Coming in for landing in a heavy cross wind

Insight

A couple of comments from the Fed chair during the post-FOMC meeting Statement have been responsible for most of the market price action, notably, Powell’s remarks “we’re some ways away from substantial progress on jobs” and that “the Fed is nowhere near considering raising rates”.

https://soundcloud.com/user-291029717/markets-turn-as-powell-reaffirms-some-way-to-go?in=user-291029717/sets/the-morning-callhttps://soundcloud.com/user-291029717/markets-turn-as-powell-reaffirms-some-way-to-go?in=user-291029717/sets/the-morning-call

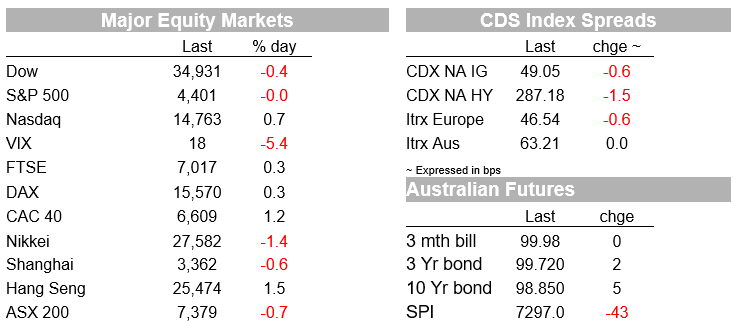

Following a small knee-jerk pop higher in US Treasury yields and the USD immediately following the FOMC statement where the Fed says that ‘progress’ has been made towards its goals, moves have since been reversed, and then some, during the post-FOMC Powell presser which includes a few dovish soundbites. A Similar ‘down then up’ reaction in US equities, but more up than down to see the S&P500 close flat on the day and the NASDAQ +0.7%.

A couple of comments from the Fed chair during the post-FOMC meeting Statement have been responsible for most of the market price action between the time of the Statement (4:00 AEST) and completion of the post-meeting press conference. Notably, Powell’s remarks “we’re some ways away from substantial progress on jobs” and that “the Fed is nowhere near considering raising rates”.

This was after the FOMC Statement re-iterated that the Fed would not downsize its $120bn per month increase in its holdings of Treasuries ($80bn) and agency mortgage‑backed securities ($40bn) until ‘substantial further progress’ has been made toward its maximum employment and price stability goals, but said “the economy has made progress toward these goals, and the Committee will continue to assess progress in coming meetings” (meetings plural).

With the next Fed meeting not until September (27/28), this would now seem to be the absolute earliest that ‘substantial progress’ might be deemed to have been made (i.e. not as soon as the August Kansas City Fed symposium in Jackson Hole) and possibly not before the December (16/17) meeting.

Fed aside, perhaps the most important story overnight is a Bloomberg report saying that ‘China’s securities regulator convened a virtual meeting with executives of major investment banks on Wednesday night, attempting to ease market fears about Beijing’s crackdown on the private education industry. The hastily arranged call, which included attendees from several major international banks, was led by China Securities Regulatory Commission Vice Chairman Fang Xinghai, people familiar with the matter said, asking not to be named discussing private information. Some bankers left with the message that the education policies were targeted and not intended to hurt companies in other industries, the people said’.

Taken at face value, the message is that profit has not become a dirty word in the Chinese system of ‘Socialism with Chinese characteristics’, only in certain sectors and where they are seen to conflict with key policy objectives linked to social justice and inequality, involving access to affordable education, housing and healthcare. How successful the messaging by the authorities will be in putting a floor under the broader Chinese stock market remains to be seen, but where the potential spill-over to Australia, if it does not, is significant, primarily via the observed link from Chinese equity market weakness to a weaker Chinese currency to a weaker AUD. So we are monitoring this very closely as a potential downside risk to our otherwise still constructive multi-month view of the Aussie.

Also to note in the last few hours is new that the group of 10 bipartisan Senators have reportedly reached agreement on the proposed near-$600bn infrastructure bill, expected to run for ten years and be self-funding over its life. A procedural vote is expected sometime during our morning, which if passed will likely lead to a full Senate vote over the weekend and where a 60-vote majority will be required for it to pass prior to be signed into law by President Biden. The bill primarily provides for spending on roads, bridges, waterways and broadband.

Economic data has been confined to a bigger than expected Advance US trade deficit in June ($91.2bn vs $88bn expected) which implies a bit of downside risk to tonight’s’ Q2 GDP numbers, and Canada’s June CPI where the average of its three core measures came in at 2.2% down from 2.3% in May and the 2.3% expected. Wednesday’s Australia’s CPI release was close to market expectations, with annual inflation surging 3.8% y/y although the core figure the RBA focuses on, the trimmed mean, was up just 1.6% y/y. There was no smoking gun in the release to change expectations on the RBA’s overtly dovish policy outlook.

So in US equities, the NASDAQ ended +0.7%, significantly outperforming the S&P500 (flat) and Dow Jones (-0.4%). S&P sector performance was unsurprisingly mixed, Communications Service and Energy – the latter thanks to a modest rise in oil prices – the biggest gainers, offset by losses mostly in Consumer Staples, Utilities and Real Estate. Facebook reported its Q2 earnings after the bell, where revenue of $29.08bn beat its street estimate of $27.86bn, but its stock is currently down 4% in after-hours trading, evidently on disappointment regarding its user numbers and warnings that it expected revenue growth to deteriorate significantly in both Q3 and Q4.

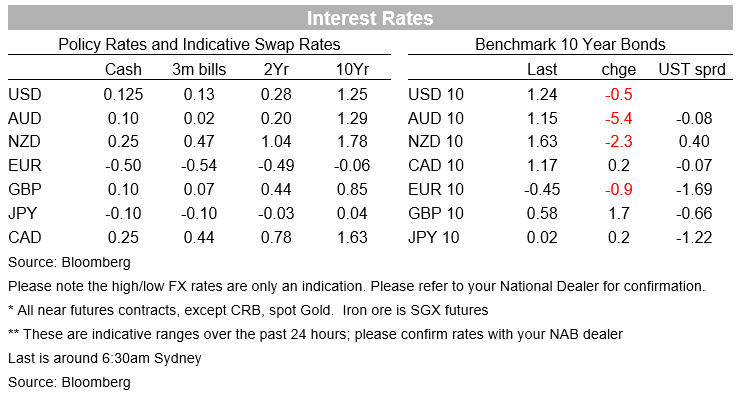

Bonds are finishing the New York day with 10-year Treasuries -0.8bps at 1.233% and 2s very marginally lower (-0.2bp at -.202%), consistent with the messaging from the post-FOMC messaging from Fed chair Powell. The day’s range of 1.225% to 1.27% on the 10-year has all been made since the FOMC Statement (first the highs then the lows).

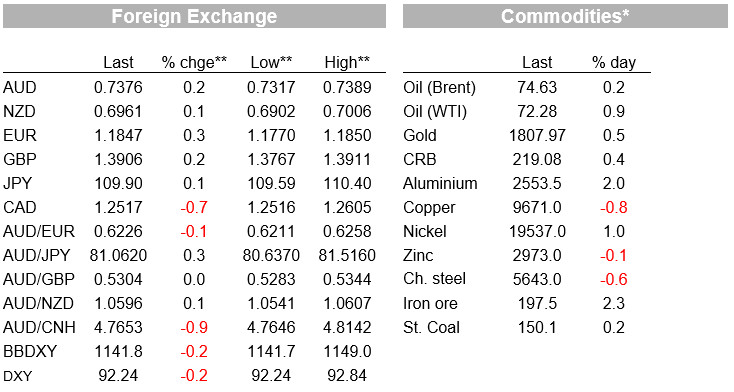

Finally in FX the small knee jerk positive USD reaction post the FOMC statement has been more than undone subsequently, the DXY index down just less than 0.2% and the broader BDXY just over 0.2%, again the dovish Powell messaging largely responsible. All G10 currencies bar NZD and JPY – both down 0.1% – are up against the USD, led by a 0.8% rise for the NOK and 0.6% for CAD. AUD is +0.2% to 0.7370, after having been as low as 0.7317 immediately after the Fed statement. The current 0.73-0.74 range looks set to prevail for a little longer.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Read our NAB Markets Research disclaimer

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.