We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

US CPI was a higher than expected but the Market seems to have taken it largely in its stride.

https://soundcloud.com/user-291029717/market-unphased-by-us-cpi-ecb-stays-dovish-despite-upping-forecasts?in=user-291029717/sets/the-morning-call

Ooh, baby

Ain’t nothing like the real thing, baby – Marvin Gaye & Tammi Terrell

US inflation printed stronger than expected with most, but not all of its underlying drivers pointing to transitory factors. Still, markets bought the transitory narrative implying the Fed won’t be taking its foot from the easing pedal anytime soon. After some intraday volatility, US equity markets ended the day higher, but the real story was in the US Treasury market. The 10y Note led the decline in nominal yields with a sharp fall in the real yield, only partly offset by an uptick in breakevens. The USD closed the session a tad softer, AUD up smalls and NZD unchanged. ECB doesn’t surprise the market and kicks tapering discussion down the road.

US inflation continued its sharp rise in May with the headline reading up 0.6%mom taking the yoy reading to 5%. The core reading jumped 0.7%mom, above the consensus, 0.5%, lifting the yoy reading to 3.8%. The past 3 month rise in core US inflation was the highest recorded since August 1982, but just like in April, the main drivers for the lift in prices in May can be linked to post covid re-opening dynamics. The May uptick in core inflation was largely driven by an increase in used car prices (+7.3%, adding 0.3% to the core CPI, after a 10.0% surge in April), airline fares (7.0% after 10.2% in April) and auto rental (12.1% after 16.2% in April).

That said, the data also revealed a pick-up in housing costs and with rents accounting for 40% of core CPI, a louder voice of economists is pointing to the risk of a more permanent lift in inflation once the reopening spike in prices is over. Housing demand is on the rise against tight supply and an improving labour market, supporting the notion that a higher trend in housing cost could be in the offing.

That is a story for another day, for now the market has seemingly embraced the transitory inflation narrative implying the Fed won’t be taking its foot from the easing pedal anytime soon. Supporting the Fed’s view, another measure of core inflation – the Cleveland Fed’s trimmed mean measure – saw another small increase in underlying inflationary pressure, but at a more moderate pace than the official measures, with a monthly gain of 0.39% (previously 0.37%) and annual inflation rising to 2.6%.

US jobless claims fell for a sixth consecutive week to 376k, consistent with the range of other labour market indicators showing an improvement as the economic recovery takes holds.

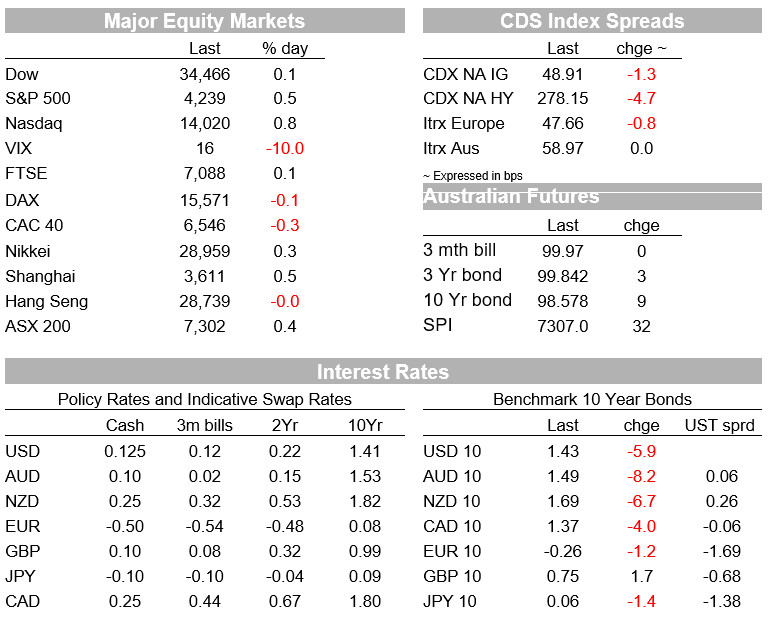

After some intraday volatility, US equities have ended the day higher. The CPI release triggered an intraday fall of 0.65% in the S&P 500, but once details of the report were assessed, the index recovered closing the day +0.47% and at a new record high of 4239.18. The NASDAQ was the outperformer, up 0.78% aided by the post CPI rally in the US Treasury market.

The 10y note led the move lower in nominal UST yields, down 6bps on the day to 1.43%. But the real story was the sharp decline in the real yield component. Ahead of the data release, the 10y real rate traded to a high of -0.83%, but reaction to the data triggered a big fall and now the real 10y rate trades at -0.9378%. The move lower in real yields was only partly offset by an uptick in the breakevens (inflation expectations component) from 2.32% to 2.35%.

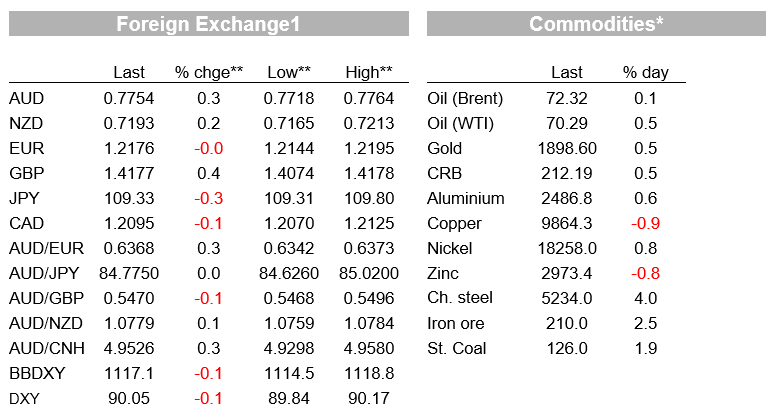

The FX reaction to the US CPI and ECB for that matter (more below) was rather muted. The USD is only a tad weaker (both BBDXY and DXY ~-0.10%) with the post CPI improvement in risk appetite and move lower in UST yields, led by real yields only proving to be a small headwind for the greenback. That said, the narrative of Fed tolerance for higher inflation is not a good a USD story and we see the move lower in real yields as a supporting factor for a lower USD.

The dovish ECB has held back EUR performance, seeing it flat at 1.2175 , GBP and NZD are also little changed at 1.4177 and 0.72 respectively while the AUD is a tad stronger (+0.13%) at 0.7754.

In its policy update, the ECB raised GDP growth and inflation forecasts and, for the first time since 2018, noted that the risks to economic growth are now balanced (previously saw downside risk). However, the Bank saw higher inflation as temporary (CPI inflation of 1.9% in 2021 but falling to 1.5% next year) and underlying price pressures remaining subdued.

On its QE programme the ECB still decided that emergency bond buying would continue at a significantly higher pace than seen at the start of the year . President Lagarde noted some diverging views on the Governing Council on the pace of bond purchases and some in the market had expected some moderation. So this was a small dovish surprise but overall market reaction to the ECB’s messaging was minimal.

Looking at other economic news, China released its aggregate financing data for May yesterday evening. Credit growth was steady in May, but shadow bank lending contracted again . Aggregate financing was ¥1.9trn ($297 billion), unchanged from April and in line with expectations. Shadow bank lending, such as trust loans, outstanding bank acceptance bills and corporate bonds contracted again (~¥400bn), consistent with authorities’ emphasis on guarding against financial and default risks.

After the sharp credit tightening in April, the stabilisation in China’s credit growth in May is a welcome outcome, easing concerns over the negative impact in activity from a slowdown in the credit impulse. That said, we still think the PBoC will aim to restrain the pace of credit growth as China’s economy continues its post pandemic recovery.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.