Coming in for landing in a heavy cross wind

Insight

FOMC Statement hints at reduced pace of tightening ahead…

The FOMC statement hinting at possibly smaller incremental rate hikes ahead produced the requisite knee-jerk boost for US equities, lower bond yields and a weaker USD, before moves in rates and FX markets were more than fully reversed during and after the ensuing press conference from Fed chair Powell. He noted that the ultimate level of (policy) rates is seen to be higher than previously expected and that it is ‘very premature’ to think about pausing rate hikes.

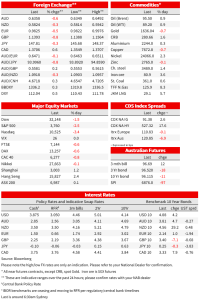

USD FX indices have flipped a near-1% fall post the FOMC statement into modest gains on the day, US treasury yields are higher across the curve in a ‘bear flattening’ move, 2s having earlier been more than 10bps lower. US equities were initially holding on to a good chunk of their post Fed Statement gains but have cratered in the last ‘hour of Power’ NYSE trade. AUD/USD is now back from its post Statement high of almost 0.65 to be struggling below 0.64 (~0.6360).

The market-moving sentence in the FOMC Statement now just over two hours old reads, “In determining the pace of future increases in the target range, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments”.

This gave immediate succour to the views expressed by San Francisco Fed President Mary Daly and ‘Powell doppelganger’ Nick Timiraos from the Wall Street journal, both on October 21, that a step down to no more than 50bps incremental Fed tightening could come as early as the December (13-14) FOMC meeting.

The market’s second take on the Fed during the ensuing Press conference from Fed chair Jay Powell was on comments (paraphrased here) such as ‘ultimate rate level higher than previously expected’, that the time ot slow rate hikes may come in December but that a ‘decision has not been made on that’, that the Fed is looking for positive real rates across the curve and that it is ‘very premature’ to think about pausing rate hikes. ‘We have a ways to go, ground to cover’, Powell adds.

In FX, the BBDXY index was flat to Tuesday’s New Yor close half an hour into Powell’s press having been almost 1% lower following the release of the FOMC Statement. It is currently up 0.3% (and the narrower DXY closer to 0.5%) within which AUD/USD is currently around 0.6360 having been as high as 0.6492. Only the JPY (currently 0.3%) is showing any gains relative to Tuesday’s New York closing levels, and which followed various MoF/BoJ comments during our day yesterday where one that caught our eyes was reference by MoF chief Suzuki to both levesl as well as volatility being relevant (vis-a vis the ongoing FX intervention risk).

For the time being at least, therefore. More ‘sideways chop’ for the US dollar looks at least as a good (better?) bet than a quick fall-back though the recent (27 October) lows. The latter, dare we say it, still looks to be very much ‘data dependent’ (and requiring clearer sight of the Fed’s ‘terminal rate’).

In the rates market, prior to the Fed (i.e., at Tuesday’s NY close) the money market priced the terminal Fed Funds rate at 5.05%, in May next year. Currently it’s 5.075%, also for May 2023. So not a lot of net movement, though remember 5%+ was already above) the 4.625% (4.50-4.75% target range) median ‘dot’ in the September Summary of Economic projections (SEP). Compared to the now 3.75-4.0% Fed Fund Target and judging from the sentiments expressed by Mr Powell just now, one could be forgiven for thinking the risks around current Fed pricing in 2023 currently lie to the upside.

In bonds, the ‘change on the day’ for Treasuries are currently +5bps for the two-year and 4bps for 10s, moves which compare to a very mixed performance by European bonds earlier in the night, where 10-year gilts ended 17bps low in front of the Bank of England tonight – moves which followed a successful £750bn ‘QT’ sale of bonds by the BoE on Monday afternoon – while Bunds finished some 6.6bp higher.

Bond yields have finished off their highs following what has been a very negative last ‘hour of power’ in US stock market, with the NASDAQ finishing off 3.54% and the S&P 500 by 2.5%. The S&Ps double digit October rally off its early-month lows is suddenly staring to look like a distant memory.

Earlier in the day Wednesday, the recently revamped US ADP private payrolls report showed a gain of 239k in October, above the 185 concensus, driven by strong job gains in the leisure/hospitality sector. This followed the previous day’s strong (i.e., rebounding) JOLTS labour market report. Outside of various hiring freezes in the tech.sector, all indications are that that the US labour market remains too hot for comfort for the Fed. Friday’s key non-farm payrolls report is expected to show slowing employment growth and maybe a 1/10% upticks in the unemployment rate, but still a robust 200k jobs added for the month.

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.