NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

A surprise U-turn by the UK government on the fiscal package and a weaker than expected US ISM Manufacturing (50.9 vs. 52.0 expected) have driven a large fall in global yields.

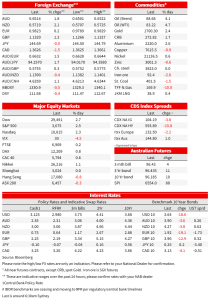

A surprise U-turn by the UK government on the fiscal package and a weaker than expected US ISM Manufacturing (50.9 vs. 52.0 expected) have driven a large fall in global yields. The US 10yr is down -18.6bps to 3.64%, and at one point hit a low of 3.57%. The US 2yr yield also fell around 16bps to 4.12% meaning the 2/10s curve flattened to -47.9bps. The moves have been reflected in real yields with the 10yr TIP yield falling -24.4bps to 1.43%, while the implied breakeven rose 5bps 2.20%. The lift in break-evens comes alongside a surge in oil prices with Brent oil up 4.7% ahead of OPEC+ tonight. Even though yields have moved sharply, Fed Funds pricing still implies a 72% chance of a 75bp hike in November and a peak of 4.45% by March 2023. For equities, the weaker than expected ISM was ‘bad news is good news’ with the S&P500 surging 2.6% after having fallen on Friday to its lowest level since November 2020. The sharp moves in bonds and equities also reflects the bearish positioning of last week – CFTC bond futures were net short last Tuesday by the largest amount this cycle. There is also renewed talk within equities of the Fed being forced to pivot, helped along by UNCTAD latest report warning of a policy-induced global recession and calling on central banks to pull back from aggressive hikes (“there’s still time to step back from the edge of recession”). The Fed’s Williams and Barkin though both pushed back on any notion of a Fed pivot.

First to UK politics. The UK government has reversed a plan to scrap a cut to the top rate of income tax, keeping it at 45%. Although the walking back costs around £2-3bn out of an estimated £72.4bn worth of possible debt issuance this year, it is a sign that the government is responding to market concerns and also to polling which may mean the new government is not as cavalier as some had feared. As the say ‘a week is a long time in politics’ and if the opposition Labour continues to lead the Tory government by 33 points in the opinion polls, then further modifications may come. The FT also noted that Chancellor Kwarteng is expected to bring forward by a month his plans to unveil a medium-term fiscal statement. The plan was initially due to be set out on November 23, but will be announced later this month. That importantly means it will also be available ahead of the BoE MPC meeting on 3 November. The FT notes the statement will set out a five-year plan to show UK debt falling over time. BoE MPC member Mann was out just 30mins ago, noting a weaker pound and the UK government’s support for household energy bills were behind her push for the largest interest-rate in more than three decades last month. It suggests markets should still expect a supersized rate hike – markets price around 121bps for November and a peak of 5.6% by mid-2023.

As for data, it was a tale of ‘bad news is good news’. The US ISM Manufacturing printed at 50.9, below the 52.0 expected and was the lowest print since May 2020. The details within the report were worse. New Orders fell sharply to 47.1 from 51.3, which is also a 28-month low, and Inventories rose to 55.5 from 53.1. A ISM recession indicator which takes the difference between New Orders and Inventories is now at -8.4, its lowest since the height of the pandemic. Adding to recession expectations, the ISM chair Fiore said manufacturing could be on a path to a contraction in the first half of 2023. In more positive news on the inflation front, the Prices Paid index fell to 51.7, the lowest since June of 2020, and supplier deliveries fell to 52.4. An indicator for inflation pressures adds prices paid and supplier deliveries and this calculation is now at its lowest since March 2020. Its clear then price pressures are rolling over in goods/manufacturing, which then puts a premium on the ISM Services Index on Wednesday and Payrolls on Friday to see whether price pressure is starting to ease on the services side, and as well whether the slowdown in activity is broadening beyond the manufacturing sector (see US ISM Manufacturing for details).

The last item of news flow worth noting was UNCTAD warning advanced economy central banks risk pushing the global economy into recession followed by prolonged stagnation if they keep raising interest rates. UNCTAD Secretary-General Rebeca Grynspan called on central banks to pull back on the aggressiveness, noting “There’s still time to step back from the edge of recession”. UNCTAD estimated that a percentage point rise in the Fed’s key interest rate lowers economic output in other rich countries by 0.5%, and economic output in poor countries by 0.8% over the subsequent three years (see UNCTAD report for details). The Fed is pivoting narrative has been behind at least one bear market rally this year, and Fed officials were quick to push back on any notion. The Fed’s Barkin noted the US Fed was concentrated on US developments and that it would only worry about weakness in the global economy if it was spilling over to the US – “The thing you worry about is what collateral damage could there be to international economies and in particular their financial systems ”. The Fed’s Williams also confirmed the Fed’s hawkish path as laid out in the September FOMC projections. On the Fed is hiking until something breaks, the shar prices of Credit Suisse’s e slumped as much as 12% at one point overnight before recovering to close broadly unchanged. The sharp slide in its share price this year, around -55%, is partly due to concerns the scandal-hit bank will need to raise fresh equity capital as part of a much-needed restructuring, diluting existing shareholders.

Finally in terms of FX moves, it was commodity currencies that outperformed with the AUD +1.8% and NZD +2.1%. The general risk on tone and the surge in oil prices ahead of OPEC+ tonight driving. GBP meanwhile held on to early gains and extended in response to the UK government’s fiscal U-turn. GBP was up 1.3%.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.