Price growth edges lower despite reasonable economy

Insight

The RBA didn’t steer from its earlier stance that it was too soon to be looking at any changes in policy right now.

https://soundcloud.com/user-291029717/no-surprises-from-the-rba-and-dont-be-surprised-by-an-uptick-in-aussie-gdp-today?in=user-291029717/sets/the-morning-call

Sorry’s just not good enough for you – McFly

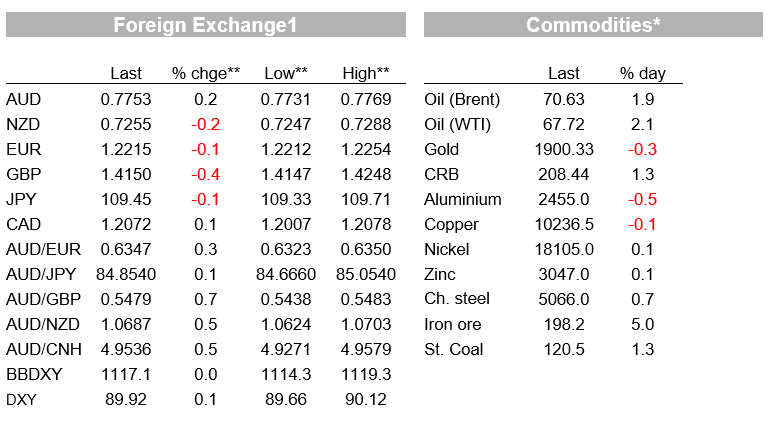

After a solid start led by a rise in energy prices, US equities have ended the day flat while European equites closed higher. Solid manufacturing activity readings supported European markets, but in the US, ahead of payrolls on Friday, the ISM manufacturing index beat expectations, the softer employment component print sour the mood. USD and UST yields are little changed, but AUD is tad stronger ahead of today’s Q1 GDP print.

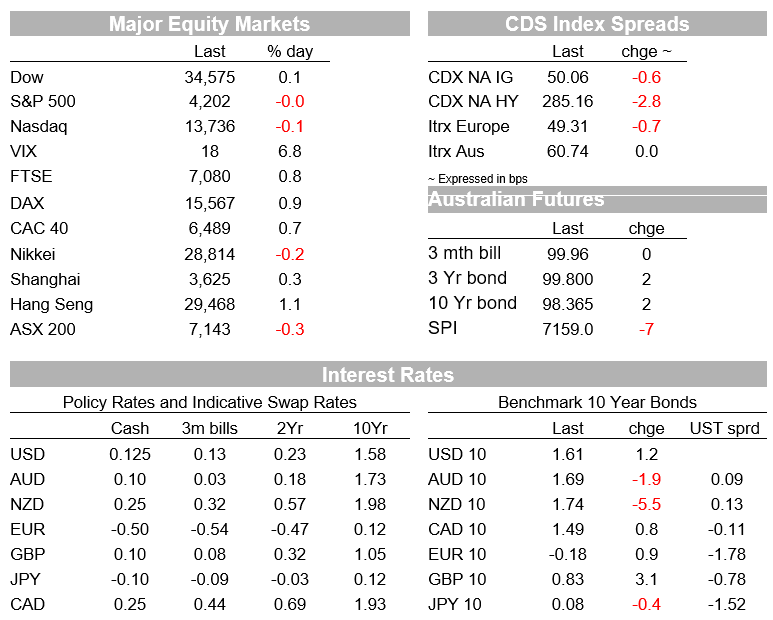

The S&P 500 has ended the day down 0.05% with the NASDAQ -0.09%. Looking at the S&P 500 sector performance the energy sector was the big winner, up 3.93% while Health Care (-1.64%) and Utilities (-0.62%) were the laggards. Gains in energy stocks were supported by a solid rise in oil prices with WTI + 2.47% and Brent +1.72%.

The move up in oil was buoyed by supply uncertainty coming from OPEC+ while the International Energy Agency warned of a looming gap between rising demand and stagnant supply in the second half of the year, putting upward pressure on prices. OPEC+ agreed to stick to the plan to hike output in July, but the market was left guessing about what will happen after July, with the Saudi Arabia keeping its options open about whether to raise supply further as demand recovers. Playing to the upbeat outlook, Saudi Energy Minister Prince Abdulaziz bin Salman said “The demand picture has shown clear signs of improvement,” , but then when pressed on whether more supply increases will be needed, he said: “I will believe it when I see it.”

Overnight we also had solid European and US manufacturing activity readings favouring the notion that the global economic recovery is on a strong path supported by solid demand but with ongoing supply-chain/logistics bottlenecks and upstream inflation high as a result. One notable difference is the bigger labour supply shortages in the US.

The US ISM Manufacturing index rose marginally to 61.2 from 60.7, marginally above the 61-reading expected by consensus. Demand continues to put pressure on supply that is still struggling to catch up with staffing challenges preventing factories from ramping up production. The key employment gauge notably fell to a six-month low of 50.9, reflecting the difficulty in hiring and retaining labour , with the spokesman for the survey pointing to the enhanced unemployment benefits reducing labour supply and once they expire the labour market will be much more in sync with demand and supply. Worth noting here that 24 US states are planning to stop the $300 supplement employment benefit by the end of June with many also offering one-time bonuses for returning to work. So, there is a reasonable case supporting an ease in US Labour shortage over coming months.

Earlier in the session, final readings for the Markit manufacturing PMIs across the Euro area were revised slightly higher from the flash estimates, with the aggregate up to a record high of 63.1, consistent with a strong recovery for the region . The common theme was output and inventories held back by capacity constraints and as deliveries from suppliers “deteriorated at a severe and unprecedented rate”, leading to a substantial rise in average input costs, “with the rate of inflation hitting an unprecedented level”.

European equities closed higher across the board with the Stoxx 600 index up 0.75%, after surging as much as 1.3% earlier in the session. Like in the US, the energy sector outperformed (2.2%) with materials also doing well (2.9%). Health care (-0.1%) was the only sector in the red, while telecom (+0.1%) and food, beverage and tobacco (+0.1%) lagged the index’s gains.

In Fed-speak, Governor Quarles, who was quoted last week as suggesting that it might be apt to discuss plans to taper bond purchases over the coming months in a highly qualified statement, was on the wires again overnight. He noted some benefit in reducing the Fed balance sheet “in the future” But he also noted that there was a significant way to go to full employment and that monetary policy tools shouldn’t be used to address supply chain disruptions, adding the “question is whether they last long enough to affect inflation expectations”. Governor Brainard noted the Fed was still “far from our goals” with risks on both sides and called for the Fed to be “steady and transparent” in its policy approach “while remaining attentive to the evolution of the data and prepared to adjust as needed”.

In other economic releases, Euro area annual CPI inflation hit 2% for the first time since 2018 but the core increase was much lower at 0.9%, as expected. Canada GDP in Q1 was weaker than expected but was still up a strong annualised 5.6%, fuelled by a record contribution from residential investment.

UST yields are little changed with the 10y note at 1.6062% and the USD is also little moved in index terms. Both BBDXY and DXY are trading close to their year to date lows, but not quite yet looking to break lower. DXY now trades at 89.92 while BBDXY is at 1117.

The USD has had a mixed performance vs G10. The AUD is one of the top performers in the past 24 hours, up 0.3% to 0.7755, so still comfortable within the 0.77-0.78 range that has mostly contained the pair since the start of March. Yesterday AU Q1 GDP partials pointed to the potential for a strong Q1 GDP print today (see more below) and the RBA policy meeting came and went with little fresh insight about its intentions on policy decisions that will come in the July meeting. Edits to the statement were mostly in a positive direction. Our economists continue to believe that the 3-year yield curve control will not be extended from the April 2024 bond to the November 2024 bond and QE will probably be extended, but at a slower pace later in the year.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.