Coming in for landing in a heavy cross wind

Insight

There’s a cautious mood in the markets right now.

https://soundcloud.com/user-291029717/market-cautious-over-speed-of-recovery?in=user-291029717/sets/the-morning-call

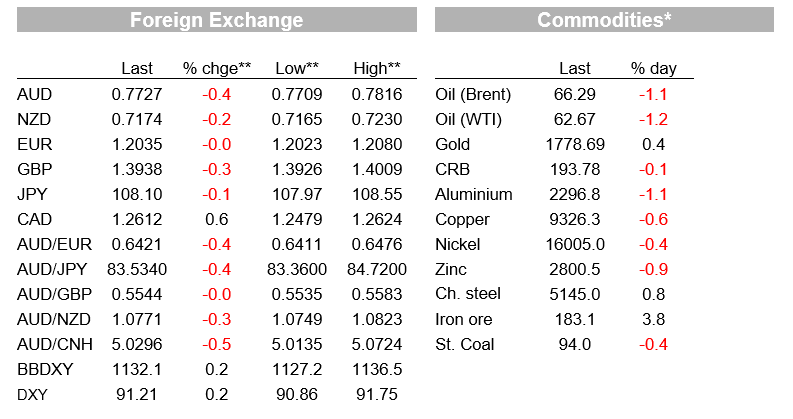

A further set back in US stocks following Monday’s decline has read through to a modest reversal in the USD’s dwindling fortunes thus far in April, and also a fresh set-back in US bonds yields back after a fleeting attempt at a rally either side of the weekend. Oil prices are lower, seeing the CAD fare worse in the G10 currency arena ahead of the Bank of Canada tonight where an announcement of QE tapering is generally expected. NZ CPI and AU retail sales are out his morning.

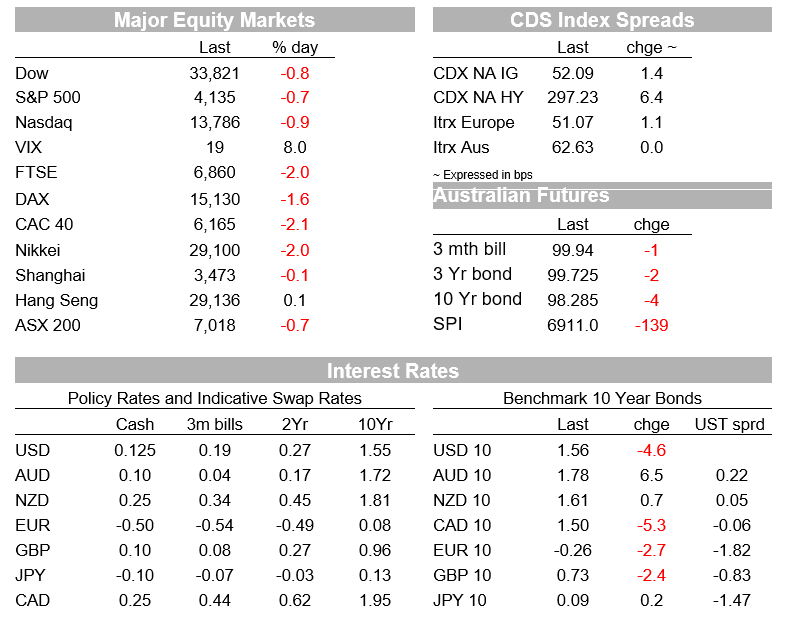

Netflix has reported its Q1 results after the bell and its stock is off over 10% after reporting a rise in new subscribers for its streaming services in Q1 of just under 4 million against expectations of more than 6 million, and expectations for adding only 1 million more in Q2 against a street consensus of more than 4 million. Netflix is blaming a limited amount of new content, partly due to covid restrictions hampering production, though one can speculate whether the positive omens regarding fuller US economic re-opening in coming quarters has limited enthusiasm for yet more stay-at-home entertainment services. Certainly not much of the $1,400 stimulus cash that most US households received in March look to have been sent Netflix’s way.

Newswires, ever needful of fitting facts to figures, are suggesting concerns about rising covid infection rates and what that means for fuller (global) economic re-opening later this year is are at least part of the story for this week’s stock set back and there may well be something to this. Certainly there is plenty of negative news around in his regards, in India, Japan, and Canada to name but three regions. In the UK, our NAB colleagues there note concerns that individuals are taking it upon themselves to act well ahead of the cautious and staged re-openings of parts of the economy, and that the risk of this leading to another wave of infections is real.

US equity indices have ended in New York down by 0.7% (S&P) and 0.9% (NASDAQ) and presumably futures market will be reacting in a negative fashion to the Netflix results and ahead of the rest of the other ‘FANNGS’ reporting in coming days. Within the S&P 500, the energy sector is by far the weakest (-2.7%) in which respect WTI crude is off just over $1. On factor here is a Bloomberg source report saying the White House plans to pledge this week a target of reducing U.S. emissions of greenhouse gases by at least half by the end of the decade as it holds a summit on climate change with world leaders. Also relevant has been news that the US House Judiciary Committee has advanced a bill that would allow the Justice Department to pursue antitrust enforcement against OPEC members. Good luck with that.

Lower oil pics have taken bites out of the CAD and NOK, down 0.6% and 0.8% respectively against the USD and the worst performing G10 currencies. CAD might also being negatively impacted by covid news, where Ontario, the country’s most populous province, is struggling to contain a sharp rise in Covid-19 cases (last Friday, Ontario Premier Doug Ford’s imposed some of North America’s toughest restrictions to get a handle on the region’s third wave of the pandemic that threatens to overwhelm its health-care system). Whether this has any implications for the Bank of Canada’s latest policy decision we will find out tonight, where the consensus expectations heading into it was that it would announce a tapering of its weekly QE bond purchases from $4bn to $3bn.

Elsewhere in currencies the USD is generally stronger in keeping the return of risk aversion evident in the US equity market, with the BBDXY index up 0.2%. AUD/USD has given back of all of yesterday’s gains seen during the APAC and early European sessions and which saw the pair break above 0.78 level for the first time since mid-March. It is back to 0.7730 now.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Read our NAB Markets Research disclaimer

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.