Total spending grew 0.9% in June.

The impact of the latest lockdown and Biden’s stimulus backflip. NAB’s Ray Attrill on two bits of news for markets to respond to this morning.

https://soundcloud.com/user-291029717/lock-down-means-no-rba-lowdown?in=user-291029717/sets/the-morning-call

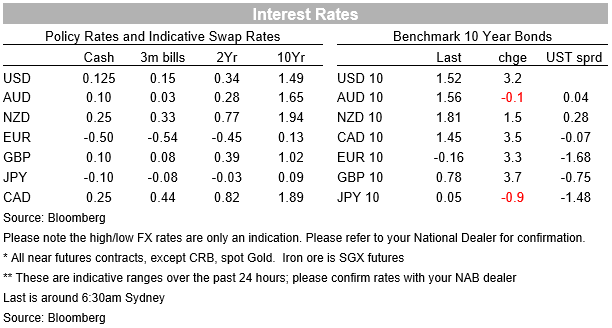

It wasn’t a big night for markets on Friday, lacking major data surprises or other market moving events, though over the week it has been a good one for stocks globally; the US Treasury curve has re-steepened somewhat after the dramatic post-FOMC flattening the week before with 10s now back above 1.50%, while in the context of a US dollar that lost 0.8% in BBDXY index terms, AUD/USD finished the week up some 1.5%. It failed though to gain a foothold back above 0.76 as we head into month, quarter, half and financial year-end on Wednesday.

Of note since Friday’s New York close, US President Biden on Saturday walked back his threat to refuse to sign a $1tn bipartisan infrastructure deal unless it is accompanied by a larger and more comprehensive spending package, in what the FT for one described as a ‘sharp U-turn by the White House just two days after reaching the landmark cross party deal’. The abrupt shift from Biden came after Republicans reported balked at the US president’s insistence on Thursday that the fate of the two pieces of legislation be tied together.

“At a press conference after announcing the bipartisan agreement, I indicated that I would refuse to sign the infrastructure bill if it was sent to me without my Families Plan and other priorities, including clean energy,” Biden said in a statement on Saturday. “That statement understandably upset some Republicans, who do not see the two plans as linked,” he added. “My comments also created the impression that I was issuing a veto threat on the very plan I had just agreed to, which was certainly not my intent.”

In so far as one of the catalysts for US equities achieving new record highs last week was the news of a the handshake deal between the president and a bipartisan group of Senators, but some Republican Senators now ‘smell a rat’ in so far as voting for the infrastructure bill could be akin to also voting for the American Families Plan then developments here promise to be one source of market volatility in the week ahead.

Fed speakers on Friday night included Boston Fed President Eric Rosengren (2021 non-voter) who while aligning himself with the view that current high inflation is likely to prove transitory in so far a large outliers (used car prices especially) accounted for most of the recent movement, he did say that the conditions could be met for a first rate rise by the end of 2022. Minneapolis Fed President Kashkari professed not to be surprised by some of the current inflation readings and is still of the view they will normalise to bring inflation back down (he cited the recent sharp fall back in lumber prices as one example). Former US Treasury Secretary Larry Summers meanwhile is still having none of it, saying he sees inflation at 5% at the end of this year and that he “doesn’t see the basis for policy makers’ serenity”.

On the data front, US Personal Incomes fell 2.0% in May, reflecting the fading impact of the stimulus payments made under the March covid relief bill, better than the -2.5% consensus. Real personal spending fell 0.4%, weaker than the -0.1% consensus, though April was revised up to 0.3% from -0.1%. The core PCE deflator rose 0.5%, below the 0.6% expected but the yr/yr rate lifted to 3.4% from 3.1% as expected, a smaller jump that in the already-released may CPI data, due to rents having lower weight in the PCE data and differences in the way airlines fares are calculated, which our friends at Pantheon Economics note throw up month-to-month anomalies even though they trend together over time.

The final University of Michigan June Consumer Sentiment Index came in at 85.5, below the 86.4 preliminary and 86.5 expected. 5-10 year inflation expectations were unchanged on the preliminary at 2.8% while 1-year expectations were 4.2%, above the 4.0% preliminary and 4.1% expected. China industrial profits data released on Sunday showed profits up 36.4% in May on a year ago, down from 57.0% in April, reflecting some fading of year-ago base effects that were at their peak in March when profits were up 92.3% yr/yr.

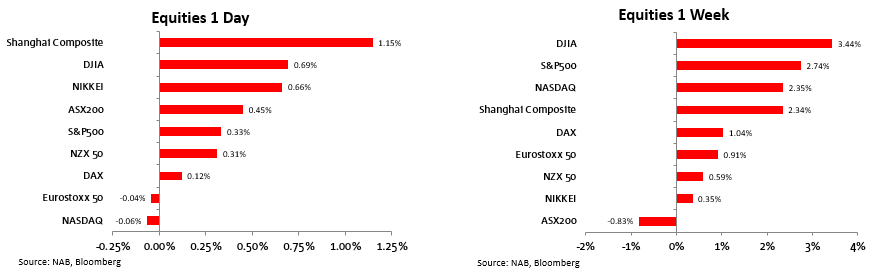

It was a good night – and week – for US equities on Friday with the S&P500 closing at a new record high for the second successive day and the VIX at a new post-pandemic low of 15.6 (not quite back to pre-pandemic levels, but pretty close). Financials led Friday’s moves (+1.25%) benefiting both from the announcement after last Thursday’s close that all 28 large US banks had comfortably passed the latest Fed stress tests (so heralding potential fresh share buy-back and/or dividend increases) and the further re-steepening in the US yield curve following the prior week’s dramatic flattening.

The Dow, (+3.44%) S&P (+2.74%) and NASDAQ (+2.35%) were the best three performing major global equity indices last week. The ASX 200 was down on the week due to the impact of some stocks going ex-dividend on Tuesday, but did okay on Friday (+0.5%) despite the latest covid infection news and anticipation of more widespread lockdowns being announced at the weekend, which duly arrived on Saturday with all of Greater Sydney put into lock-down, initially for two weeks.

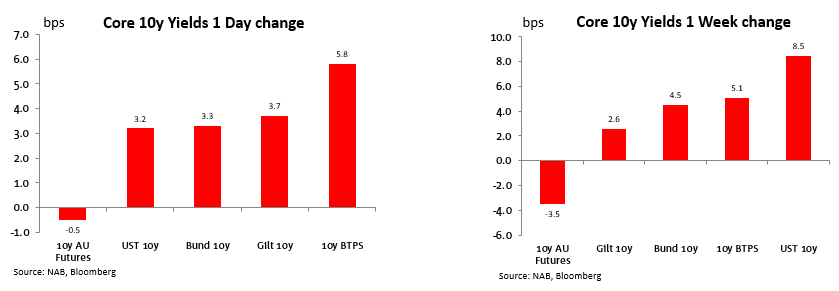

In bond markets, longer dated yields continues to recover from their prior week’s post-FOMC bashing, with 10-year Treasuries and Bunds both up 3bps, UK gilts +4bps and Italian BTPs +6bps. On the week, US 10s are up 8.5bps, 2s up 1bps and the 30-year +13.5bps. In contrast, Australian 10-year cash bonds lost 3.5bps to 1.56%, narrowing the spread over US10s to some 4bps from 16bps a week before.

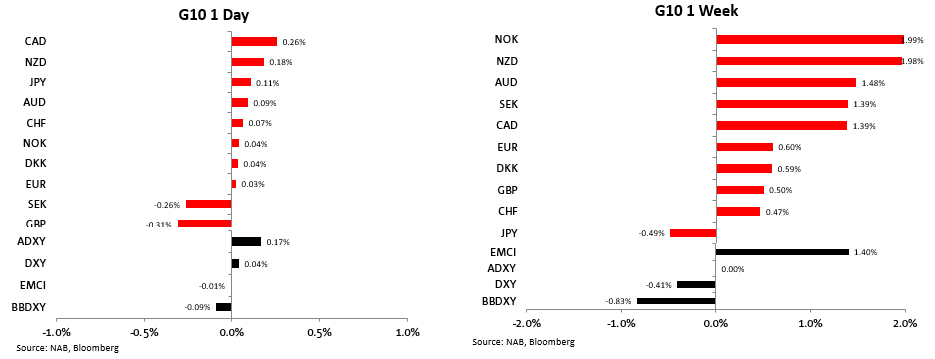

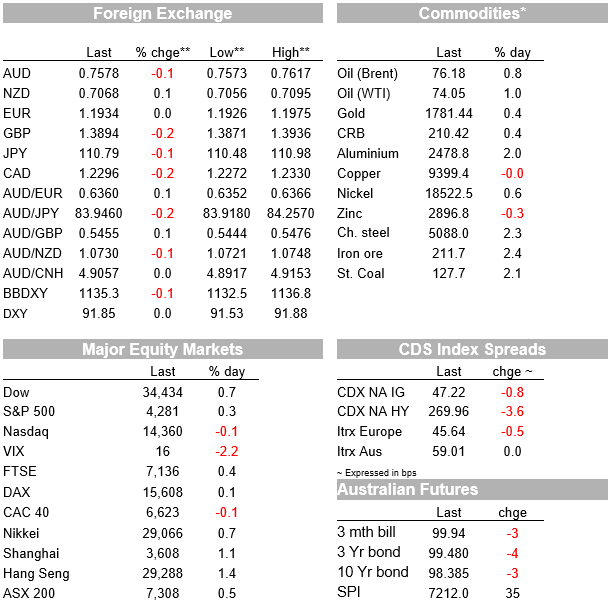

It turned out to be a quiet Friday in currencies with the USD losing a touch (-0.09%) and only the CAD (+0.26%) and NZD (+0.18%) showing much movement. AUD was up just shy of 0.1% and did manage to spend some time above 0.7600 (high of 0.7617) but ended the week at 0.7590, up 1.5% on the prior week’s lows. It has opened s little softer this morning (0.7580) doubtless as market’s asses the economic fall-out from the covid related restrictions announced over the weekend.

Finally commodities generally did well on Friday, e.g. aluminium up 2%, iron ore futures +2.4% and a 0.8% rise in Brent crude lifting it to $76.18 ahead of this week’ OPEC+ meetings. The LMEX index of base metals closed Friday at its best level in 8 days to be up 3.6% on the week.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.