Online retail sales growth slowed in May following a fairly strong April

Insight

Volatile overnight session sees risk on, risk off then risk on again

NZ: Food prices (y/y%), Sep: 8.3 vs. 8.3 prev.

US: CPI (m/m%), Sep: 0.4 vs. 0.2 exp.

US: CPI ex food, energy (m/m%), Sep: 0.6 vs. 0.4 exp.

US: CPI (y/y%), Sep: 8.2 vs. 8.1 exp.

US: CPI ex food, energy (y/y%), Sep: 6.6 vs. 6.5 exp.

US: Initial jobless claims (k), 8-Oct: 228 vs. 225 exp.

Markets have endured a volatile session overnight with an initial risk on move supported by media reports noting the UK Government was set to make a U turn on its tax cuts plan. Then, markets went risk off on a stronger than expected core US CPI print, to a 40 year high, driven by a nasty surprise in the services component. In the end the risk off move proved short lived with positioning, UK news and a sense that a stronger US inflation today still doesn’t negate expectations of a sharp declines ahead (wishful thinking?) all combined for a turnaround in sentiment with all main US equity indices ending the day with decent gains. The increase in Fed rate hike expectations triggered a flattening of the UST curve leaving 10y UST yields little changed at 3.95%, GBP has lead gains against the USD with AUD and NZD recovering after making fresh lows.

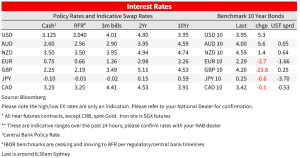

The overnight session began with a Europe enjoying a broad positive backdrop led by decent outperformance of UK Gilts, particularly the long end of the curve with the 30y initially declining by 25bps, extending the 2-day decline to 60bps from yesterday’s high of 5.14%. Media speculation of a UK government U turn on its fiscal plan has increased in recent days with overnight report noting the government was looking at several U turn options, but this time confirmed by government sources.

According to The Sun, government officials and the Treasury are working on several options which include scrapping Truss’ pledge to keep corporation tax unchanged next year, and instead raise it as planned by her predecessor Boris Johnson. This news and the BoE Gilt buying which has also ramped up in the past two days (£4.7bn of gilts, including of £3.1bn of index-linked bonds in the past two days) clearly appeased markets. In addition to the decline in longer dated UK Gilt yields (30y closing 26bps lower to 4.53%), the market has also trimmed BoE rate hike expectations, presumably on the basis that less government expenditure means less inflationary pressures next year. The peak in the BoE cash rate next year is now seen around 5.55%, down from 6.27% late in September.

The US CPI print was billed as the glamour stat to watch this week and from that perspective its release certainly didn’t disappoint, however those hoping for an ease in US core inflationary pressures where severely disappointed. Both headline and Core CPI readings surprised to the upside with both yoy and mom readings printing stronger, the headline print came at

8.2%yoy vs 8.1% expected while the more important Core reading printed at 6.6% vs expectations for 6.5%. The core CPI print was the highest in 40 years with the monthly reading lifting to .6% m/m (0.4% expected) implying no ease in inflationary pressures yet, with five of the past six months coming in at that rate or higher.

Looking at the details, core price pressures centred squarely on the service sector with core goods prices unchanged. In the services sector, most of the damage is in rents, which rose 0.8%, stepping up after a run of increases of 0.6-to-0.7%. Here is where the debate on the outlook for core US inflation is likely to focus over coming months, the housing market is already in recession suggesting inflationary pressures on rent should also ease, but the way this is measured in the US has a lag effect which depending on who you read it could be a couple of months and or potentially more than a year. So, while there is evidence of an ease in new rentals, rent renewals is what matters for the CPI and arguably there is still a fair bit that needs to work its way through.

Also release overnight and an important reading for the Fed, the Cleveland Fed’s alternative measures of underlying inflation suggest the same persistent inflation message as the core CPI. The Median CPI +0.7%/7.0% after 0.7%/6.7%, the trimmed mean 0.6%/7.3% after 0.6%7.2%. From the Fed perspective, all these inflation numbers suggest a 75bps hike in November looks like a done deal while another 75bps hike in December is also looking increasingly likely. Looking at Fed Fund futures, the market is considering the option of a 100bps hike in November with 0.794bps priced while 63bps are expected in December. The terminal rate in the cycle has also edged higher with a peak now seen at 4.92% early in May next year.

The increased in Fed rate hike expectations triggered a flattening of the UST curve with the 2y note ending the day 12bps higher to 4.409%. The 10y rate traded to an overnight high of 4.075% in the aftermath of the CPI release, but then it gave most of it back, ending the session at 3.95%, 1bps higher over the past 24 hours. As noted above the big move in core global bond yields have come from the UK, with longer dated Gilts leading the decline in yields, 10y Gilts closed at a 4.198%, 24bps lower on the day.

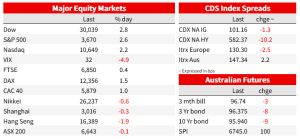

The equity and FX markets were not immune to the volatility seen in the rate world, indeed some of the equity and FX moves were probably more volatile. Starting with US equities first, after opening sharply lower it was onwards and upwards, the S&P 500 gapped 2.38% at the open and then closed 2.64% higher, that is over a 5% range on the day. The NASDAQ ended the day +2.23 and the Dow was 2.83%. In recent times good economic news have been treated as bad news by the equity market given implications for more Fed hikes, overnight however the stronger than expected CPI did trigger an increase in Fed hike expectations, but this time equity investors seemingly decided that a stronger US inflation today still doesn’t negate expectations of a sharp declines in prices ahead. That might be true, but there is still a great deal of uncertainty of how quickly this decline will unfold and for the Fed this decline needs to be significant, a fall from 6 to 4%, won’t be enough, the Fed wants assurances that cope CPI will head down to 2% and we are still a long way from that goal.

An alternative explanation for the strong recovery in US equities has been a mass of a wave of short covering with a test of some technical levels also favouring move, with Bloomberg suggesting at one point, the benchmark S&P 500 had given back 50% of its post-pandemic rally, triggering programmed buying. Either way, if the cause for the rally was one of both of these drivers, then it hard to suggest we are at the start of a new uptrend. Instead, an aggressive Fed and concern over inflation are likely to keep markets volatile.

The USD jumped on the CPI release with the DXY index trading to an overnight high of 1.1388 before falling to 112.47, down 0.75% on the day. GBP led the gains against the USD within G10, up just over 2% to 1.1325 reflecting just how much bad news has been in its pricing while there is a lot of uncertainty ahead, in addition to the UK Fiscal plan, will the BoE deliver on the +200bps priced over the next two meetings?

The AUD and NZD have remained at the mercy of risk appetite, trading to fresh new lows as equity markets collapse and then jumping as they recover. The AUD fell to 0.6170 and has recovered to start the new day at 0.6296 while the NZD fell to a fresh low of 0.5512 following the US CPI report but has recovered some 2½% from that nadir to trade as high as 0.5642.

USD/JPY traded to a high of 147.67, 1pip above the 1998 high and now trades at 147.2475 with speculation of another round of intervention increasing, although our sense is that intervention from here will be about the speed of depreciation rather than a specific level

NAB Markets Research Disclaimer

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.