NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

In what have been predictably quiet bond and equity markets ahead of US payrolls tonight, currencies are continuing to enjoy their week in the sun.

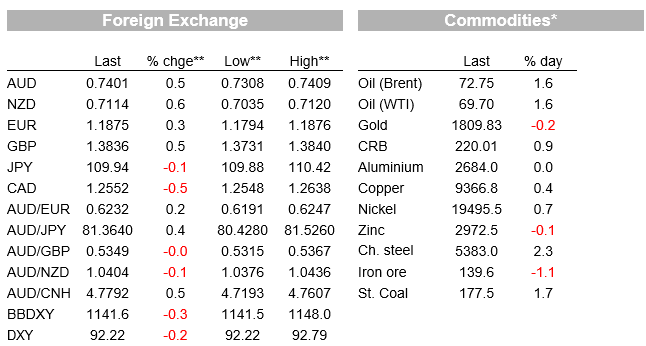

In what have been predictably quiet bond and equity markets ahead of US payrolls tonight, currencies are continuing to enjoy their week in the sun, AUD/USD poking above 0.7400 for the first time in a month and NZD above 0.7100 for the first time in over two months. The USD is at a four week low.

One of the more keenly anticipated US employment reports awaits tonight – as it has been since Monday – and where in the wake of Wednesday’s much weaker than expected ADP employment report (374k) the whisper number will be a fair bit softer than the Bloomberg survey median of 725k, polled prior to this week’s data, as unreliable as ADP (as one lead indicator) is as a guide to private sector non-farm payroll employment. A strong report in line with the prior two months puts the market on the scent of a September FOMC QE tapering announcement (November currently the more favoured month). Numbers much softer than June and July will kicks expectations into the (slightly) longer grass.

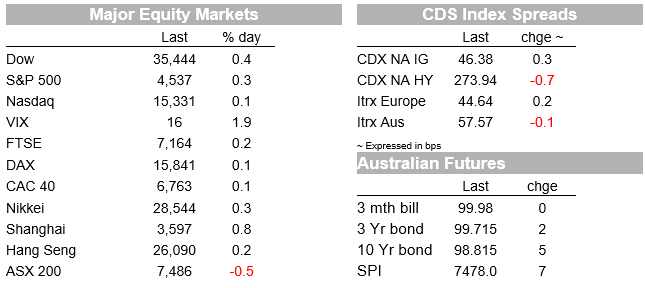

Were it not for a 2.5% jump in the energy sub-sector, the S&P 500 would almost certainly have finished just in the red rather than just in the green (+0.25%, with the NASDAQ +0.1% and the Russell 2000 up 0.6%). Oil related stocks are higher with oil prices, as 94% of Gulf of Mexico crude production remains shut even though the storms created by Hurricane Ida have left the area. The oil market has also taken the agreement this week by OPEC and friends to lift production from October comfortably in its stride being very much ‘as expected’. WTI and Brent crudes are both up 1.7%, to $69.72 and $72.79 respectively. Other commodity markets are mixed with base metals mostly higher (including copper and aluminium), iron ore futures mixed – down 0.5% on the Dalian exchange night session but up 0.8% on the SGX – while gold is unchanged at $1,810 an a ounce.

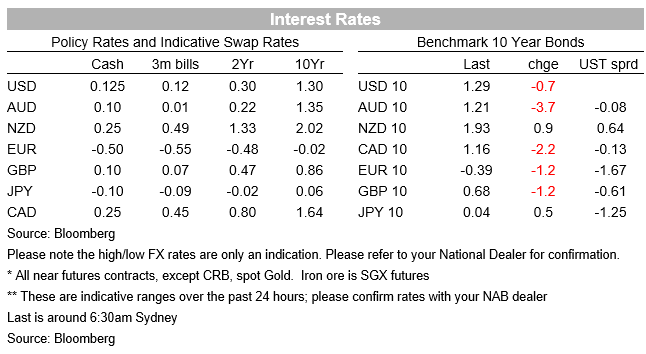

Nothing to note in bond markets with 10-year Treasury yields down less than 1bp to 1.285% and the 2-year note flat at 0.21%. Veteran bond investor Bill Gross’ comments that Treasury bonds belong in the “investment garbage can” haven’t impressed anyone other than financial news headline writers particularly desperate for a story ahead of tonight’s payrolls data. European bond yields have given back a little more of their mid-week spurt higher but with the exception of Italy (-1.8bps) yield at 10 years are mostly less than 1bp down on the day.

Economic data overnight has been confined to weekly jobless claims which fell to a new post pandemic low of 345k from 354k last week, though more symptomatic of business reluctant to let employees go, given the likely difficulty of replacing them down the track, that the current pace of hiring. There were some minor revisions to Durable Goods Orders within the overall Factory Goods Orders numbers (latter +0.4% against 0.3% expected and ex-transport 0.8%, above the 0.5% consensus).

Yesterday in Australia, the trade surplus came in at a record high of $12.1bn for July, a couple of billion dollars better than expected, driven by a further increase in goods exports (+6% m/m to $41.3bn and led by higher iron ore values). Meanwhile new housing loan approvals rose 0.2% m/m in June against expectations for a 0.2% fall. A 1.8% rise in investor loan approvals was partially offset by a 0.4% fall in owner occupier approvals and where the share of first-home buyer approvals continues to fall post the end of the HomeBuilder fist-home buyer scheme . Investor loan commitments have seen monthly growth each month since October 2020 to be close to double their value a year ago. However, although it has increased recently, as a share of total loan approvals, investor loans remain below their long run average at just 29.1%.

So the FX market story is really one of further slippage in the USD off its 20 August year to date high, the DXY index now 1.6% lower since then, 1% of which has been since Fed chair Powell’s Jackson Hole address last Friday. Also supporting losses has been improving sentiment toward fuller global economic re-opening as vaccine roll-outs proceed apace in many countries. As one example, the MSCI World Hotels, Restaurants and Leisure index is now up over 5% since 20 August (the day the USD peaked).

The fact commodity currencies are leading the push higher in all major currencies is no surprise in so far as they were the ones suffering the most when the USD was in the ascendancy. NZD and NOK are both finishing the New York day up 0.6%, the normally flightless bird to a high of 0.7120, its best level since 16 June. The AUD’s recovery off its 0.7106 August 20 low continues, AUD/USD up another 0.5% in the last 24 hours to a high of 0.7409 (best since 5 August). AUD has, with the exception of the AUD/NZD, now recouped more than half – and in the case of AUD/CAD all – of the losses it suffered in the 1 July – 20 August period when it was the world’s worst performing major currency.

Finally a couple of COVID-19 news snippets the caught your scribes eye this morning, both courtesy of the Financial Times. Italy may eventually mandate Covid-19 vaccinations for all eligible citizens. Prime minister Mario Draghi said during a press conference yesterday that all Italians may be required to be vaccinated when EU health authorities give full approval to the vaccine. So far the European Medicines Agency (EMA) has granted conditional approval to four vaccines.

And second, the rollout of Covid-19 vaccines in England has prevented an estimated 143,600 hospital admissions, 24m infections and 105,000 deaths, figures from Public Health England show. Previous estimates put the number of hospital admissions averted at 82,100. PHE said vaccine effectiveness estimates used in its modelling were updated this week. The roughly 143,600 admissions averted, which PHE said was likely to be an underestimate, are all among people aged 65 years and over.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.