Online retail sales growth slowed in May following a fairly strong April

Insight

The FOMC was on hold as expected. Yields are lower, though most of the moves came ahead of the Fed with soft US data.

Events round-up

NZ: LCI pvt wages x overtime (q/q%), Q3: 0.8 vs. 1.0 exp.

NZ: Employment (q/q%), Q3: -0.2 vs. 0.4 exp.

NZ: Unemployment rate (%), Q3: 3.9 vs. 3.9 exp.

AU: Building approvals (m/m%), Sep: -4.6 vs. 2.5 exp.

CH: Caixin PMI manufacturing, Oct: 49.5 vs. 50.8 exp.

US: ADP employment change (k), Oct: 113 vs. 150 exp.

US; JOLTS job openings (m), Sep: 9.55 vs. 9.40 exp.

US: ISM manufacturing, Oct: 46.7 vs. 49.0 exp.

US: FOMC policy rate (upper bd%), Nov: 5.5 vs. 5.5 exp.

The FOMC was on hold as expected, with only minor changes to the post-meeting statement.

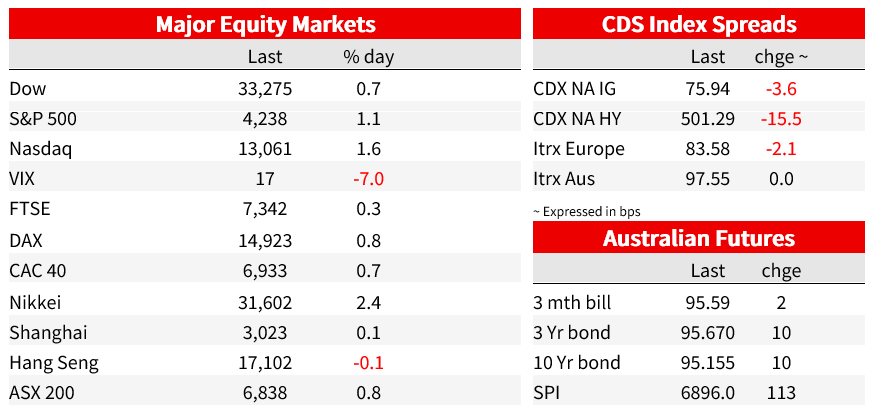

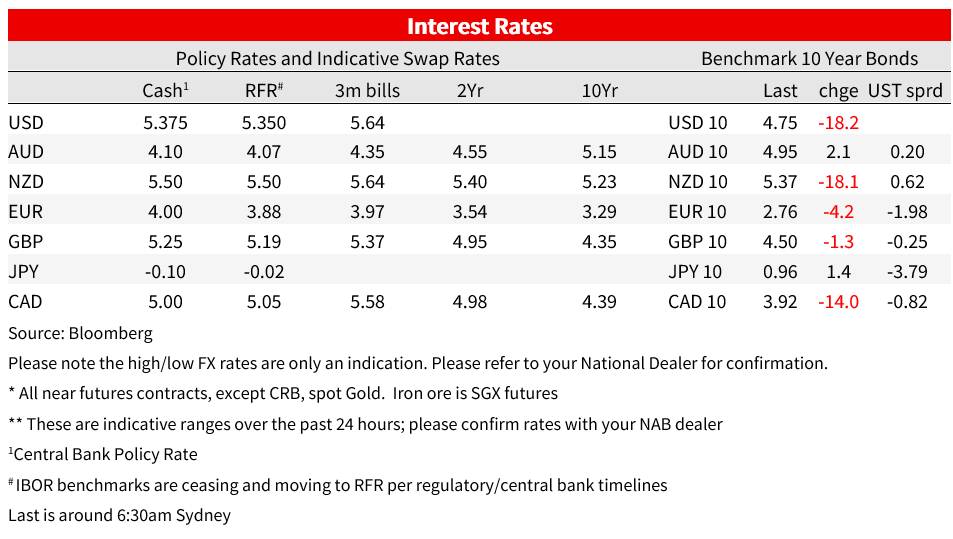

Equities are higher, extending gains towards the end of the session following the Fed. US yields were lower heading into the meeting, after the quarterly refunding announcements and alongside a soft US Manufacturing ISM. Following the FOMC, the US yields slipped a little further. The 2yr was 14bp lower on the day to 4.95%, while the 10yr was 18bp lower at 4.75%. The S&P500 gained 1.1%, and the Nasdaq was 1.6% higher, with equities moving higher towards the end of the session. Gains were led by IT and Communication Services.

The FOMC held rates steady as expected. The post-meeting statement saw two only minor changes: ‘solid’ growth was upgraded to ‘strong’, and there was some acknowledgement of higher longer-end yields, with tighter financial conditions mentioned alongside tighter credit conditions. In the Q&A, Powell said the FOMC is ‘proceeding carefully’ and that evidence of above potential growth could warrant a hike. He also said that the FOMC was attentive to the increase in longer term yields, but agreed with a questioner that tighter conditions are not yet sufficient to ‘finish the job.’ Powell said the FOMC was monitoring geopolitics for economic implications, (this didn’t make it into the post-meeting statement). Powell was clear that the Committee was not thinking or talking about rate cuts, adding that the question is ‘should we hike more.’ The OIS curve has shifted lower with only 3.5bps of tightening priced for December and a cumulative 90bps of cuts for next year versus 82bps priced before the decision and press conference.

Ahead of the Fed meeting, the 2-year rate was down 6bps on the day, with falls of 12bps for the 10-year and 30-year rates. The 10-year rate fell to as low as 4.78%, before nudging back up to 4.81% ahead of the Fed. The move lower in yields came in the context of the quarterly refunding announcement and a weak ISM report . The US Treasury said it would pare back the rise in longer dated issuance and increasing in the front end due to the rise in term premium and strong demand for treasury bills. Next week the Treasury will sell $112b of debt, less than estimates for $114b. The US Manufacturing ISM disappointed at 46.7 from 49.0, and against expectations for 49.0. Both the employment and new orders subindices fell. Also of note was mixed US labour market data (see below).

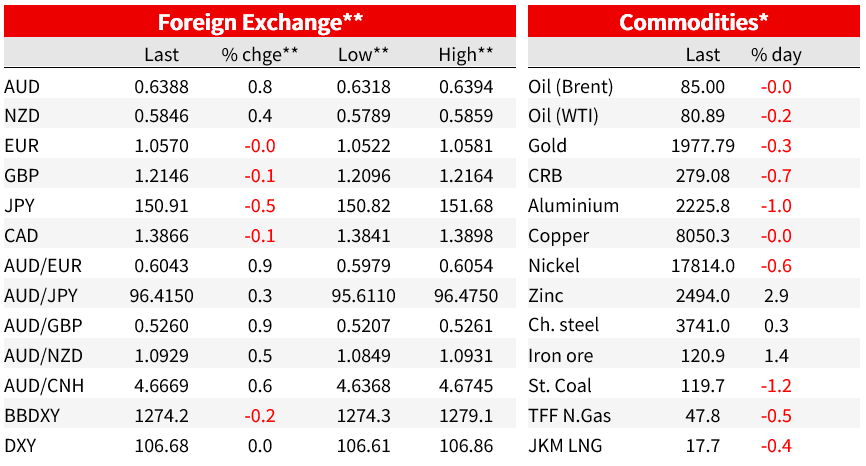

Yields were generally lower alongside Powell’s remarks, 2yr yields down another 7bp to 4.94%, down 14bp on the day and the 10yr yield slipping to 4.75% down 5bp from before the Fed announcement and 18bp lower on the day. Equities extended gains, and the US dollar retraced earlier strength to be back near flat on the day. The DXY was little changed at 106.68, eking very small gains against euro and GBP as it lost ground against the Aussie and the JPY. The AUD is the outperformer, up 0.8% to 0.6387, having touched an intraday high just below 64c at 0.6399.

Yesterday, Japan’s MoF ramped up some verbal intervention on the yen, after the BoJ’s still ultra-easy policy stance invited further weakness in the currency. Japan’s top currency official said “we’re very concerned about one-sided, sudden moves in currencies…we’re on standby ”. Japan’s 10-year rate rose to a fresh cycle high of 0.97% before edging lower after the BoJ announced an unscheduled bond-purchase operation in response to the higher yield. The BoJ and MoF’s actions continue to work against each other, but the backdrop of lower global rates worked in the yen’s favour. The yen is stronger, up 0.6%, with USDJPY falling to 150.82.

NZ labour market data were weaker than expected, with a 0.2% fall in employment in Q3 driving a 0.3 percentage point lift in the unemployment rate to 3.9%, its highest level in more than two years. Labour market tightness was abating and leading to weaker private sector wage inflation, supportive of the view the RBNZ will not be pushed to tighten further.

US labour market data was mixed . ADP private payrolls rose by 113k in October, less than the 150k expected by the consensus. The series has been a poor indicator of non-farm payrolls, released Friday and where consensus is for 180k. Job openings increased 56k to 9.55m from a downwardly revised August, though were a little above the 9.4mn expected. The ratio of job openings to unemployed was steady at 1.5, well down form the peak of 2 but remaining above prepandemic levels near 1.2. In contrast, the quits rate held steady at 2.3%, in line with pre-pandemic levels, and the hiring rate held at 3.7%, a little below its 2019 average. On those flow-based metrics, the labour market doesn’t overly look tight. In the Q&A, Powell said that labour demand still exceeded the supply of available workers.

Coming Up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.