Online retail sales growth slowed in May following a fairly strong April

Insight

Big gains in US equities on Friday help extend rally for a second week

Events Round-Up

NZ: ANZ consumer confidence, Oct: vs. 85.4 prev.

JN: Tokyo CPI ex fr. Food, energy (y/y%), Oct: 2.2 vs. 2 exp.

JN: BoJ 10yr yield target (%), Oct: 0 vs. 0 exp.

GE: GDP (q/q%), Q3: 0.3 vs. -0.2 exp.

GE: CPI (EU harmonised, y/y%), Oct: 11.6 vs. 10.9 exp.

CA: GDP (m/m%), Aug: 0.1 vs. 0 exp.

US: Employment cost index (q/q%), Q3: 1.2 vs. 1.2 exp.

US: Personal income (m/m%), Sep: 0.4 vs. 0.4 exp.

US: Personal spending (m/m%), Sep: 0.6 vs. 0.4 exp.

US: Core PCE deflator (y/y%), Sep: 5.1 vs. 5.2 exp.

US: Pending home sales (m/m%), Sep: -10.2 vs. -4 exp.

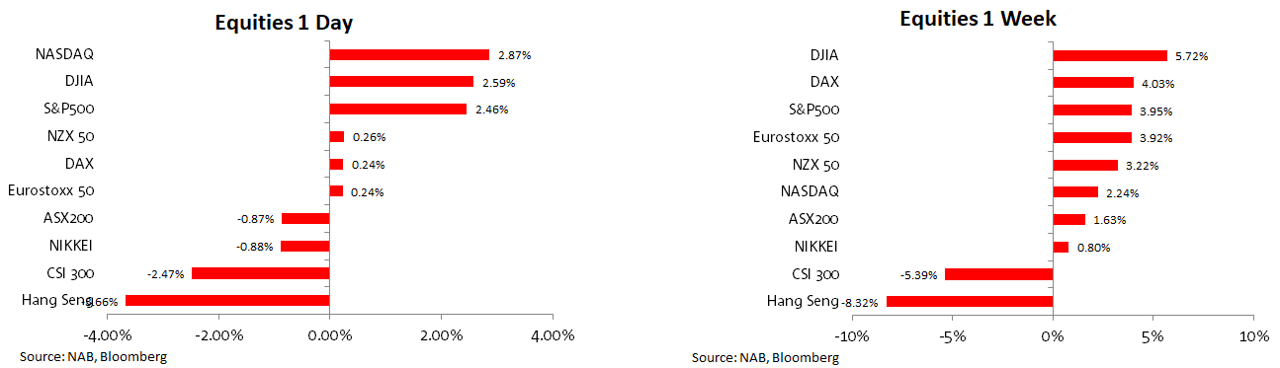

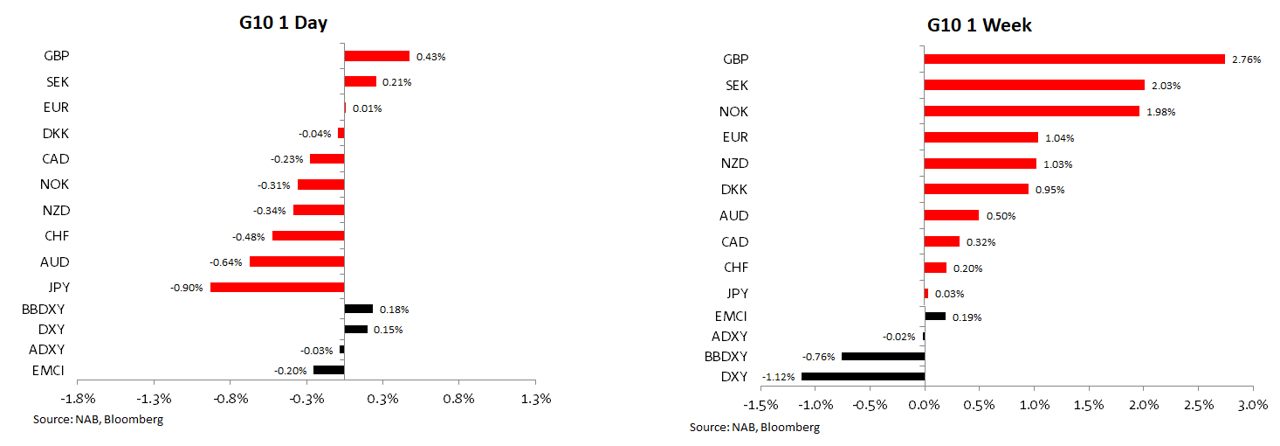

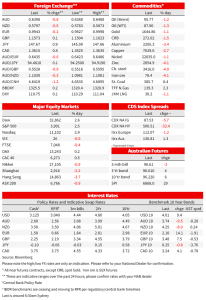

US equity markets rebounded strongly on Friday with gains in Apple shares more than offsetting the decline in Amazon. The underwhelming results by some big US tech. companies was not enough to deter the market from recording a second consecutive week of gains. Meanwhile, the rally in core global yields came to an end on Friday, following record inflation prints in Germany, France and Italy. A reminder that Central Banks’ fight against inflation is not over yet. The USD was broadly stronger on Friday with the AUD and NZD underperforming notwithstanding the improvement in risk appetite evident in the US equity market. GBP was the outperformer on Friday and on the week, rebounding from an oversold position with the euro the other notable weekly performer.

US equities enjoyed a strong rebound on Friday with gains in Apple shares (up 7.6%) a strong contributor, more than offsetting the decline in Amazon ( -7%), after the latter revealed disappointing earnings results on Thursday. The S&P 500 Index climbed 2.5%, more than reversing the aggregate 1.35% decline in the previous two days, closing the week up 3.95%, a second consecutive weekly gain. On Friday the NASDAQ jumped 3.2%, while the Dow rose 2.5%.

Meanwhile on the other side of the Atlantic, European equities had a mixed Friday but the broad EU Stoxx 600 index managed to scrape a 0.14% gain on the day. That being said along with the Dow (US industrial heavy index) European equities were the weekly outperformers, with the DAX up just over 4%. In contrast, China was a notable underperformer on the week with investors likely expressing disappointment at the lack of pro-growth rhetoric coming from President Xi at the National Congress while support for the zero-covid policy with no hints over a potential unwind of restrictions was also disappointing. China CSI 300 index fell 5.39% on the week with the Hang Seng down 8.32%.

Notwithstanding concerns over downward revisions to earnings given the aggressive coordinated policy tightening around the globe, so far the US reporting season is showing resilience with some big tech. companies the exception. 71% of S&P 500 companies that have reported their earnings have beaten expectations, slightly below the 5-year average of 77%. Those with a positive inclination may look at October’s equity performance as a sign of a new uptrend while others would suggest we have not yet seen the worse given the lag effects from monetary policy and the prospect of still more tightening to come.

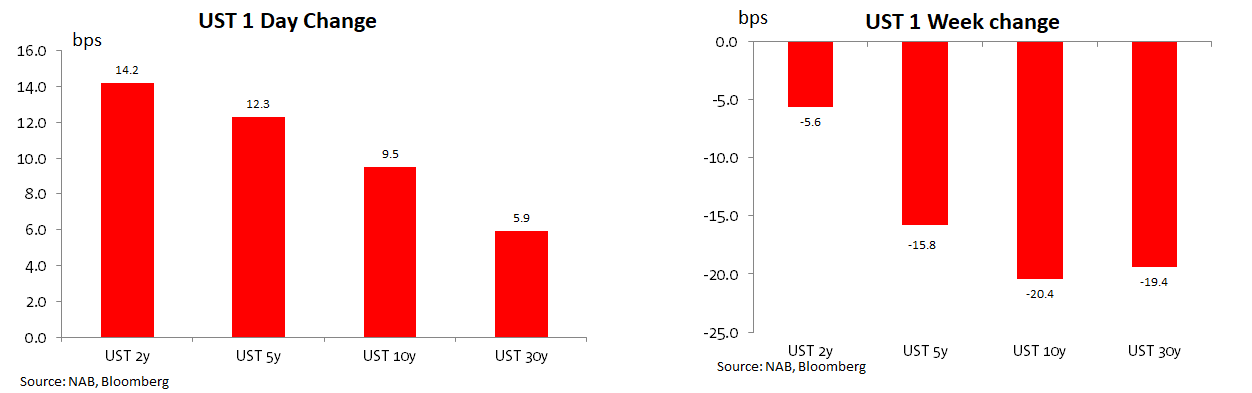

he policy tightening debate was another theme on Friday, the market has been looking for signs central banks may be looking to slowdown their pace of tightening with the BoC last week supporting this notion (and the RBA previously) while the ECB on Thursday was seen as joining this boat after the ECB statement dropped ‘several meetings’ line, citing ‘substantial progress’ on policy . A factor that contributed to the positive vibes in equities last week amid decent declines in core global bond yields. This narrative, however, was challenged on Friday with much stronger than expected European inflation numbers. German headline CPI hit an annual rate of 11.6% in October, well above the 10.9% expected by economists, while Italy (11.9% vs. 9.5% exp.) and France (7.1% vs. 6.5% exp.) also beat expectations.

Reaction to the numbers triggered a sell-off in core global bonds with European bonds leading the move up in yields. 10y Bund yields jumped 14bps to 2.095%, while pricing expectations of ECB policy tightening also reversed the declines recorded in the previous day. Pricing of the deposit rate for December declined to 1.96% on Thursday, but after the data releases on Friday, pricing closed the week at 2.01% while expectations for the deposit rate next year in September jumped from 2.28% to 2.78%, still below the 3.20% priced early in October, but a decent move relative to Thursday’s levels. Speaking to the Irish national broadcaster RTE’s , ECB President Lagarde renewed her pledge to tame consumer-price growth, saying that “defeating inflation is our mantra, our mission, our mandate.”

The UST curve bear flattened on Friday after a 14bps jump in the 2y rate to 4.419% while the 10y rate gained 9.5bps to 4.01%. US inflation/Wage data releases were mixed, but arguably the main take away is that inflation numbers are still too high, supporting the notion the Fed will lift the funds rate by 75bps this week to 4% and keep a hawkish guidance ( will they leave the door open to another 75bps hike in December?).

One of the Fed’s preferred core inflation readings accelerated in September although by a slightly smaller magnitude than expected (core PCE was 5.1%yoy, up from 4.9% previously, vs 5.2% exp.), while the employment cost index (ECI) edged down, but only moderately. The 1.2% increase in the ECI marks the second straight marginal slowdown, after gains of 1.3% and 1.4% in Q2 and Q1, respectively. That said, encouragingly the slowing in the key component, private sector wages and salaries, was more pronounced; the 1.2% Q3 increase followed an alarming 1.6% jump in the second quarter. As a result, the y/y rate slowed to 5.3% from 5.7%. Still very high, but a decent decline in Q3 nonetheless.

Looking at the week’s performance, core global bond yields still enjoyed decent declines with 10y UST yields down 20bps relative to levels a week ago. Honorary FOMC member, WSJ Timiraos who wrote earlier in the week that the Fed was considering downshifting to a 50bps hike in December having a longer lasting impact, notwithstanding solid inflation data over the past week.

As for other US data release, US personal spending was stronger than expected in September, rising 0.6%, with households continuing to rundown their large stockpile of savings accumulated through the pandemic (estimated to still be in the region of $1.4tn. While the bad news in the US housing market continued on Friday with September pending home sales plunging by 10.2%, significantly below the consensus, -5%.

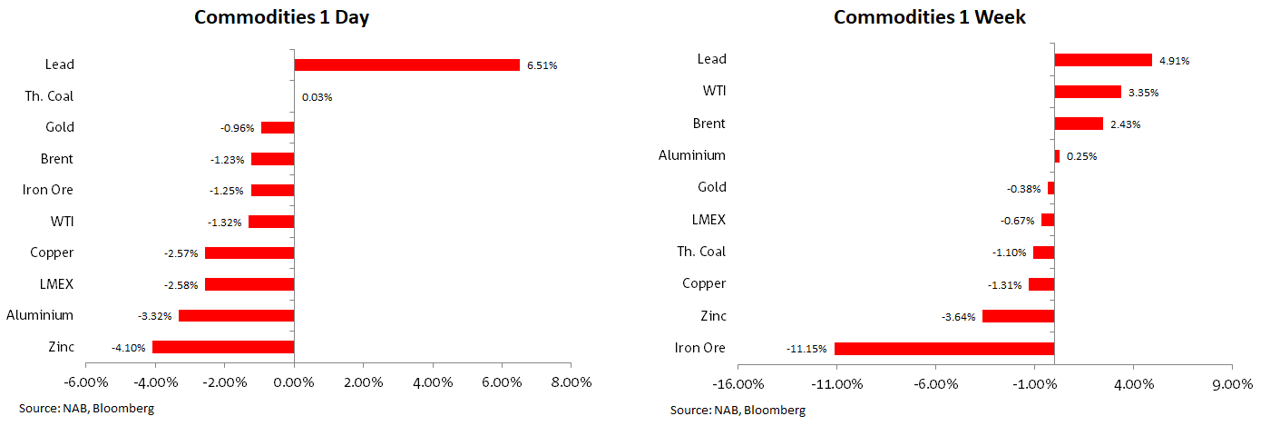

Moving onto FX, the USD was mostly stronger on Friday with the AUD and NZD unable to enjoy the improvement in risk appetite evident in equity markets. The AUD fell 0.64% to 0.6411 on Friday, with the fall in commodities prices, particularly iron ore probably not helping. For the week the AUD edged up 0.5%. The kiwi loss 0.34% on Friday, but had decent gains on the week, up 1.01%. The AUD starts the new week at 0.64 while NZD is just below the 0.58 mark.

The other G10 underperformer (biggest on the day) on Friday was JPY, down 0.94%. The BoJ concluded its two-day meeting on Friday with Kuroda and Co. dismissing the prospect of any near-term exit from their ultra-easy monetary policy setting. Speaking at the press conference Governor Kuroda said that Board members would discuss an exit of easy policy if the 2% price target comes into sight, but then noted that the Bank’s median inflation forecasts for the 2023 and 2024 fiscal years were around the mid-1% range. So, it looks like we are going to have to wait for a long time. USD/JPY start the new week at ¥147.685.

GBP’s unwinding from an oversold position continued on Friday with the pair up 0.43% on the day and 2.76% on the week. The pound starts the new week at 1.1573, after trading to an overnight high of 1.1618 on Friday. The euro was the other outperformer on the week, up 1.04% to 0.9949.

As for commodities, iron ore was the standout underperformer over the past 5 days, down 11.5% to $78.4. Copper fell 2.17% on Friday to $3.466, down 1.26% on the week while Aluminium fell 3.32% on Friday but was unchanged on the week. WTI crude eased 0.79% to $87.90 and for the week it gained 3.35%. Gold fell 0.96% to $1,642 and for the week it eased 0.38%.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.