The NAB Commercial Property Index lifted to an 8-year high in the March quarter, continuing the run of improvements seen in recent quarters.

Insight

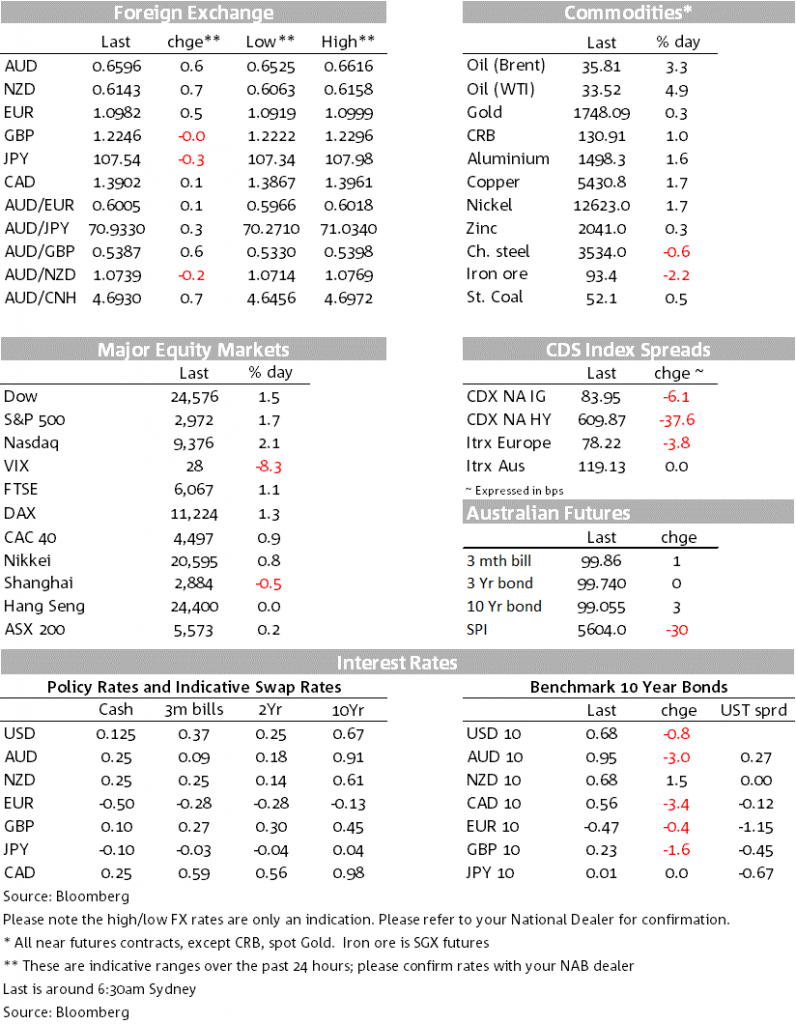

It’s been another positive session, driving equities higher and giving another boost to the Australian dollar.

https://soundcloud.com/user-291029717/markets-accentuate-the-positive-but-boe-now-contemplating-the-negative?in=user-291029717/sets/the-morning-call

“I feel like a zombie comin’ back to life (back to life); Hands up, and suddenly we all got our hands up; No control of my body; Ain’t I seen you before?”, Usher 2010

Rollback continues to support risk sentiment with markets optimistic that economic activity will rebound sharply (in a cursive V shaped recovery perhaps?). Vaccine hopes also continue despite Tuesday’s mild doubts with Moderna pushing back on detractors. Another company (Inovio Pharmaceuticals, stock +8.8%%) also reported encouraging findings for its own vaccine in animal tests (see Nature Communications). Separate studies in rhesus macaques also suggests vaccines can lead to immunity from COVID-19 (see Science for details), and that being infected by the coronavirus leads to protective immunity against re-infection – again at least in primates (see Science for details). The developments again reinforce for markets it’s a matter of when, rather than if for a vaccine.

Equities rose (S&P500 +1.7%) with the rally now broadening to smaller caps (Russel 2000 +2.7%) and suggestive that broader activity is picking up as rollback restrictions are eased (note all 50 US states have now eased containment measures in some way). The USD remains on the backfoot with the DXY -0.5% and back to where it was in late April.

Global growth proxies and commodity-linked currencies continue to outperform with the AUD +0.6% to 0.6599 (session high 0.6616 with 0.6675 being a key resistance level). Those gains come despite elevated rhetoric around Australia-China trade and US-China trade. And the US Senate passing a bill that could bar some Chinese companies from listing on US exchanges. The AUD has been trading with little day light to the S&P500 rally since late March, highlighting its global growth proxy role. Also likely adding to sentiment was more speculation around Chinese stimulus and a possible GDP target to be unveiled on Friday at the National People’s Congress. MNI yesterday ran a piece a 3% target could be possible, while Finance Minister Kun has called for “more proactive fiscal policies”.

The broad-based weakness in the USD was reflected in most pairs apart from GBP, where talk of negative rates helped to drag it lower (GBP -0.1%; EUR +0.4%; USD/Yen -0.3%). BoE Governor Baily said he isn’t excluding the idea of taking borrowing costs below zero (“of course, we’re keeping the tools under active review in the current situation” …“we do not rule things out as a matter of principle”). The BoE’s stance is in contrast to the BoC, RBA and Fed who have all ruled out negative rates. Meanwhile a £3.8bn 3yr Gilt auction settled at a yield of -0.003% and was oversubscribed (the first for the UK after a negative yielding bill auction in 2016). Brexit negotiations remain ongoing with little new development.

The NZD outperformed, up 0.7% as the RBNZ continues to push back on any near term change to the OCR. RBNZ Governor Orr said in a Bloomberg interview yesterday that “We don’t want to go negative at this point; we’re prepared to if we have to but not until a lot later. It’s got to jump the hurdles. It’s got to be seen to be necessary. It’s got to be seen to be effective, efficient and operationally capable”. Bank officials have made it crystal clear that they want the option of a negative policy rate in the toolkit, but that doesn’t necessarily mean it would be used. Our BNZ colleagues continue to see the RBNZ not taking the OCR into negative territory and keeping to its word of having the OCR unchanged this year. Consequently the OIS market is nudging rates higher, with the November meeting up 2bps to 0.16%. The market continues to see a negative OCR priced from May next year, although over recent days reduced conviction in that call is evident as it digests recent RBNZ comments.

The FOMC Minutes came and went without two much fanfare given we already had Powell at the Senate Banking Committee. The key takeaways were: (1) “some” participants suggest forward guidance could be made more explicit by utilising “outcome-based forward guidance” linked to a certain level of the unemployment rate or inflation; and (2) a “few” participants noted forward guidance could be enhanced via yield curve control – “purchases of Treasury securities on a scale necessary to keep Treasury yields at short-to-medium term maturities capped at specified levels for a period of time (see FOMC Minutes for details). Yields were little moved on the FOMC Minutes and generally traded in tight ranges. The US 10yr yield fell marginally by -0.8bps to 0.68%.

It continues to take a back seat as markets look to higher frequency data to gauge how quickly activity is returning. Reflecting that, Australian markets were little moved by yesterday’s flash retail sales print for April where sales fell by a record -18% m/m as panic buying faded (food sales fell 17% m/m in April, following a 24% rise in March).

Another hint of activity returning in higher frequency data is Job Ads with SEEK reporting today new job ads posted in the fortnight ended 17 May are up 26.8% compared to the April 2020 average with sizeable increases seen across all states, “suggesting we have turned a corner as long as we do not see a return of restrictions or a further outbreak”.

Economic news overnight was on the light side with UK Core CPI in line at 1.4% y/y, while Eurozone Consumer Confidence was a little better than expected at -18.8 against a consensus of -23.8.

WTI up +4.9% to $33.52 despite mixed EIA inventory data (oil inventories fell, but gasoline stocks rose). CAD underperformed despite the rise in oil prices with Canada’s Headline CPI fell by 0.2% y/y in April, the lowest since the GFC, driven by lower petrol prices, while core inflation was steady at 1.8% y/y.

All eyes on the global PMIs to see whether economic activity troughed in April and if the easing of lockdown restrictions is seeing a bounce back in activity as indicated by the high frequency data such as Apple/Google mobility indicators. Australia kicks off the flash-PMIs, followed by Japan, Germany/Eurozone and the US. Focus domestically will also be on RBA Governor Lowe’s appearance at a financial regulators forum. Attention then turns to the US with Weekly Jobless Claims watched closely to see whether increasing activity is translating to a troughing in the labour market and to the Fed where the big three of the FOMC (Powell, Clarida and Williams) are speaking. Key releases in detail:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

The NAB Commercial Property Index lifted to an 8-year high in the March quarter, continuing the run of improvements seen in recent quarters.

Insight

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.