Online retail sales growth slowed in May following a fairly strong April

Insight

Equities are back on the rise and bond yields are falling, slightly, as investors seem to have accepted the line of most central banks that inflation is only transitory.

https://soundcloud.com/user-291029717/low-volumes-more-risk-less-inflation-concerns?in=user-291029717/sets/the-morning-call

Destiny is calling me, Open up my eager eyes

‘Cause I’m Mr. Brightside – The Killers

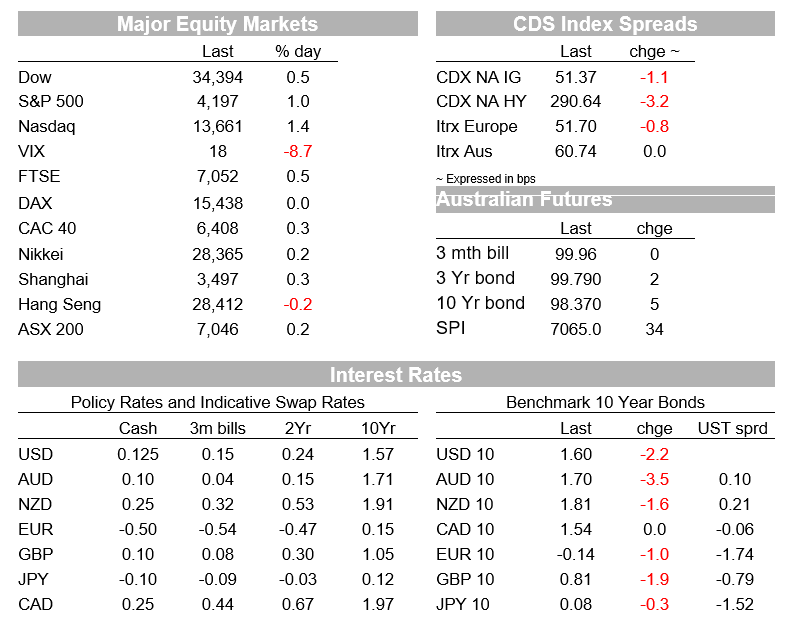

US and European equity markets have begun the new week looking at the bright side of life, longer dated UST yields have continued to drift lower and the USD is broadly weaker. Oil and copper are up while bulk commodities stabilise after yesterday’s China led decline.

Tech stocks have the led the gains in US equities with the NASDAQ up 1.41% while the S&P 500 has ended the day +0.99%. Looking at the 11 sectors in the S&P 500, utilities is the only sector in the red, down 0.2% with the remaining 10 sectors showing gains for the day. Communications and IT closed up around 1.8%. The Stoxx 600 Index added 0.14% with German, Danish, Norwegian and Swiss stock markets closed for holidays.

There were no major news flows or data releases affecting markets overnight with the pickup in risk sentiment attributed to an ease over inflation concerns . Markets appear to be coming around to the Fed narrative that a burst in inflation is only likely to be temporary and therefore should not be a concern. A temporary spike in prices should not instigate a removal of stimulatory policies from Central Banks.

Supporting this view, Fed speakers overnight reiterated the message that they expect a rise in prices due to bottlenecks and supply constraints as the pandemic retreats and pent-up consumer demand is unleashed, however at this stage there is no evidence to suggest this push in price anything but temporary in nature. Fed Governor Brainard ran the party line in calling the lift in inflation as likely temporary, noting “well anchored” longer-term inflation expectations. Atlanta Fed President Bostic ran the same line, calling the lift in inflation as temporary while St Louis Fed President Bullard said that it wasn’t the time to talk about changing the parameters of monetary policy, saying “when you’re in the crisis I think you should make sure you’ve exited the crisis aspect before you think about changing policy. We’re not quite there yet”. He added that he expected to see more inflation but “it’s mostly temporary”.

Moving onto the rates markets, longer dated nominal UST yields have drifted a little bit lower again, favouring the risk positive backdrop in equities, the 10y Note is down 1.7bps to 1.6029% while the 30y Bond is down by a similar amount to 2.3020%. The move down has been led by the real component with 10y real rate down 3bps to -0.86%. Meanwhile after a 10bps decline last week, 10y UST breakevens have edged a little bit higher overnight, up 2bps to 2.46% with the move up in oil prices the likely culprit.

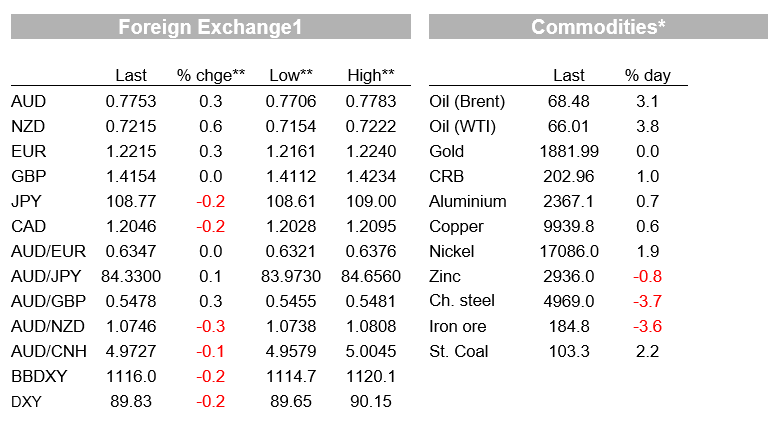

Oil prices are up 3-4%, with less concern about the possibility of a short-term ramp-up in supply from Iran after the country said that there are still differences on sequencing and verification relating to talks with world powers on the 2015 nuclear agreement. Furthermore, a Goldman Sachs report said that demand would be strong enough to absorb extra supply and Brent crude would hit USD80bn the next few months.

Looking at other commodities, copper rebounded (+0.66%), shrugging off China’s renewed angst against soaring commodities prices . Yesterday China’s National Development and Reform Commission (NDRC) said the government will show “zero tolerance” for monopoly behaviour and hoarding after leaders of top metals producers were called to a meeting in Beijing with multiple government departments on Sunday. Key enterprises should “actively fulfill their social responsibilities” and take the lead in maintaining market order, the NDRC said in a statement.

The warning from Chinese officials triggered a sell-off in metals and bulk commodities with steel and iron ore prices falling during our session yesterday, but prices stabilised overnight edging a little bit higher before the close. Although some of the rise in commodity prices has been driven by speculators, there is also a genuine increase in demand as the global economy reopens while China’s own policies to reduce greenhouse gas emissions along steel output restrictions have also contributed to the rise in commodity prices. So many think NDRC measures to clamp down on speculators may not be enough to ease the price pressure.

In currency markets, higher risk appetite has driven broadly based weakness in the USD with BBDXY and DXY indices down around 0.20% over the past 24 hours. NOK heads the leader board boosted by the decent rise in oil prices (+0.68%) with the NZD not far behind, up 0.61% to 0.7210. The RBNZ MPS is the focus this week, the NZD has been locked in a 0.71-0.73 range and a less dovish RBNZ, as our BNZ colleagues expect, could be the catalyst for a topside break .

The move lower in metals and bulk commodity prices weighed on the AUD yesterday, although in the end it wasn’t a longer lasting headwind. After trading to a low of 0.7706, the AUD now trades at 0.7756, comfortably within its 0.77 to 0.78 range that has mostly contained the pair since March this year.

Other major pairs show modest gains against the USD with USD/JPY in particular little changed and showing no major reaction to news the US CDC issued a “do not travel” advisory for Japan due to “very high levels of covid-19”. Raises the obvious question of US participation in the July Olympics (and with that the fate of the Olympics itself). Current state of emergency restrictions in Tokyo and elsewhere currently expire on May 31, with a decision on whether to extend them therefore needed this weekend at latest.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.