Total spending grew 0.9% in June.

The US dollar continued to rise yesterday, after the hawkish comments from the Fed.

https://soundcloud.com/user-291029717/nz-gdp-aussie-employment-both-punch-the-lights-out-but-currencies-fall?in=user-291029717/sets/the-morning-call

Composed shortly before his untimely demise, Bowie here comments on his self-imposed exile from Britain in favour of New York, dismissing any regrets about being away from his home country for so long. I empathise. I do miss Bowie though, much as I know some readers do George Michael (morning Lucia) and too Prince of course, all of whom tragically passed in 2016.

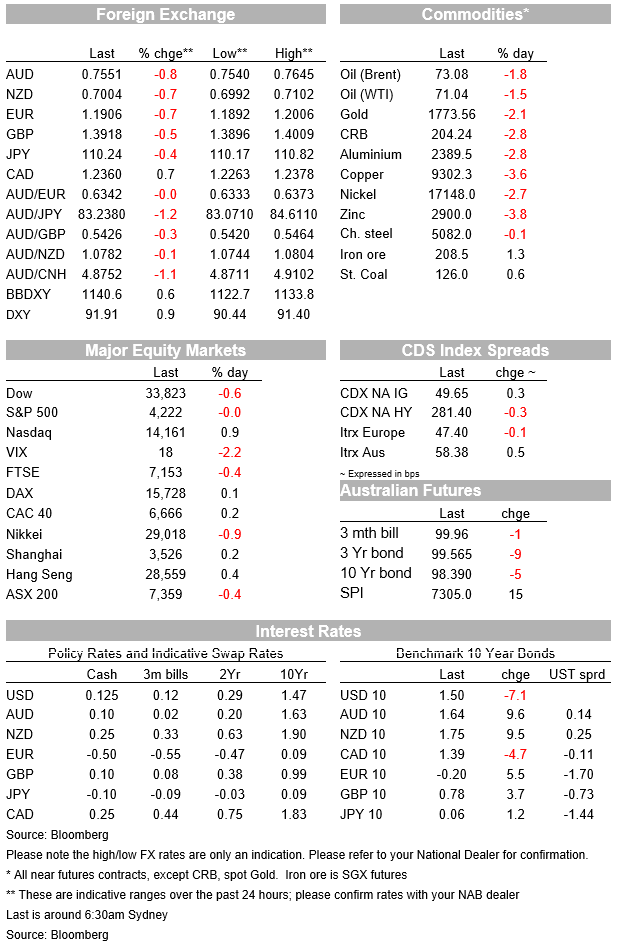

All of which has little to do with markets save for the title, and where we come in to find that the big dollar has added the same again (0.9%) to Wednesday’s post-Fed gains, in doing so pulling AUD/USD to within a whisker of its 2021 year-to-date lows (latter 0.7532 back on April Fool’s day). US bond markets have seen a decent reversal of Wednesdays yields back-up but only at the longer end of the curve, meaning the post-Fed curve flattening themes has extended (2-year Treasuries +0.4bps, 5s -1.5bps, 10s -7bps and the 30-year -11.5bps). US equities have recovered from their APAC futures market weakness to see the NASDAQ ending the NY days up 0.9% and the S&P about flat. Sector rotation is the big theme here.

The overarching theme of market price action since yesterday’s Fed meeting, where the standout feature was the imposition of two 2023 FOMC rate hikes in the Fed’s new ‘dot plot’ where previously there was none, was a rapid retreat from the global reflation trade. I always thought (still do) of this more about a vigorous recovery in the real global economy post the pandemic than necessarily a resurgence of inflation. This theme (strong global upswing) is very far from dead in our view, yet one of the most notable features of post-Fed market price action has been the sharp pull-back in (US) market-implied inflation expectations (‘break-evens’). At 10-years they have fallen back from 2.42% to 2.21% and an early-May peak of 2.60%. All because in the latest dot plot, the median FOMC member thinks conditions might warrant 50bps of rate hikes in 2023, following which Fed chair Powell told the press than the ‘dots’ are an unreliable guide to future Fed policy actions and that ‘rate increases are really not at all the focus of the committee’? Really?

It may be that the Fed was just being really, really smart on Wednesday, following what former Bank of England chief Mervyn King dubbed the (Diego) Maradona playbook for monetary policy, whereby central bankers (Maradona) sends markets (defenders) scurrying in all directions with their commentary (shimmying and head fakes) and then simply stroll down the middle of the park and pop the ball in the net, not having had to take any hard policy action. Mind you, King’s an Aston Villa supporter, so take him with a grain of salt.

The post-Fed market positioning shake-out has been most evident in the commodities market, with Bloomberg’s commodity index down a chunky 3.5%, including a 3.5% fall in copper prices, 2.8% for aluminium and 3.8% for zinc, and gold down 2% (having been more than 4% lower at one stage). Iron ore futures are up though, albeit by just 1.2%. Moves lower in some of these market – base metals in particular and earlier iron ore – were well already underway in prior days, commodity market longs having been rattled by China’s increasingly shrill verbal attacks on ‘speculators’, instructions to state owned firm to curb their dealing with offshore commodity suppliers, the announcement of a staggered release of copper, aluminium and nickel reserves, and then Wednesday’s weaker than expect set of May China activity readings.

So there can be no doubt that the froth has well and truly been blown off many commodity market, yet if the global (growth) reflation trade is still very much intact, it is hard to envisage that commodity prices overall are not going to remain strong as we go through the second half of 2021 and into 2022. Remember too, China will need a lot of commodities to services this demand from the rest of the world.

As such, we maintain a constructive view of the AUD for the second half of this year, while acknowledging the parlous near term technical picture or the currency. In the absence of a big bounce back today, the catalyst for which is hard to see after yesterday’s rally off the much stronger than expected local employment data proved fleeing, the weekly closes are going to be regarded ominously by the charting brigade. As for the big USD, the Bloomberg BBDXY index has now undergone an almost exact 61.8% (Fibonacci) retracement of the April-May decline. If that can hold, there is hope for an early resumption of the USD downtrend.

In overnight economic news US jobless claims unexpectedly rose last week for the first time since April, at 412k versus 360k. It would be too early to jump to the conclusion that the downward trend has been broken, and the figure might just represent noise. The Philly Fed manufacturing index was in line, suggesting robust activity levels while the mix showed a notable fall in new orders and a rise in employment. The prices paid index rose to a fresh multi-decade high of 80.7.

Finally, The big theme in US equities has been sector rotation back out of the value/cyclicals into growth, the latter dominated by ‘big-tech’. The hit to commodity prices and flatter yield curve see Energy 3.5%, Materials -2.2%, Industrials -1.6% and Financials down 3%.The net result is the S&P500 ending flat for the day while the Nasdaq index finished up 0.9%

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.