Online retail sales growth slowed in May following a fairly strong April

Insight

There’s still talk of a v-shaped recovery in the US.

As long as I’m living, I’ll be waiting, As long as I’m breathing, I’ll be there

Whenever you call me, I’ll be waiting – Lenny Kravitz

US equities ended the week on a positive note, but still down for the week, the USD lost a bit of ground on Friday, but was broadly stronger on the week and despite all the market volatility the AUD was little changed on Friday and for the week. Markets appear to be in need of a new catalyst, US earnings could be the one with 173 S&P 500 companies reporting this week while major central banks could be the other with the BOJ, FOMC and ECB meetings this week.

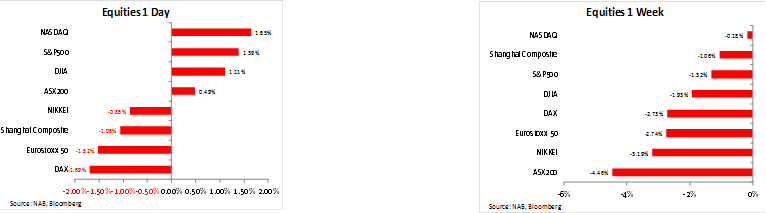

Technology shares led the rise in US equities on Friday with the NASDAQ index leading the charge and closing the day at 1.65%. The S&P 500 ended the day at 1.35% with the tech sector the outperformer. The energy sector was little changed notwithstanding further gains in oil prices (WTI +2.68% Brent +0.52%). The oil market was buoyed by news US operators have continued to shut wells down, Baker Hughes reported a 14-year drop in US oil drilling, down to 378 vs 438 prior. Gilead helped sentiment in the NY afternoon, following news the company is set to report the first results from a company-sponsored study of the experimental drug Remdesivir on COVD-19 patients . Data and results from 400 severely ill coronavirus patients being treated with Remdesivir in an open-label study are expected before the end of this week.

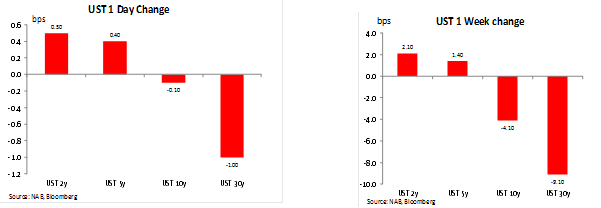

10y UST yields were little changed on Friday, ending the week at 0.60%, 4bps lower on the week. That said the 30y year part of the curve continued to drift lower, down 1bps on the day and 9bps on the week to 1.172%. There has been a fair bit chatter on the deflationary forces challenging the US economy at the moment with the US break even curve suggesting US inflation is not expected to get back above 2% over the next 10 years ( the 10y tenor is now at 1.21%).

So looking at the week’s performance lower longer dated UST yields along with lower global equities do leave us with a sense of cautiousness in the air. On this score is probably worth noting that the S&P 500 closed at 2836, below the 2935 61.8% retracement level from the February/March decline, keeping many technical analyst with a bearish medium term bias, including our in-house TA analyst, David Coloretti.

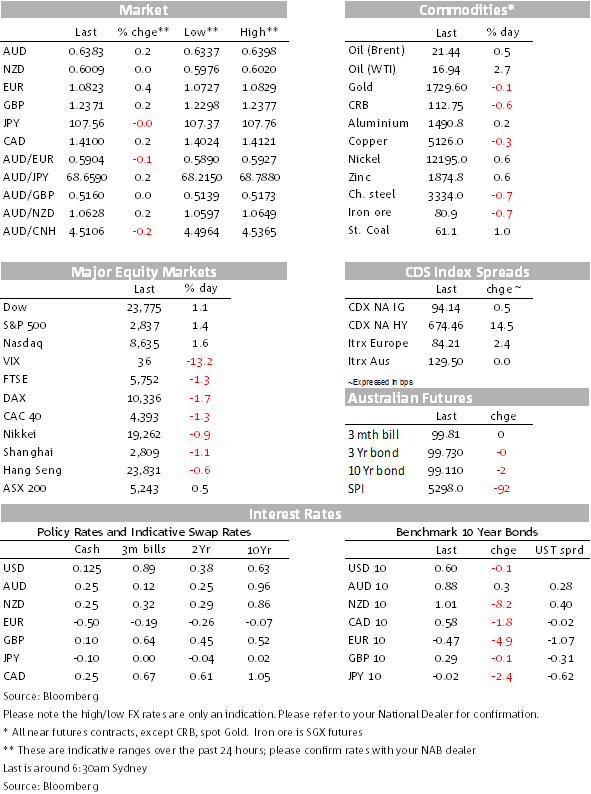

Italian BTPS continue to outperform (10y down 14 bps to 1.83%) following news Italy avoided a downgrade below high-grade status as S&P reaffirmed the country’s BBB rating. The rating agency said it could lower Italy’s credit rating if its public debt levels failed to move towards a clearly discernible downward path over the next three years.

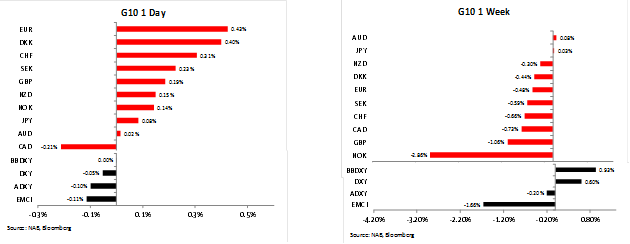

The Euro was Friday’s highlights, snapping a four day losing streak against the USD and now it starts the new week just above 1.08 mark. The union currency traded to a weekly low of 1.0727 following a dire German IFO survey, but the Italian rating news helped currency recover later in the session.

German business confidence extended its slump in April to a record-low 74.3, well below market’s expectations at 79.7. “Sentiment at German companies is catastrophic,” said Ifo President Clemens Fuest. “Companies have never been so pessimistic about the coming months. The coronavirus crisis is striking the German economy with full fury.”

Despite losing a bit of ground on Friday, the USD still had a solid week, up on index terms against majors (BBDXY +0.95%, now @1260, DXY +0.60% now @100.23), Asia (0.20%) and EM (1.66%). NOK was the G10 underperformer, down -2.66% over the past 5 days to 10.6226, reflecting its high degree of sensitivity to oil prices and the other notable underperformer was GBP, down 1.06% to 1.2367. UK Brexit and COVID-19 uncertainty weighed on the pound while NZD and AUD where little changed.

The AUD starts the new week at 0.6387 and NZD is at 0.6012. This could be an important week for antipodean currencies, both are very risk sensitive with the AUD in particular showing a higher degree of sensitivity to the performance of US equity markets in recent times. As noted above, the big number of US companies reporting their earning this week could be a big test for equity markets.

US data releases didn’t elicit much of a market reaction, but for the record March Durable goods orders fell 14.4%, worse than the consensus at -12.0%. Notably, ex-transport orders dipped only 0.2%, better than the -6.5% expected by economists. The big plunge in total orders was due primarily to the huge wave of cancellations for Boeing 737MAX aircraft – which subtracted 9.9% from the headline number, and an 18% drop in orders for autos and parts, subtracting 4.4%. Behind this noise, core capital goods orders were little changed, leaving Q1 as a whole exactly unchanged from Q4. Consistent with this view and bearing in mind the preliminary US Q1 GDP is released later this week, the Atlanta Fed GDP tracker has Q1 at -0.3% while the St Louis tracker is at -0.25%. These numbers are just a prelude to be big collapse expected in Q2.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.