Online retail sales growth slowed in May following a fairly strong April

Insight

Bond yields are pushing lower and market volatility is easing.

https://soundcloud.com/user-291029717/markets-going-nowhere-yet-us-job-openings-boom?in=user-291029717/sets/the-morning-call

She’s running to stand still – U2

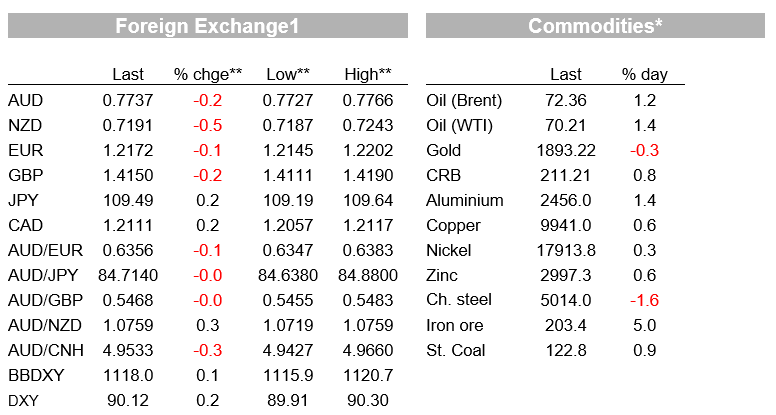

US equities traded in and out positive territory ending the day close to flat. After a day of consolidation, UST yields resumed their decline with solid US data releases again reflecting issues with supply constraints. The USD has eked out small gains with NZD the underperformer.

Ahead of the May US CPI release tomorrow night, markets are essentially running on the spot perhaps wary over the potential for US inflation data to surprise on the upside . Both the headline CPI and core readings are expected to climb by 0.5% to 4.7%yoy and 3.5% yoy respectively, that said details on the CPI print are going to be important, another strong print may trigger a little bit of market volatility, but if the rise in prices is again driven by temporary factors, then a higher CPI reading is not going to be enough to move the Fed’s dovish stance.

Indeed, one could also argue that last week solid but not super strong US labour market report, provides the Fed with plenty of ammunition to keep the QE punchbowl well liquified without any need to talk about tapering. Favouring the current subdued market volatility.

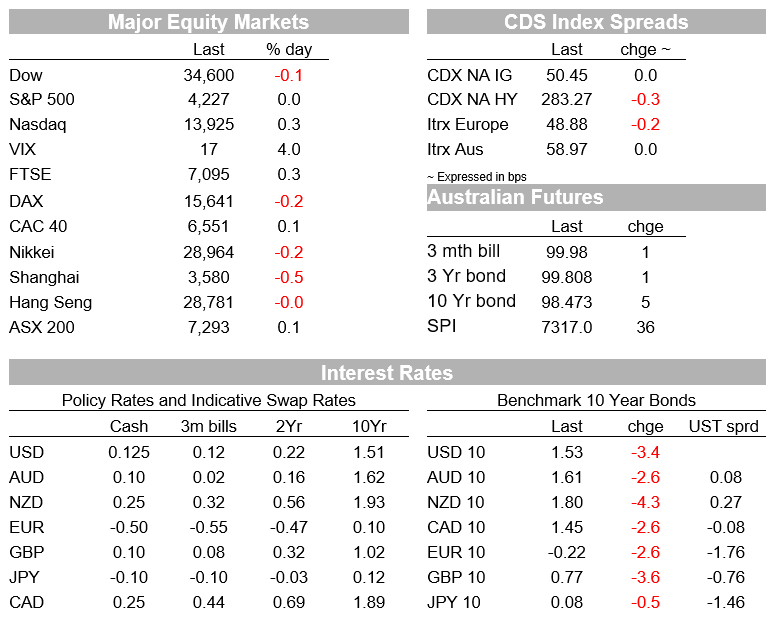

On this score we note that overnight US data releases printed mostly on the solid side with little market impact. Indeed, after consolidating in the previous night, UST yields resumed their decline notwithstanding JOLTs (job openings) report revealing numbers in the US which were high enough for everyone to have a job, but to attract workers companies are having to lift their wages ( see more below). Both the 10 and 30y tenors fell by 4bps to 1.5280% and 2.2165% respectively and ahead of the $38bn 10y UST Note auction early tomorrow morning, overnight the 3-year auction was well received marginally through the mid-level at the time and with 2.47 bid-to-cover ratio vs. a 2.44 average in the prior six auctions..

Meanwhile US equity markets traded in and out of positive territory before ending the day close to flat. The S&P 500 closed +0.02%, NASADQ was +0.31% and the Dow -0.09%. Early in the session, European equity indices closed mixed, although the Euro Stoxx 600 index eked out a small gain, rising to a third straight record high. The index gained 0.1% with Travel & leisure (+1.8%) plus real estate (+1.1%) outperforming.

Currency markets have also been quiet, the USD is a tad stronger in index terms (BBDXY and DXY ~ +0.14%) with a notable underperformance of commodity currencies. The NZD down 0.5% from this time yesterday, slipping below 0.72, the AUD is -0.14% and now trading at 0.7742 while CAD is -0.19% at 1.211. The decline in these pairs is somewhat surprising given commodities actually had a good night with gold the only small underperformer (-0.24%) while lead, metals oil and Steam coal recorded gains close to or above 1%.

Bloomberg’s commodity price index up 0.6% and looking to close at its highest level in six years. Indeed, both the WSJ and FT have published articles on the “super-cycle” for commodities, the tone of which is that higher commodity prices could spill over to higher CPI inflationary pressure, more so than is widely acknowledged. Capital spending on major commodity resources has been lagging over the past decade, driving inventories to a two-decade low and reducing supplies, at a time when global demand has increased, and there is no quick fix.

JPY and GBP are the other two notable underperformers , both down 0.23% over the past 24 hours. JPY’s moves again seems unjustified given the declines in UST yields while GBP’s decline could be linked to concerns the country’s exit from lockdown may be delayed plus rising tensions between Britain and the EU. Brussels is ready to consider tougher retaliatory measures if the UK government fails to implement post-Brexit obligations over Northern Ireland.

Looking at the overnight data release in more detail. US job openings and the quit rate both jumped to record highs in April, a sign of a strong and active labour market . Meanwhile the number of vacancies exceeded hires by 3.2m, the biggest gap on record, an indication of hiring challenges for businesses reflecting skills mismatches, overly generous unemployment benefits that are keeping folk from re-joining the labour force, fears of catching COVID19 in the workforce and closed schools that have increased child care obligations.

The NFIB small business survey showed similar themes in its labour market indicators while the headline index unexpectedly slipped a little – the index is sensitive to political developments and could reflect the fear of higher taxes according to Pantheon Macroeconomics. Inflationary pressure continued to build, with a net 40% of businesses saying they raised selling prices, a record high level for the survey that dates back to 1986, and a net 43% said they would raise prices in the next three months.

In Europe, Germany industrial production fell 1% in April, which some put down to supply chain disruptions. The ZEW survey of expectations showed a dip in the expectations component but the current conditions index rose to a two-year high . Q1 GDP figures for both the euro-area and Japan were both revised higher, now showing smaller contractions of 0.3% q/q and 1.0% q/q respectively.

In local news, former RBA board member John Edwards tells Bloomberg he doesn’t expect yield target to be extended to Nov. ’24. “ To commit to it really does lock them in a bit on the timing of moving the cash rate,” Edwards said adding that “It’s an unnecessary risk because they can at any point between now and April ’24 announce an extension if things go unfavourably.”

Edwards also noted the increase in fixed rate borrowing is not something the RBA would “really welcome”, providing another argument for not prolonging the three-year fixed-rate target.

In terms of QE, Edwards emphasises the importance of QE restraining the potential for the AUD to appreciates, noting the RBA will want to keep the QE capacity and expectation that it’ll intervene if the 10-year yield moves so quickly and at such magnitude that it rekindles an appreciation of the Australian dollar. Presumably along the lines of the BoJ approach, Edwards then suggests the RBA could simply restate a commitment to not let the 10-year yield get too far out of line with what the RBA would describe as the fundamentals rather than committing to another tranche of buying.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.