Total spending grew 0.9% in June.

Equities made an unconvincing “buy the dip” bounce as yields consolidated their recent moves.

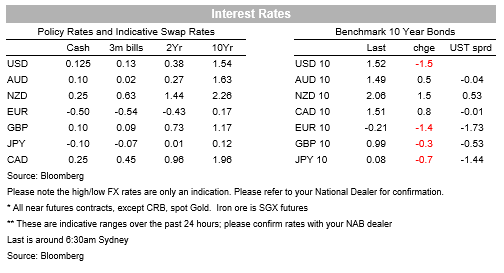

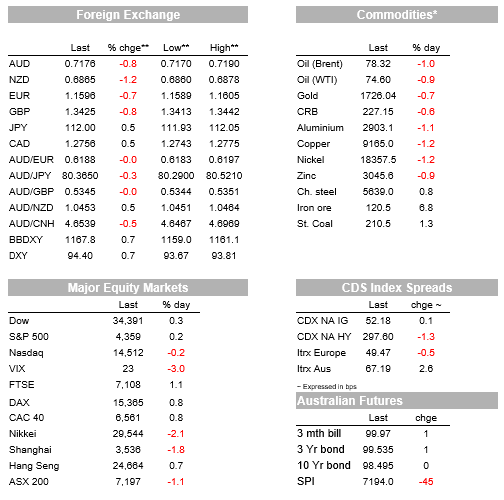

Equities made an unconvincing “buy the dip” bounce as yields consolidated their recent moves. The S&P500 closed up 0.2% with tech stocks notably trailing the rebound (NASDAQ -0.2%). Yields have taken a breather, with the US 10yr consolidating around 1.50-1.55% (overnight -1.5bps to 1.52%). The USD tells the better story with the broad BBDXY +0.7% and now at its highest levels since November 2020. Since last week’s FOMC meeting the USD has risen by an impressive 1.3%, meaning many key support levels are breaking for major pairs. The Yen slipped to its lowest level since February 2020 (USD/Yen +0.5% to 111.99), GBP lowest since December 2020 (GBP -0.8% to 1.3425) and EUR lowest since July 2020 (EUR -0.7% to 1.1596). The ECB’s Sintra conference overnight emphasised the divergence between the Fed and the BoE which is contemplating hikes in 2022, against the ECB and BoJ which remain more dovish. The AUD (‑0.8%) and NZD (-1.2%) while weaker overnight have not broken new ground given their sell-offs in August. The AUD/NZD cross though has lifted with virus cases in NZ casting doubt on an easing of lockdown restrictions.

As for whether the US can avoid a government shutdown, no progress was made overnight. Focus today will be on Congress passing a continuing resolution before the end of Thursday to fund the government thru to December 3 – both sides think this will pass. The debate around the infrastructure bills continues (the $1 trillion bi-partisan, and the $3.5 trillion social infrastructure) as is the debt ceiling debate. The debt ceiling itself is not as pressing given Treasury Secretary Yellen’s date of October 18 of when the US would run out of room if the debt ceiling is not raised. Democrats so far have resisted going it alone and using reconciliation to raise the debt ceiling given Republican opposition, though that could be tested if Republicans continue to blankly oppose raising the ceiling. (see WSJ: Democrats Aim to Keep Government Funded as Talks Continue on $3.5 Trillion Bill and Politico: Congress primed to avert shutdown despite remaining conflicts).

There was little market reaction to Fed speak overnight. The Fed’s Harker added to the view of the US hiking rates in 2022 or early 2023, noting “after we taper our asset purchases, we can begin to think about raisin g the federal funds rate…But I wouldn’t expect any hikes to interest rates until late next year or early 2023.” The Fed’s Daly in contrast was more dovish saying she didn’t see a case for a 2022 rate hike (“If we should get there [to maximum employment] in the time frame of next year that would be a tremendous win for the economy,“, but “I don’t expect that to be the case.”). There was also little reaction to economic data which was sparse . US pending home sales unexpectedly rose by 8.1% against 1.4% expected and is now at a seven-month high. Meanwhile across the pond the euro area’s economic confidence series, a mix of business and consumer confidence, nudged higher to remain close to historical highs. This is of some relief considering the backdrop of surging energy prices.

It appears while central banks are still buying the transitory narrative, the transitory impact is expected to be longer than expected with the Fed and the BoE, relatively speaking, the most willing to raise rates. At the ECB’s Sintra Conference, central bank heads were asked about their biggest worries – for Fed Chair Powell it was the tension between faster inflation and slack in parts of the labour market, while for BoJ’s Kuroda it was the economic recovery and for the ECB’s Lagarde the massive unvaccinated population. The difference in worries is thus pretty clear in terms of the potential for policy to respond to inflation in 2022. Although not elaborated on, the notion of transitory inflation remaining high for longer was noted by Powell who said it was “ frustrating to see the bottlenecks and supply chain problems not getting better, in fact at the margins apparently getting a little bit worse. We see that continuing into next year probably, and holding up inflation longer than we had thought.”.

Developments in China remain a concern for the global growth picture. Widespread power cuts in China have prompted the government to consider raising power prices, which are currently heavily regulated. Some of reason for the power cuts is that the regulated prices are too low relative to the increased cost of generation. Higher prices would incentivise more generation and less consumption. There is also the potential for Evergrande to weigh on the wider construction sector, while delta outbreaks amid China’s zero-COVID policy is also providing to be problematic. We get an update on how activity is faring against these developments in today’s PMIs.

Finally in Australia, The Council of Financial Regulators (the RBA, APRA, ASIC, and Treasury) have formally discussed a potential tightening in macro-prudential policy with APRA set to unveil an “information paper on its framework for implementing macroprudential policy” in the next couple of months. APRA will consult with the Council on the implementation of particular measures. The main concern of the Council does not stem from any deterioration in lending standards – which “remain sound ” – but rather the medium-term risks to the economy should credit growth continue to materially outpace growth in household income (i.e. debt to income ratios rising materially). The RBA has consistently ruled out the option of using interest rates to tackle house prices or other housing market developments. Debt to income ratios appear to be the tool regulators are contemplating using.

A busy day domestically with Building Approvals, Credit and Job Vacancies. Offshore most focus will be on the China PMIs to see what impact recent events are having on activity, while in the US focus will remain on Congress and whether they can pass a standalone funding measure and thereby avoid a temporary shutdown after Thursday. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.