Robust growth for online retail sales observed in June

Insight

There’s been big increases in equity markets and bond yields on news of a successful stage one vaccine trial in the US.

https://soundcloud.com/user-291029717/markets-go-vaccine-crazy?in=user-291029717/sets/the-morning-call

“Are we gonna let the elevator bring us down; Oh, no let’s go, go crazy; I said let’s go, go crazy; Let’s go, let’s go, go, let’s go”, Prince 1984

Headline reports that a COVID-19 vaccine might be in sight drove it early in the session with Moderna reporting very promising results from its phase 1 study, concluding its mRNA-1273 vaccine “has a high probability to provide protection from COVID-19 disease in humans”. If phase 2 and 3 are successful, a vaccine could be possible as early as the northern hemisphere Autumn (Sep/Oct 2020).

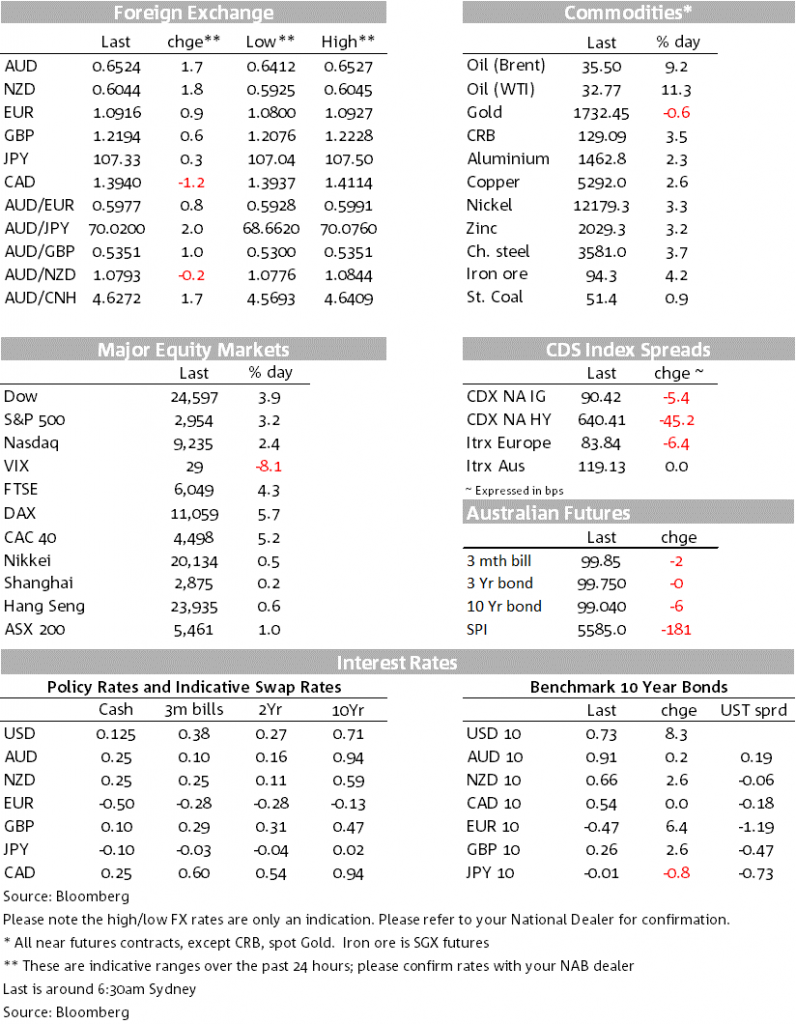

Also adding to positive sentiment was China flagging more stimulus at the upcoming National People’s Congress starting from Friday, the EU gradually inching closer to a €500bn recovery fund, and Fed Chair Powell’s 60 Minutes Interview where he noted he wouldn’t bet against the US economy and the Fed had plenty of policy ammunition. Equities surged with the S&P500 +3.2% (Moderna stock was +20%), while the USD dollar and other safe haven FX fell (USD DXY -0.7%) with commodity-linked/global growth proxy FX rallying sharply (AUD +1.7%, NZD +1.8%, USD/CAD -1.2%, and USD/NOK -1.4%). Bonds fell with yield curves steeping (US 2yr yield +3.5bps and US 10yr yield +8.3bps to 0.73%). Oil surged (WTI +11% to $32.77), driven by both the surge in risk sentiment and also on reports Chinese oil demand is nearly back to levels seen before China’s lockdown.

Moderna reported very promising results from its phase 1 study, concluding its vaccine “has a high probability to provide protection from COVID-19 disease in humans”. The data is from a phase 1 trial of 45 people aged 18-55 with levels of binding antibodies in blood samples on par with those who had recovered from COVID-19. Importantly the vaccine was said to be generally safe and well tolerated. A phase 2 study will soon commence on 600 patients and a final phase 3 will likely start in July. Should phases 2 and 3 go as expected, a vaccine could be ready for emergency use as early as the fall (Sep/Oct 2020) (see Moderna for details). While it is still early days in vaccine development and some question the rally in equities in response, it is worth noting that Australia’s Peter Doherty a noble prize winner in immunology on ABC’s 7.30 said he was bullish on the possibility of a vaccine. Professor Doherty noted that a number of vaccines have worked at the animal stage and the specific types of vaccines being trialled generally have low risk in humans (see 7.30 for details). For markets then it seems it’s a matter of when (rather than if).

Sentiment was also buoyed by China flagging more stimulus at the upcoming National People’s Congress starting from Friday. On Sunday China issued guidelines on developing the western regions so western China will be on par with the eastern regions by 2035. The plan calls for similar levels of public service, infrastructure connectivity and living standards. As part of the plan, fiscal, taxation, financial, industrial as well as land policies will be used. Last Friday the Political Bureau also met and discussed the draft government work report, noting “proactive fiscal policy should be more positive, the prudent monetary policy should be more flexible and appropriate”.

Oil prices took their que from China with reports of Chinese oil demand being nearly back to levels seen before China’s lockdown, around 13m barrels per day according to those on the ground. Aligning with notions of oil demand coming back, air pollution in China is now above 2019 level according to analysis of 1,5000 air quality monitoring stations in China. Concerns around the coronavirus are also seeing people choose private cars over public transport. The increased demand comes at a time when production is falling, supported by the big cuts by OPEC+ producers and low oil prices encouraging US shale producers to stop drilling. Brent crude has breached the USD35 mark overnight.

Also boosting sentiment in early Asian trade was Chair Powell’s remarks late Sunday (early Monday AEST). In his 60 Minutes interview he noted the recovery “may take a while…it could stretch through the end of next year”. But importantly, he also noted “in the long run, and even in the medium run, you wouldn’t want to bet against the American economy. This economy will recover”. On the question of negative interest rates, he reiterated the unanimous view of the FOMC that it is not an appropriate or useful policy “…there’s no clear finding that it actually does support economic activity on net…it introduces distortions into the financial system which I think offset that”. (see the 60mins transcript for details)

Last week Governor Bailey said that negative rates weren’t currently being planned for or contemplated. In a weekend interview Chief Economist Haldane seemed to contradict that, saying that the Bank was examining unconventional monetary policy measures, the suite of which included negative interest rates. That later remark saw GBP decline in early Asia yesterday before recovering. Overnight MPC member Tenreyro said that negative rates shouldn’t be ruled out, “everything is on the table for us”.

The final factor that drove the rebound was the EU appearing to be inching closer to a €500bn Euro recovery fund. Germany and France have agreed to support the €500bn Recovery Fund, although it still requires the support of the rest of the 27 EU members to get off the ground. Funds would be raised by the European Commission borrowing on capital markets and then distributed to needy nations in the form of grants than loans. This latter distinction is important and still faces opposition from some nations, including Austria, the Netherlands, Denmark and Sweden.

It’s no surprise to see the USD on the backfoot with the DXY -0.7%. Other risk haven currencies have also fallen with USD/Yen +0.3% to 107.33. Gains against the USD were led by the commodity-linked or global growth proxies with notable moves in AUD (+1.7%), NZD (+1.8%), USD/CAD (-1.2%) and USD/NOK (-1.4%).

Can the rally in risk sentiment be sustained? It is possible with more reports of countries/US states easing containment restrictions – California the latest as I hit send. There is also growing evidence that the global economy troughed in mid-April with high frequency data such as Apple/Google mobility pointing to a pick-up in activity. Sentiment indicators are also now starting to rebound (though harder data will likely lag for another month). The latest indication of that was the US NAHB Housing Market Index which rose to 37 from 30 in May. The flash PMIs on Thursday will be closely watched in this vein.

A busy day ahead that kicks off domestically with Weekly Consumer Confidence that has now risen for six consecutive weeks. Weekly Payrolls data is also out with some hint it may point to the first signs of some improvement in labour market conditions with a small sample ABS Household Survey seeing increases in employment and hours worked. The RBA Minutes also released are unlikely to contain much given the detailed SoMP was released earlier in May. Overseas, key items include the ECB’s Chief Economist talking, UK Unemployment Data and the Fed’s Powell testifying before the Senate Banking Committee. Key releases in detail:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Robust growth for online retail sales observed in June

Insight

Coming in for landing in a heavy cross wind

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.