Consumers lead the way

Insight

ECB now seen hiking by 50bps tomorrow and then again in September

https://soundcloud.com/user-291029717/markets-set-for-a-tougher-ecb?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

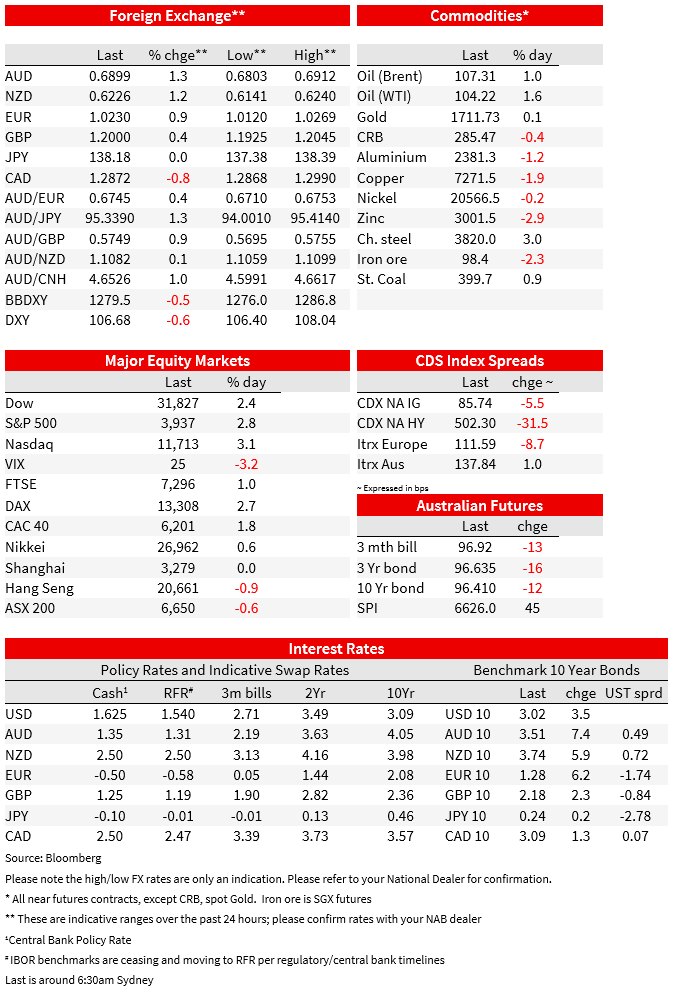

US and European equity markets jumped overnight in a broad rally that has been led by tech stocks. The NASDAQ outperformed, up over 3% with the VIX index easing down to 24. The news flow has been very Eurocentric with report suggesting the ECB is considering hiking by 50bps tomorrow while Gazprom looks set to restart gas flow to EU via Nord Stream but only partially and the EU considering a 15% reduction in gas demand. Core global bond yields are higher while in FX the USD is broadly weaker with the euro and pro-growth currencies outperforming. AUD is flirting with a move back above 69c.

In addition to a tech led rally in equities (more below), the main news flow has been mostly about Europe which has lifted the euro back above 1.02 with core European yields also broadly higher. The move up in the currency and EU yields was sparked by an ECB source Reuters report and since repeated by Bloomberg suggesting the Governing Council is more open to a 50bps move on Thursday. Previously ECB President Lagarde had signalled a preference for a 25bps hike, although with the caveat that the decision was dependent on the data flow and developments ahead of the meeting.

Reaction to the report trigged a move up in yields with the market quickly moving to price a 50bps hike tomorrow (now 75% priced). Of note, the ECB the has good form in delivering what the market expects when rate hikes are priced over 70% as it is currently the case. Expectations now are not only for a 50bps hike tomorrow, but for the Bank to deliver another 50bps hike in September as well. Messaging from ECB Council members has been by and large supportive of a 25bps hikes, but similar to the Fed and other central banks, it seems the ECB is now taking the approach of using the media to prepare the market for a different outcome relative to what it has been communicating in recent times. Before adding any more comments on this point, lets wait and see what the ECB does tomorrow.

In another media report, according to “people familiar with the matter”, Gazprom will resume gas flows into Europe via its Nord Stream pipe, albeit at a reduced capacity, after the Russian gas giant declared force majeure on some European clients. Flows were capped at 40% of capacity before the maintenance work began last week. Also, overnight and consistent with the Gazprom news, Bloomberg reported the EU is set to propose a voluntary 15% cut in natural gas use by member states starting next month on concern Russia may halt supplies of the fuel . The goal would be embedded in a regulation accompanying a demand-reduction plan the European Commission is scheduled to unveil Wednesday to cope with a potential full cut off by Moscow.

We also had news on the ECB fragmentation tool with Reuters noting the ECB will announce its anti-fragmentation tool, designed to support vulnerable peripheral government bond markets like Italy’s, with countries needing to meet European Commission targets to participate. Italy’s 10-year bond spread to Germany narrowed only marginally, with investors seemingly waiting for the full details of the scheme to be announced. The anti-fragmentation tool comes at an important juncture for the European bond market, with Italy experiencing another bout of political turmoil after PM Draghi offered to resign late last week. Draghi is due to address parliament tonight amidst reports of further fractures in his coalition government, with the right-wing League and Forza Italia parties saying they would no longer work with the Five Star party.

European equities gained for a third day following the news above, but it is hard to see the nature of the rally as anything but one of a relief kind, rather than based on strong fundamentals. No energy means no growth and an aggressive ECB hikes are not going to help the growth outlook either. Banks, which benefit from higher rates, led gains with the Stoxx Europe 600 Index ending the day comfortably above 1%.

Equity markets also rebounded strongly in the US with the S&P 500 closing the day up 2.76% while the NASDAQ gained 3.11%. All 11 sectors of the S&P 500 closed in the green with the index recording is biggest daily gain in almost a month. Mega IT stocks where big winners with Apple and Alphabet bouncing back from Monday’s losses. After the bell Netflix shares gained ~ 8% after the streaming-video company reported 2Q results that showed subscriber losses weren’t as bad as expected.

So it has been a risk positive night, but recession fears certainly haven’t gone away and the rebound in equities over the past week could as much reflect a recovery from oversold levels and extreme levels of pessimism. To this point, Bank of America’s closely watched Fund Manager Survey showed investors’ equity allocation was its lowest since the GFC while cash levels were at a more-than 20-year high, indicative of a very cautious stance towards risk assets. When investor sentiment reaches bullish or (in this case) bearish extremes, it sometimes leads to a contrarian reversal.

Moving onto FX, the improvement in risk appetite sees the USD broadly weaker with the Euro and pro-growth currencies outperforming. As noted above the euro was lifted by the increase in ECB rate hike expectations, euro now trades 102.27, but one can’t help the feeling this is going to be yet another classic case of buying the rumour and selling the fact given uncertainties to the European outlook and lots of question marks on ECB’s approach including be the ECB’s anti-fragmentation tool, which we see as still not ready and thereby risks disappointing markets.

NOK (1.82%) and SEK (1.64%) are at the top of the G10 leader board, reflecting their high euro beta nature. Then AUD and NZD are not far behind, up around 1.20%, the AUD is flirting with a more sustained move above 69c, now trading at 0.6898, after printing an overnight high of 0.6012. Yesterday the minutes to the RBA’s July policy meeting and RBA Deputy Governor Bullock’s speech yesterday were seen as hawkish, contributing to a 10bps increase in the 3-year Australian bond rate. The cash rate remains a long way below ‘neutral’, and the central bank’s initial aim appears to be to remove stimulatory conditions reasonably quickly given the extremely tight labour market and intense inflationary pressures. RBA Governor Lowe is speaking this morning, with the market pricing around a 30% chance of a 75bps hike for next month’s meeting, but the key event ahead of the next rate decision is next week’s CPI release.

The media is reporting details of the review into the RBA. The review will be independent to the RBA and carried out by BoE external Financial Policy Committee member Carolyn Wilkins, Professor Renee Fry-Williams from the ANU (whose husband Warwick McKibbin is a proponent of nominal GDP targeting) and senior public servant Gordon de Brouwer.

The Committee will report by March next year, by which time NAB would expect much of the current phase of monetary tightening to have concluded. From the media, the terms of reference reportedly include: (i) looking at appointments to the Board (critics suggest there are insufficient monetary theoreticians to challenge the RBA staff), (ii) the transparency of messaging (a press conference after each Board meeting and a formal vote on decisions could be likely outcomes); (iii) the appropriateness of the inflation targeting regime (any change to the 2-3% target higher or lower would be important for policy expectations – we’d be surprised if the target was changed); (iv) the performance of the RBA in achieving its inflation target (the Bank is likely to face criticism for consistent undershooting in the pre-pandemic era and for massively overshooting in recent times) – this effectively reflects poor forecasting and arguably an over-reliance on forecasting models. It may mean the RBA is more reactive to inflation in coming years; (vi) the Bank’s policy actions during the pandemic (the Bank is likely to sustain significant criticism for its policies as the economy recovered and its incorrect forward guidance, which in turn reflected its poor forecasting performance); and (vii) how monetary policy, fiscal policy and banking policy interact when interest rates are close to zero/the RBA has limited room to work.

This would seem to be a positive development during the pandemic when all arms of policy worked together. Again, the conclusion is likely to be that the RBA erred in not reversing policy accommodation earlier as vaccines were rolled out, inflation picked up and unemployment fell sharply.

The NZD has appreciated strongly in sympathy with the EUR, to which it has been highly correlated in recent times, moving from around 0.6160 this time yesterday to 0.6220 this morning. Overnight, the GDT dairy auction saw a 5% fall in the price index (5.1% for whole milk powder), the eighth fall of the past nine auctions.

In the UK, Bank of England Governor Bailey flagged a possible 50bps rate hike next month, saying “a 50 basis point increase will be among the choices on the table when we next meet” given upside inflation risks, while adding that the committee hadn’t made a decision yet. There hasn’t been much market impact from Bailey’s comments with the market already close to fully-pricing such a move, the GBP underperforming overnight, up 0.4% to just below 1.20.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Consumers lead the way

Insight

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.