Total spending grew 0.9% in June.

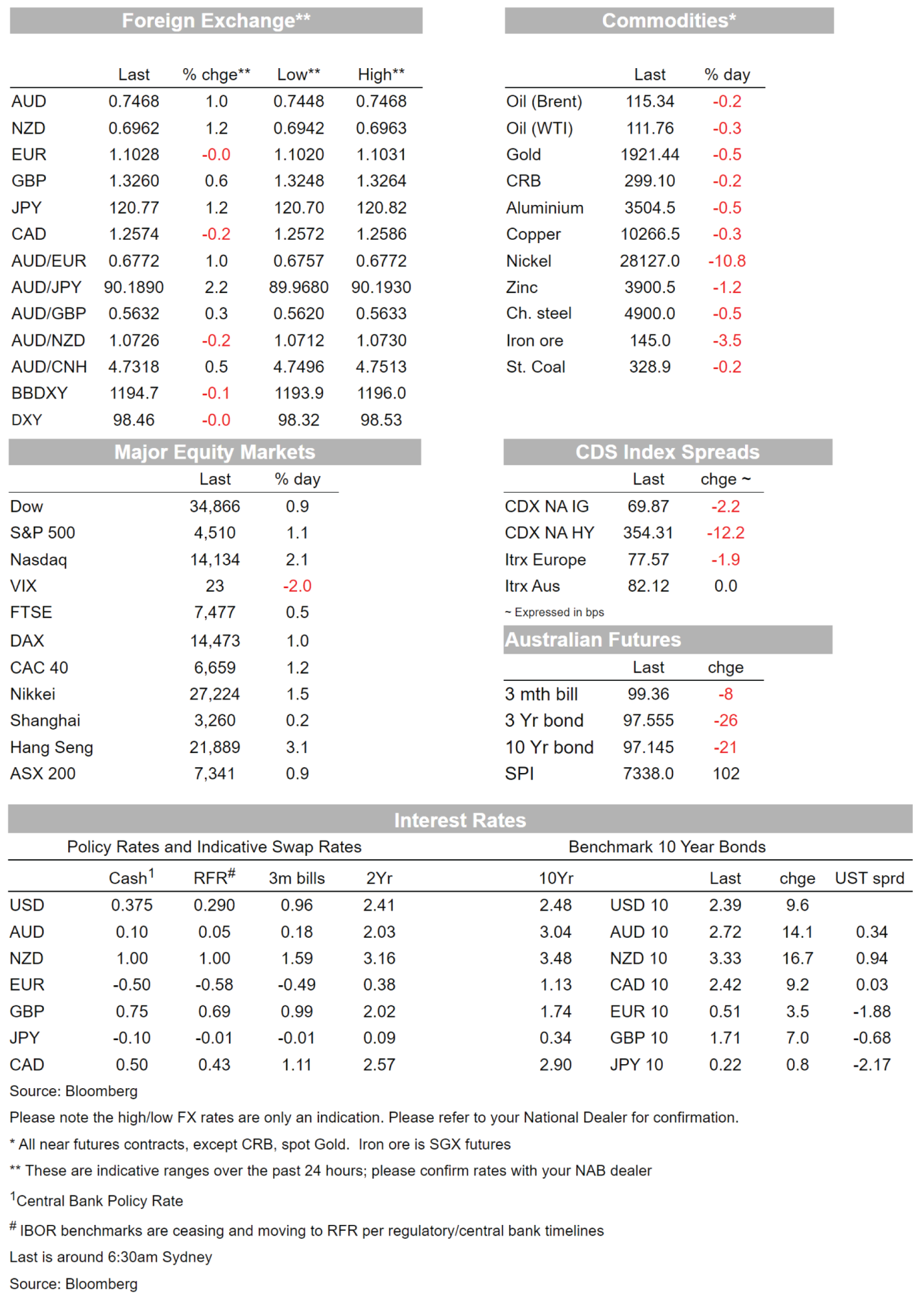

Yields continue to rise with US 10yr now +9.6bps to 2.39%.

https://soundcloud.com/user-291029717/markets-support-the-feds-balancing-act?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

Risk appetite remains resilient to the rise in bond yields (US 10yr +9.6bps to 2.39%) with the S&P500 up 1.1% overnight, while the US dollar has also edged lower (DXY -0.0%) and the global risk proxies of the NZD (+1.2%) and AUD (+1.0%) have outperformed. JPY (USD/JPY +1.2%) is the weakest out of G10 FX given the growing rate differential. US Fed pricing has lifted further with 7.6 rate hikes now priced at the next 6 meetings, meaning the market is pricing in a fair chance of two 50bp moves with the first in May and the second in June. That would take the Fed Funds rate to 2.25% by the end of the year, close to where most estimates of neutral are. Fed rhetoric remains hawkish after Powell on Monday with Bullard stating he wants to go to 3.00% by the end of the year to be mildly restrictive and drew parallels to the 1994 hiking cycle. Recession talk meanwhile continues with equity markets seemingly betting on a soft landing, while Eurodollars show rate cuts starting to be priced from mid-2023 (from Q3 2023 previously).

Global bond markets continue to sell-off with investors incorporating the hawkish pivot by central banks over recent weeks. Since the beginning of March the US 2yr yield has increased by 73bps to 2.16% and the US 10yr yield has increased by 55bps to 2.39%. At the same time the S&P500 has increased by 3.2%, suggesting risk appetite overall has remained resilient despite the hawkish pivot. As for moves overnight yields rose further again, though the 2s10s curve did steepen a little by 5bps to +21bps (2yr yield +5bps and 10yr yield +9.6bps). After Fed Chair Powell’s speech on Monday where he outlined the possibility of raising rates in 50bps clips, markets now price in 7.6 rate hikes for the next 6 meetings, meaning there is a fair chance of two of those meetings having a 50bp increase. The Fed’s May meeting now has 43bps priced, meaning around a 70% chance of a 50bps move. One US investment bank yesterday moved their call to 50bp increases in May and June, which broadly aligns with market pricing.

The Fed’s Bullard overnight added to those hawkish tones, emphasising the Fed needs to get to neutral (which Bullard pegs around 2%) and then go into restrictive territory. Bullard said he would “want to go to 300bps this year to be mildly restrictive” as well as reducing the balance sheet In terms of recession risk. Bullard said such a profile wouldn’t “break” the economy and he drew a parallel to the 1994 tightening cycle where the Fed was aggressive, but a soft landing was achieved. Chair Powell in his speech on Monday set up the soft landing narrative, stating: “ I believe that the historical record provides some grounds for optimism: Soft, or at least soft-ish, landings have been relatively common in U.S. monetary history.5 In three episodes—in 1965, 1984, and 1994—the Fed raised the federal funds rate significantly in response to perceived overheating without precipitating a recession”. Equity markets it seems is taking heed from the soft landing narrative.

Rates markets in contrast are pricing in the chance of rate cuts from mid-2023. In the words of former Treasury Secretary Summers, the “alleged soft landings in 1994, 1984, and 1965 were from nothing like current inflation and labor tightness. They were explicitly pre-emptive, something the current Fed explicitly rejects in its 2020 operating procedures”. Earlier this week Capital Economics’ Chief Economist published a note that looked at previous tightening cycles in the US, UK and Eurozone since the late 1970s. The conclusion was that of the 16 tightening cycles studied, 13 ended in recession. Soft landings are hard to achieve.

In FX, given the positive risk appetite backdrop, the NZD has been the best performing of the majors overnight, up 1.2% to 0.6962. The AUD is up 1.0% to 0.7468. GBP has also notably outperformed, up 0.7% to 1.3255, ahead of tonight’s Budget update and CPI release. At the other end of the leader board, JPY continues to struggle against the backdrop of higher global rates. USD/JPY surged above 120 for the first time since 2016, up over 1% to 120.75. Oil prices are slightly lower after yesterday’s 7% gain, with reports that EU members can’t agree on a Russian oil embargo, with Germany and Hungary holding out on such an agreement.

Finally in Australia, the AFR is reporting the government is considering cutting/freezing indexation for fuel excise. Phillip Coorey writes: “Next week’s federal budget will contain measures to deal directly with high petrol prices – either through a temporary reduction in the fuel excise or a freeze on its indexed increases. Prime Minister Scott Morrison all but confirmed on Tuesday that help was on the way regarding prices at the bowser, not just because of their direct impact on household budgets but also because of the flow-on costs to businesses” (see AFR: Budget will offer some form of petrol price relief, PM signals).

Coming Up

Very quiet with no top-tier data scheduled for Australia or the rest of Asia. In Europe, UK CPI data will front and centre after the dovish hike from the BoE last week, while the UK Budget Statement will also likely be looked at closely.

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.