesting the BoE news that it will begin selling bonds from its QE portfolio on January 9th. The Bank expects to hold five auctions in each short, medium and long maturity buckets with a planned size of £650 million per sale (£9.75bn sales in total). The market has also increased BoE pricing expectations with a peak in the Bank rate now seen at 4.679% in September next year, 7.8bps higher relative to Friday’s levels.

ECB pricing expectations have also ticked higher with a peak in the Deposit rate now seen at 3.23% in July next year, 5bps higher relative to Friday’s pricing and 43bps higher relative to pre-ECB levels. In contrast to the bear steepening evident in the UK Gilts market, the Bunds market has endured a parallel upward move in yields with both the 2y and 10y rates up by 4bps (10y to 2.20%).

Playing to the move up in European yields, ECB Guindos said the ECB will raise interest rates until projections show that unprecedented euro-area price gains are headed back to the 2% target. Guindos suggested another 50bps should be in the offing at the next ECB meeting early in February. ECB (and Bundesbank President) Nagel was also speaking, stressing the need to increase rates given it will take some time until inflation slows to the central bank’s 2% target.

UST yields followed the move up seen in European yields with a steeping bias. As I type, the 2-year rate is up 7bps to 4.25% and the 10-year rate up 10bps to 3.58% – the latter has now fully unwound the chunky fall seen after last week’s softer than expected US CPI report. The subsequent hawkish Fed policy update remains fresh in the minds of investors. Playing into the hawkish vibes, overnight ex NY Fed Dudley said that optimistic markets could only make the central bank tighten even more.

Another factor souring the US equity mood has been an extension of the negative US economic surprises flow. Against expectation for a small improvement, the NAHB housing market index extended its decline to a twelfth consecutive month – the longest downward streak on record – to 31. The index is now close to the nadir at the height of COVID lockdowns in April 2020 and is the lowest in over ten years excluding that period. The US housing market recession reflects the combination of higher mortgage rates reducing demand and higher labour and material costs making it more expensive to build.

Meanwhile the mood music in Europe is almost the opposite with yet another positive economic surprise. Germany’s IFO business survey beat expectations with the business climate index increasing for a third consecutive month to 88.6 (both the current conditions and expectations components rose on the month). Of note all the improvement in the index through Q4 have come from less depressed expectations, a European recession still looks likely, but the data flow is increasing the prospect of a shallower than previously expected contraction.

As I type the S&P 500 is down 1.34% on the day and looks set to extend its decline to a fourth day in a row. The NASDAQ is 1.81%, feeling the weight from the rise in UST yields while the Dow is down 0.84%. Earlier in the session European equities closed mostly in the green with the Stoxx 600 index up 0.27%.

Somewhat surprisingly the USD has struggled notwithstanding the declines in US equities. Of note the decline in US equity markets has been rather orderly with the VIX index falling below 22, so the classic risk aversion with a rise in equity volatility has not been evident this time.

The Euro is up by 0.27% to 1.067 with the repricing of ECB rate hike expectations still providing a tailing for the union currency. From a technical perspective the euro also has room to extend its ascendency with the previous high of 1.0749 back in late May now coming into focus. GBP also made inroads against the USD, up 0.16% over the past 24 hours to 1.2145.

The AUD has been one of the top performers, up 0.4% to 0.67. Looking at the five-day chart the AUD looks to be consolidating just above the 0.67 mark after losing ground post the FOMC meeting last week. Meanwhile the NZD saw some selling pressure into the London close, falling to just above 0.6340 but has since recovered to trade at 0.6385. After trading sub 1.05 late last week, the AUD/NZD cross traded to an overnight high of 1.0561 and now start the new day at 1.0530. As my colleague Jason Wong notes, our outlook is for NZ-Australian rate compression, with too-much tightening priced into the NZ rates curve and too-little for the Australian rates curve. The market has yet to embrace this view but ultimately a change in sentiment on the rates outlook is expected to trigger a reversal in the AUD/NZD cross, our 2023 forecast sees the cross heading back above 1.10 next year.

JPY has underperformed against the backdrop of higher Treasury yields, with USD/JPY up to 136.75, 100 pips above the low yesterday. The yen opened the week strong, before unwinding the move, following the weekend article in the Japan Times that the government was set to revise the accord with the BoJ to make its price target more flexible. That may well be the case, but not for a while, and certainly after current Governor Kuroda leaves next April. The BoJ meets today and no change to its ultraeasy policy is expected (see more below)

Coming Up

This morning New Zealand releases the ANZ business survey for December and the RBA publishes Minutes of the December policy meeting. Our economists note that the Minutes may reveal whether the RBA discussed the merits of a 25 vs. 50bp hike, or whether there was also any discussion of a pause. The post-meeting Statement only included the barest of nods towards the prospect of a pause despite recent rhetoric. With November labour market data still showing a tight labour market, we think it would be too early for pause, and we continue to see the RBA hiking rates by 25bps in February and March.

China’s Loan Prime Rate (LPR) decision is announced just after midday (Sydney time). After no change to the medium-term lending facility (MLF) rate last week, the consensus view is for the LPR (3.65%) to also remain unchanged today.

After a two-day policy meeting, later today the BoJ is expected to leave its ultra-easy policy setting (negative interest rate and Yield Curve Control) unchanged. Governor Kuroda’s press conference is likely to attract a lot of media attention not only in terms of what he may say on the inflation outlook but also on the possibility of a policy review as well as a likely revision the Government and the Central Bank accord.

Later tonight the US gets Housing Start figures (Nov) and Canada prints retail sales stats for October.

Creating cost-effective choices for consumers while forging business success is nothing new for Chemist Warehouse co-founder Jack Gance. As special guest at a recent NAB Transaction Banking event series, he looks at a new way to pay for businesses and customers.