Confidence and Conditions Lift

Insight

Last night’s first Federal Budget under Labor Treasurer Jim Chalmers contained no fireworks, falling fully in line with pre-Budget media briefings.

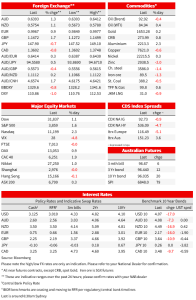

Continuing the theme of bad (economic) news is good news (for risk markets) US equities are continuing to bask in the afterglow of last Friday’s hints of a step-down in the pace of Fed tightening come the December FOMC, further supported overnight by a string of softer than consensus, albeit very much second tier, US economic news (covering house prices consumer confidence and another regional Fed survey). A Positive market take on the confirmation of Richi Sunak as Britain’s’ third prime minister of 2022 and a presumed safe pair of hands has also made a positive contribution to overnight price action, albeit our UK colleagues note there is no sign of a ‘unity Cabinet’ being assembled under new PM, appointments so far being heavily skewed toward the right/Brexiteer wing of the Tory party. Australia’s Q3 CPI is this morning, Bank of Canada tonight where there is considerable uncertainty over the size of the prospective rate hike.

US economic data overnight, second tier as it is, included a bigger than expected drop in the Conference Board’s measure of Consumer Confidence, down to 102.5 from 107.8 and 105.9 consensus. Ditto US house prices, the FHFA measure for August down 0.7% on the month (-0.6% expected), S&P Case Schiller 200-City average -1.32% on the month vs -0.8% expected and the largest monthly fall since 2009). The Richmond Fed manufacturing Index fell to -10 from zero against a consensus for -5.

Earlier Tuesday, the German IFO survey showed little overall change against expectations for a deterioration, the Business Climate reading 84.3 from 84.4 (revised from 84.3) and versus 83.5 expected, with the Current Assessment at 94.1 from 94.5 against the 92.5 consensus and Expectations up a touch, 75.6 from 75.3.(75.0 expected). All minor differences, but of some relief after weaker than expected German PMI data on Monday.

Locally, last night’s first Federal Budget under Labor Treasurer Jim Chalmers contained no fireworks, falling fully in line with pre-Budget media briefings. The near-term budget deficit position dramatically improved due to revenue upgrades from higher commodity prices, a strong economy and lower unemployment. The Budget delivers fully on Labor’s election commitments, but major reform/action to resolve medium-term pressures on the Budget are postponed to at least the next May Budget (and therefore including any decision to rescind the legislated tax cuts for higher income workers).

In NAB’s view the Budget doesn’t add extra inflationary pressure, but deficits across the horizon don’t alleviate pressure on the RBA either. Upward revision to the estimated structural deficit highlights the scale of the fiscal repair task and risk should the economy slip into recession. Growth is forecast to slow sharply next financial year (1.5% in 2023-24 versus 3.25% this year); unemployment expected to increase to 4.5% from 3.5% currently; and inflation falls relatively slowly, remaining above the RBA’s 2-3% target range in 2023-24.

In markets, there was some excitement (or consternation) following the daily PBoC fixing of the USD/CNY rate, that came in much higher than the consensus estimate complied by Reuters (7.1668 against Reuters survey estimate of 7.1348). A strong indication that the Chinese authorities, in the immediate wake of the NPC that concluded last Sunday, was not going to oppose fresh CNY depreciation (i.e., USD/CNY up though the pre-NPC high of around 7.25%). The offshore USD/CNH rose to as high of 7.3750 overnight and while the onshore USD/CNY pretty much traded up to the 7.31 +/-2% allowable limit relative to the fix before PBoC intervention is mandated (high of 7.3093).

There was some immediate read-through from the weaker Yuan to AUD and NZD, both dropping 20-30 pips in short order in early-day China trading, but overnight the impact of a broadly weaker USD alongside further improvement in risk sentiment has overwhelmed the CNY-effect, AUD/USD up to a high of 0.6412 and NZD/USD to a high of 0.5780. the USD is currently off 1% on Monday’ NY close in DXY terms, now about 3.5% off its 28 September highs.

GBP currently tops the G10 leader board with a daily fain of more than 1.5% as the new stability-oriented Sunak govt starts to be assembled and after the complete U-turn of prior Truss policies. Hard yards ahead for the UK on growth and even more division possible on things like spending cuts, tax hikes, immigration, Northern Ireland, etc. but UK market currently trade on the view that pragmatism rather than ideology will rule the day. The point here is the mini era of chaos is over for now. 10-year gilt yields are off another 10bps overnight, though this is less than the 16bps falls we have seen in the US, France, and Germany. Details of the (latest) UK fiscal plan next Monday (Chancellor Hunt has retained his post) and then the Bank of England decision on 3 November now keenly awaited. Overnight, BoE chief economist Huw Pill stanchly defended the current (2%) inflation target.

The rally in US Treasury markets begin my last Friday’s commentaries from the WSJ’s Timiraos and San Francisco Fed’s Mary Daly has extended Tuesday, with 10-year Treasuries down 16bps to 4.085% and from a high of 4.33% just in front of their remarks. Similar sized falls in Eurozone yields, both German Bunds and French OAT10s also own 16bps and Italy an even bigger -20bps. No sign of ‘fragmentation’ here and a positive for the single currency.

Equity markets are liking the lower yield backdrop (except the UK FTSE which apparently don’t like the stronger GBP!) with the Eurostoxx 50 finishing +1.6%. US stocks finished higher for a third successive day, the S&P500 up 1.7% and the more interest rate sensitive NASDAQ by 2.1%, positive earnings results from the likes of Coca Cola and General Motors helping the former. Post NYSE close, Alphabet’s shares have dropped 5% after reporting lower than expected Q3 revenue of $57.27bn (Street consensus was $58.218B) while Microsoft just beat its revenue estimate, coming in at $50.12bn against a $49.56bn consensus.

Confidence and Conditions Lift

Insight

Online retail sales growth slowed in May following a fairly strong April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.