Economic and financial market update

Insight

Banking sector turmoil is back to the fore driving all markets, today centred on Credit Suisse.

Financial instability centred on the banking system is back firmly to the fore overnight, Credit Suisse currently at the centre of the storm, its stock ending the European day some 24% down at CHF1.6970. This comes after the firm’s auditor on Tuesday morning disclosed “material weaknesses” in the bank’s financial reporting controls, and then on Wednesday the chair of its largest shareholder, the Saudi National Bank, asked whether he was open to providing more capital to Credit Suisse if there was a call for additional funding, reportedly replied “absolutely not”.

Bloomberg has since reported that bank leaders and government officials have held talks about options including a public statement of support and a potential liquidity backstop. Also amongst ideas being floated, Bloomberg says, are a separation of the bank’s Swiss unit and a ‘long shot’ tie up with larger Swiss rival UBS. In the last.

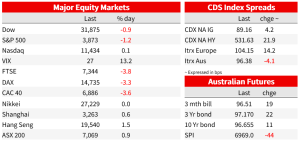

And just in the hour, the SNB has said it will provide liquidity to Credit Suisse ‘if necessary’. The earlier Bloomberg report (out soon after 5:00 AEDT) had some impact in stabilising stock markets. Europe was already shut for the day (Eurostoxx 50 -3.5%) but the S&P500 rallied from around 3,860 to 3.895 on the news (about 0.9%) – gains which were holding with an hour of NYSE trade still to come.

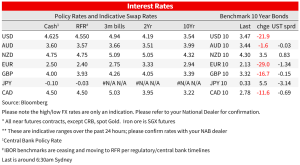

Compared to where we were sitting this time yesterday, doubts about the efficacy of central bank tightening in the teeth of a financial stability storm have shown up in market pricing for the Fed next week coming it to 13bps of tightening from 19bps on Tuesday, and for the ECB tonight from 43bps (and 49bps before the SVB news) to just 28bps.

In bond markets, 10-year Treasuries are currently 9.5bps down on the day at 3.49% and 2s a full 33bps to 3.92%. earlier Wednesday, French and German 2year yields ended down almost 50bps and 10s down 25-30bps.3-year Australian bond futures see the implied yield almost 20bps down on Wednesday’s local close.

Economic news is back playing second fiddle to banking sector travails, but the US producer price data in particular were nonetheless important. On the heels of Tuesday’s CPI report which failed to provide much support for the US disinflation story, PPI has gone a long way to doing just that. Headline (final demand) undershot expectations coming in at -0.1% against 0.3% expected with the core (ex-food and energy) reading also 0.4% lower than expected at unchanged on the month. The latter brings core annual PPI down to 4.4%, after January was revised sharply lower to 5.0% from 5.4% originally reported. As our friends at Pantheon Economics note, after producer margin expansion had a big hand in driving inflation higher in 2021-2022 margin compression is now doing the opposite, at least to non-wage related inflation. They see much more to come in this respect.

On the other side of the US economic ledger, the adage about ‘give ‘em the money and they’ll spend it’; continues to ring true for US consumers, with the so-called ‘control group’ Retail Sales up 0.5% on the month against a 0.3% fall expected. Headline sales at -0.4% on the month and ex-autos at -0.1% were both in line with consensus forecast, a payback for strong January auto sales the main driver of the former. Also of note, the NAHB Index of homebuilders sentiment lifted to 44 from 42 against a fall to 40 expected (in which respect we’d note the lack of existing home supply on the market as a possible driver, given that anyone selling and buying another home would have to refinance their (30-year) mortgages at sharply higher rates). Also, the (New York state) Empire manufacturing survey fell to -24.6 from -5.8, well beneath the -7.9 expected and meaning no uplift from earlier strength in China’s manufacturing PMI as has historically been the case.

Somewhat (completely) lost in the market melee but in any event a low-key affair by past standards (not least the quickly aborted Truss-Kwarteng one) the UK Annual Budget handed down by chancellor Hunt includes new government forecasts claiming the UK will not now enter a technical recession this year and that inflation will fall to 2.9% by end-2023 (a bit below the BoE’s 3-4%). As expected, the £2500 energy price guarantee will be extended for a further three months through July (after which bills will fall as a result of lower prices) and Chancellor Hunt also confirmed fuel duties will be frozen.

The UK government will carry on with its plan to raise corporation tax from 19% to 25% in April (a policy than has been slammed by business, though is still below Germany, France and Japan). And, as the so-called ‘super-deduction’ plan is also set to expire, a new policy was unveiled of full capital expensing. This means every £1 invested by business will be able to be deducted from taxable profits (for at least three years).

Yesterday’s slew of China activity data covering January and February offered a mixed picture, with industrial production a little on the soft side (2.4% YTD y/y against 2.6% expected, Fixed asset Investment on the high side (5.5%vs 4.5% expected) and Retail sales bang in line (3.5%).

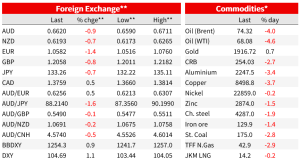

In currencies, after a small post-China data lift, AUD has since been a victim of the icy ‘risk-off’ sentiment blasting though markets, but it is European currencies bearing the brunt of this, unsurprisingly given Credit Suisse is currently at the epicentre of the storm. AUD/USD is down almost 1.0% on Tuesday’s NY close (to ~0.6620) compared to losses of 1.5-2.0% for EUR, CHF (no safe haven demand here for once) and NOK. The latter is faring the worst of any G10 currency, thanks to a 4% plunge in oil prices. This in conjunction with more confident assessments of imminent recession (in the US at least) but with losses reported compounded by technically driven selling (the stronger USD won’t have helped either). Gold is up $12 or 0.7% to $1,916 as I type.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Economic and financial market update

Insight

Online retail sales growth slowed in March

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.