Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Ahead of US payrolls on Friday the decline in ADP private payrolls report overshadowed a better than expected ISM manufacturing print. The ADP miss points to downside risk to payrolls on Friday (the bad news), implying a likely delay to the Fed’s tapering decision (the good news).

Ahead of US payrolls on Friday the decline in ADP private payrolls report overshadowed a better than expected ISM manufacturing print. The ADP miss points to downside risk to payrolls on Friday (the bad news), implying a likely delay to the Fed’s tapering decision (the good news). US equities close mixed with defensive sectors outperforming. A delay in tapering expectations weighed on longer dated UST yields and kept the USD on the back foot. The AUD led the G10 gains against the USD and after a volatile night oil prices have ended the session little changed. In other news, the PBoC said it will provide low cost funding for small and medium-sized companies.

The ADP private payrolls August report revealed a 375k increase, well below the 625k expected by consensus and although the ADP report doesn’t have a great track record at predicting US non-farm payrolls outcomes, the big miss was too big ignore. Reading some of the US economists that we follow, one of the big ADP criticism is that the model is heavily influenced by the previous month’s official non-farm payrolls numbers and given the July payrolls printed a solid 943k, then the August ADP softness is worrying sign, on its own suggesting the official number of Friday has some serious downside risk. Others have also pointed out that the weakness in ADP is consistent with the softness in the Homebase data released last week. Looking at Bloomberg, the median survey for non-farm payrolls on Friday is at 725k, early last week the number was 800k and after last nights no doubt the whisper number is a lot lower with many reputable economists now calling for a print close to $400k.

A non-farm payrolls print closer to 400k rather than 800k effectively means that the Fed’s condition of “further substantial progress” in the labour market will take longer to materialise, thus delaying the tapering decision from September to November. Bad news in the labour market are good news for risk asset given the punchbowl will remain well liquified for a bit longer.

The ISM manufacturing index was the other big data release overnight and the headline reading surprised to the upside bucking the trend suggested by the softness in regional activity surveys and the national PMI . The index unexpectedly rose to 59.9 from 59.5 in July and comfortably above the 58.5 pencilled in by consensus. Consistent wit the overnight theme there good and bad news in the details. The index was boosted by increases in orders and production, up 1.8 and 1.6 points, respectively, and a surge in inventories, up 5.3 points to a three-year high. All three pointing to ongoing supply chain issues, encouragingly however the prices paid sub index, ease from 85.5 to 79. 4, still very elevated but could be suggesting the worst is behind in terms of input cost pressures. Meanwhile on the not so good front, the employment subindex fell 3.9 points to 49.9, a nine-month low.

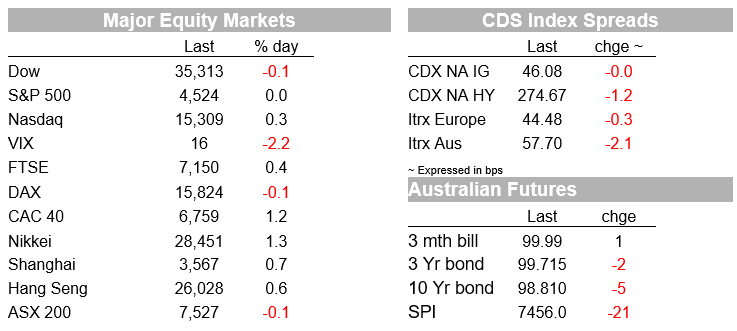

The S&P 500 ended the day flat (0.03%) with a look at sector performance revealing a clear bias for defensive stocks . Real estate and Utilities gained 1.69% and 1.30% respectively while financial and Energy were at the bottom of the pile, down 0.625 and 1.51%. The NASDAQ closed 0.33% with big tech outperforming while the industrial heave Dow fell -0.14%. Earlier in the session, EU equities closed higher with the Stoxx Europe 600 Index adding 0.5% by the close.

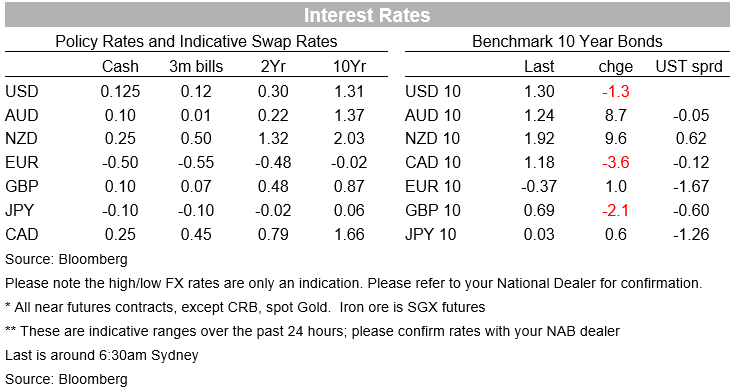

The decline in US financial stocks can be linked to the flattening of the UST curve with longer dated UST yields reversing the small uptick seen during our session yesterday with the ADP miss accentuating the move lower. 10y UST yields now trade at 1.29% 1.5bps lower over the past 24 hours, but down from 1.33% yesterday afternoon.

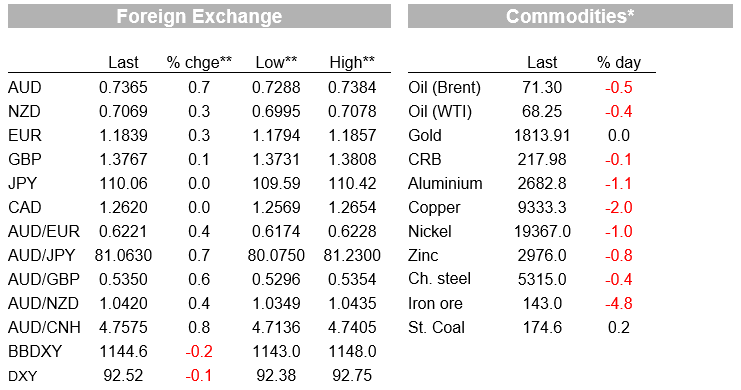

Meanwhile softness in the energy equity sector can be partly attributed to the volatility in oil prices. OPEC and friends held one of its quickest meetings in history, agreeing to stick to the plan of gradually increasing oil production through the next year, unwinding the cuts implemented at the height of the pandemic. A 400,000 barrels per day lift in supply is due next month. The news weighed on prices, pushing Brent oil down to a low $70.58, but then we saw a reversal in the price action after the EIA reported a larger than expected drop in crude stocks last week . WTI and Brent ended little changed at $71.31 and 68.22 respectively.

The move lower in longer dated UST yields and push back on Fed QE tapering expectations weighed on the USD with the DXY and BBDXY index down 0.12% and 0.2% over the past 24 hours. The AUD has been the top G10 performer, up 0.67% to 0.7366, after trading to an overnight high 0.7378. The AUD has continued it recent pattern of easing a little during our APAC session, only to then regain momentum during the overnight session. In a similar fashion the NZD has recovered further, up 0.5% overnight to 0.7070, getting closer to the first resistance level of 0.71 . A break of that would see the technicians eyeing up the 0.7315 mark, which was the resistance level through much of the first half of the year.

Looking at FX majors, the Euro has retained its recent ascendency bias now trading at 1.1839, GBP continues to find resistance around 1.38 ( now at 1.377) and USDJPY trades at ¥110.38 little changed over the past 24 hours.

Finally on other news, the PBoc has announced it will provide ¥300 billion yuan ($46.bn) of low-cost funding to banks to help them offer more support to small and medium-sized companies. The target stimulus is consistent with the recent message from officials who have shown a reluctance to favour large-scale stimulus.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Conditions ease as slow growth weighs on firms

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.