Total spending grew 0.9% in June.

“long ways to go” is the Fed’s Jerome Powell’s take on the path to recovery for the American economy and the reason that rates won’t be lifting anytime soon.

https://soundcloud.com/user-291029717/long-ways-to-go-says-powell?in=user-291029717/sets/the-morning-call

It was just a matter, It was a matter of time – The Killers

The latest FOMC meeting and press conference from chair Powell has come and gone with no big fireworks, though Treasury yields are lower, as is the USD, after Powell made clear that it was ‘not time yet’ to have a conversation about tapering its $120bn monthly QE bond buying programme and that we ‘are not close to’ the substantial progress toward its employment and price stability goals, that has been set as a conditions for contemplating doing so. This is despite the FOMC upgrading its economic assessment in the formal post-meeting Statement. This says that ‘indicators of economic activity and employment have strengthened (an upgrade from ‘ have turned up’ in March) and that ‘sectors most adversely impacted by the pandemic have improved’ (versus ‘remained weak’ in March). The Statement also removed the adjective ‘considerable’ previously placed in front of the comment, repeated, that ‘risks to the outlook remain’. The Fed chair also continued to stress the expected transitory nature of the pick-up in inflation that currently looks to be underway (and which will be further evidenced in the PCE deflator numbers in tonight’s Q1 GDP release – see Coming Up below).

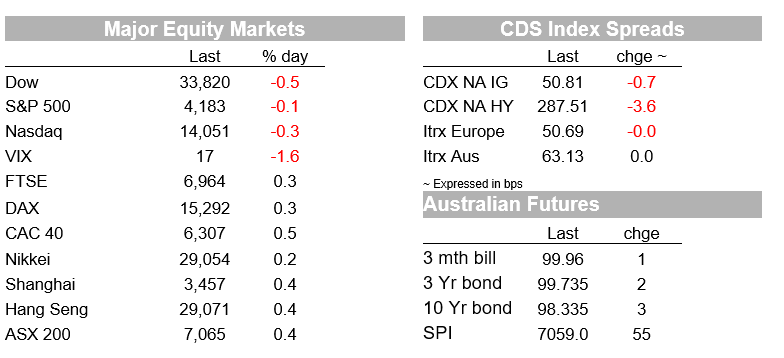

US equities initially responded positively to the messaging from the Powell press conference, the S&P 500 gaining about 0.3%, but gave back all of the gains and then some in the last ‘hour of power’ to finish 0.1% lower on the day (NASDAQ -0.3%). Post NYSE close however, Apple has jumped 3% after crushing its Q2 revenue estimate, reporting $89.58bn against the $77.30bn street consensus (it has also authorised $90bn worth of share buy-backs). Facebook reported Q1 revenue of $26.17bn, up on the $23.72bn consensus. Its stock is up over 5%. These presumably will shortly be showing up in stronger NASDAQ futures in the APAC session.

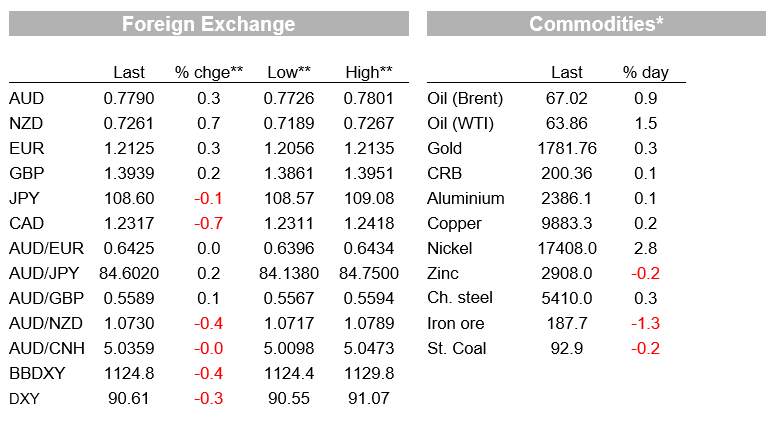

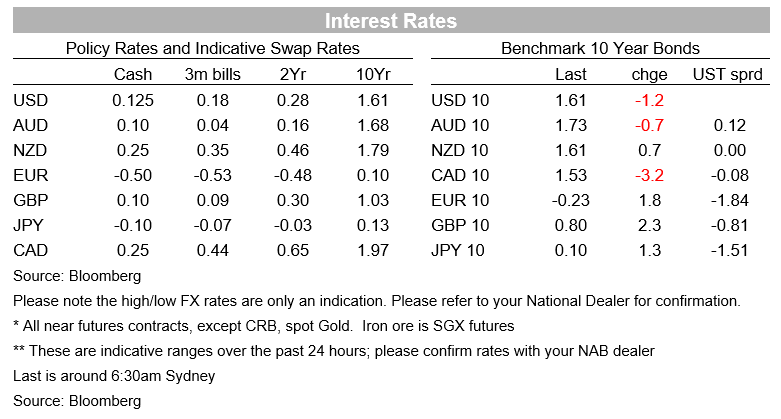

From a pre-FOMC statement level of 1.645%, 10-year US Treasury yields rose by 1bp on the upgraded economic assessment evident in the Statement, before dropping back to below 1.62% as the Powell press conference unfolded (currently 1.61%). In FX, in index terms the USD lost about 0.25% soon after Powell’s ‘not yet time’ remarks, and is now some 0.5% lower versus pre-FOMC Statement levels. The biggest gainers in the last 24 hours have now been NOK (+1%, albeit helped by an oil price rebound), NZD (+0.8%, but which was already doing well pre-Fed) and CAD (+0.7%, with assistance from both oil and very strong February retail sales data – see below).

AUD brief traded back onto an 0.78 handle during the Powell presser but is finishing in New York just below (0.7787now). Holding 0.78 really is proving challenging just at the moment, though post-Fed gains still mark a full recovery from the dip down to a low of 0.7725 in the immediate wake of yesterday’s softer than expected Q1 CPI figures. These saw headline CPI print at 0.6% against 0.9% expected and the core Trimmed Mean measure come in at 0.3% against the 0.5% consensus.

The downside miss was mostly due to housing costs, and where the large volume take up of the Homebuilder scheme in Q1 (albeit tapered from Dec 31 2020) depressed new housing costs by some 2% (these were down 0.1% on the quarter, but would have been +1.9% without the Homebuilder subsidy). Rents also surprised to the downside (led by a 0.5% fall in Sydney). So, despite reports of rising rents in Melbourne and Sydney especially, this has evidently not flowed through to positively the impact the stock of existing rental properties, while in many case higher rents currently being commanded are still not putting them back above the level to which they fell in 2020 during the pandemic. The data vindicates the RBA’s last published view (from February) that core inflation remains very subdued and that CPI inflation is likely to remain below the (sustainable) 2-3% target for several years to come. Local government bond yields fell by around 3bps from 3 years out following the release.

In economic data elsewhere published overnight, the US goods trade deficit blasted up to a fresh record high at $90.6b for March (a reminder that the burgeoning ‘twin deficits’ are coming from the external trade side not just the blow-out in budget deficits). Canadian economic data continues to positively surprise, with a strong 4.8% rebound in core retail sales in February, helped by reduced lockdown restrictions.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Read our NAB Markets Research disclaimer

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.