Online retail sales growth slowed in May following a fairly strong April

Insight

US equites fall on Friday to close out a 3rd consecutive negative quarter

Data round up:

NZ: ANZ consumer confidence, Sep: 85.4 vs. 85.4 prev.

NZ: Building permits (m/m%), Aug: -1.6 vs. 4.9 prev.

CH: Manufacturing PMI, Sep: 50.1 vs. 49.7 exp.

CH: Non-manufacturing PMI, Sep: 50.6 vs. 52.4 exp.

CH: Caixin Manufacturing PMI, Sep: 48.1 vs. 49.5 exp.

EU: CPI (m/m%), Sep: 1.2 vs. 0.9 exp.

EU: CPI (y/y%), Sep: 10 vs. 9.7 exp.

EU: Core CPI (y/y%), Sep: 4.8 vs. 4.7 exp.

US: Personal income (m/m%), Aug: 0.2 vs. 0.3 exp.

US: Personal spending (m/m%), Aug: 0.4 vs. 0.2 exp.

US: Core PCE deflator (y/y%), Aug: 4.9 vs. 4.7 exp.

US: Chicago PMI, Sep: 45.7 vs. 51.8 exp.

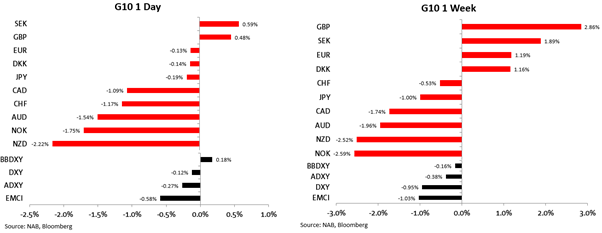

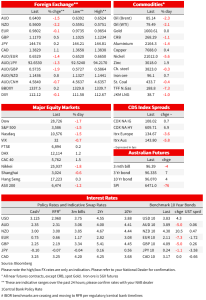

US equities fell to fresh yearly lows on Friday to close out a third consecutive quarter of declines. The S&P500 lost 1.5%. In currency markets, commodity currencies fell sharply, the AUD down 1.5% to 0.6400 and the NZD was 2.2% lower. In contrast, the pound recovered further on Friday to be within around 0.5% of its level prior to last week’s mini-budget. Over the week, US yields were higher and steeper.

Data flow on Friday showed no letup in inflation. Eurozone inflation rose 10.0% y/y in September vs 9.7% expected, while US August PCE data showed real consumption holding on to positive growth, with the PCE deflator rose faster-than-forecast (more below). The inflationary backdrop yet to provide any relief for central banks. Fed Vice Chair Brainard said on Friday that “we are committed to avoiding pulling back prematurely.”

The dollar was softer over the week on the DXY, down 0.9% as a recovery in the pound and heavily weighted euro more than offset declines in commodity-sensitive currencies. The AUD fell 1.5% on Friday to end the week 2% lower at 0.6400, back towards its low for the week at 0.6363 on Wednesday before a reversal in the dollar appreciation following the BoE’s intervention in gilts saw the Aussie claw back above 65c to 0.6542. the NZD was a clear underperformer on Friday, down 2.2% to be 2.5% lower over the week.

The GBP was 2.9% higher over the week to be back within around 0.5% of its level before the mini-budget against both the dollar and the euro. Unlikely to help the pounds fortunes heading into the new week is news after market close on Friday, S&P lowers its outlook for UK sovereign debt to negative from stable, saying tax-cutting measures “could weaken the U.K.’s fiscal position. ” The shift in outlook means the credit rating may change within 6-24 months but doesn’t indicate an imminent shift and doesn’t always indicate a change will occur. Reports suggest Chancellor Kwarteng has no plans to accelerate the new medium-term fiscal statement on Nov. 23, alongside a full forecast from the Office for Budget Responsibility.

In terms of Friday’s data flow, in Europe preliminary CPI data for September came in hot at 10.0% y/y from 9.1% in August and 9.7% expected. That’s the first double digit read in the blocs history and follows an upside surprise to German price data earlier in the week. The result was once again driven by energy and food prices, though the core measure also came on hot at 4.8% y/y vs 4.7% expected. Meanwhile, the unemployment rate held steady at 6.6%. On Friday, the ECB’s Schnabel said that “ a decline in real wages and a slowdown in aggregate demand may not materially ease current inflationary pressures,” adding that “further increases in our key policy rates will be needed.” On the other side, Italy’s Visco commented that “excessively rapid and pronounced rate hikes would end up increasing the risk of a recession.” Markets remain tilted towards a follow up 75bp hike at the 27 October meeting, with 70bp priced.

US PCE showed real consumption growth was in line with expectations, and remained positive, if only just. The very gradual normalisation of the mix between goods and services continued, real goods consumption was 0.2% lower, while services was a quarter percent higher. But the PCE deflator came in on the high side of expectations even after the hot August CPI print had forecasters braced for a bigger number . Core PCE was 0.6% vs 0.5% expected and 4.9% y/y. Headline came in at 0.3% vs 0.1% expected and 6.2% y/y. More concerningly, alternative measures of core inflation see underlying inflation running hotter. Median PCE inflation was 0.7% m/m and hit a new record 5.8% in y/y terms. There are growing signs of easing goods inflation pressures but slowing earnings growth will be key to giving the Fed confidence inflation will fall back to target. The next test comes in payrolls on Friday which is expected to show still robust employment growth of 250k, and hourly earnings growth of 0.3% m/m. An upside surprise on earnings you’d think would all but nail on 75bp in November. Markets currently price 68bps.

Out earlier Friday was China PMIs . The Official non-manufacturing PMI rose to 50.1 from 49.4 (consensus 49.7), the non-manufacturing fell to 50.6 from 52.6 (consensus 52.4), and the Caixin manufacturing fell to 48.1 from 49.5 (consensus 49.5). Despite the tick higher in the official manufacturing PMI, on net a weak read that signals China’s ongoing COVID restrictions are weighing on activity. Weaker external demand is also part of the story. New export orders in the Caixin survey plunged to 45.5 in September, from 48.5 in August.

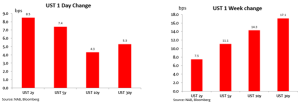

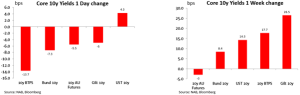

The European bond market brushed off the inflation surprise on Friday, with the German 10-year rate falling 7bps. But rates were higher in the US, by 9bps on the 2-year rate and 4bps on the 10-year. Over the week, the sharp moves in gilts that began last Friday as markets reacted to the UK Government’s fiscal plan continued in the past week. UK 10yr yields are 27bp higher over the week and 61bp higher than they were ahead of the mini-budget last Friday , closing at 4.08% on Friday. That’s after touching 4.59% on Wednesday before the BoE stepped in to short-circuit a feedback-loop enveloping longer dated gilts. Curves in the US were higher and steeper than a week ago. The 10-yield hit 4% on Wednesday ahead of the BoE intervention in gilt markets but is now sitting around 3.83% and 14bp higher over the week. While UK developments were at the forefront of global yield movements over the week, the move higher in in yields also comes in the wake of hawkish upgrades to the Fed dots at the prior weeks Fed meeting, and alongside a slew of Fed speakers talking higher-for-longer policy.

On that note, Vice Chair Brainard on Friday, while noting that it will take time for tighter financial conditions to bring inflation down, said that “Monetary policy will need to be restrictive for some time to have confidence that inflation is moving back to target. For these reasons, we are committed to avoiding pulling back prematurely. ” Though in some small contrast to some of her most hawkish colleagues, she did acknowledge that monetary policy affects inflation with a lag, and that at some point, the risk would become two sided.

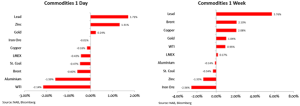

Finally, commodities markets were mixed. Some reprieve in the strength of the dollar and the possibility the OPEC will agree to a cut to crude output on Wednesday helped oil higher over the weak. Brent was 2.1% higher and WTI was 1% higher. That follows 5 consecutive weekly declines. Iron ore prices were weaker, down 2.6%.

Today

This Week

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.