We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

The Fed will not see the need to act swiftly after Friday’s payrolls numbers, but it will be a different story for thew RBA tomorrow. NAB’s Tapas Strickland says, given the improvements in the Australian economy, the need to run QE at $100 billion every six months is not there anymore.

https://soundcloud.com/user-291029717/markets-going-nowhere-yet-us-job-openings-boom-1

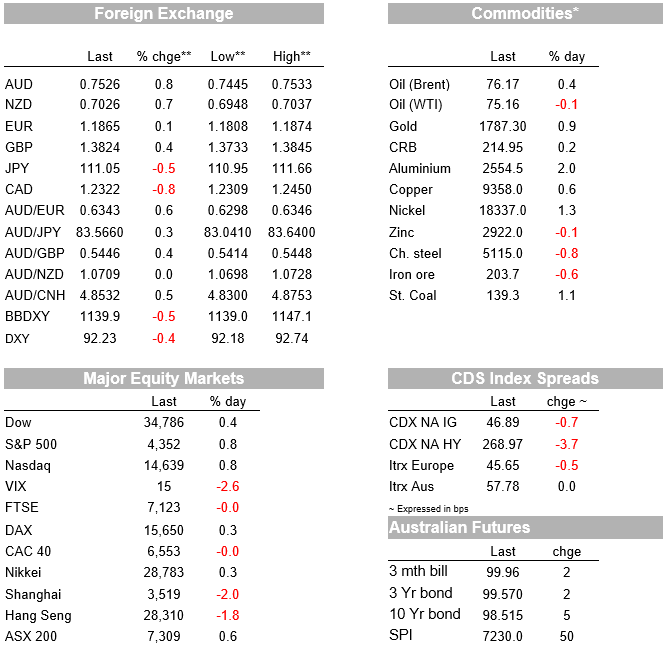

Another ‘goldilocks’ payrolls report came and went with yields lower (US 10yr -3.4bps to 1.42%), equities higher (S&P500 +0.8%) and the USD lower (BBDXY -0.5%). While headline payrolls did beat expectations by a considerable way (850k v. 720k expected), the unemployment rate rose (5.9% v. 5.6% expected) and 40% of jobs gains was led by the leisure and hospitality industry. Overall the level of payrolls is still 6.8m below pre-pandemic February 2020 levels and is still below the level of substantial progress needed by the Fed. As such there is nothing in this report for the Fed to become hawkish about. Commodities also rose with the risk on tone with aluminium +2.0% and copper +0.6%. Brent oil though was more steady at +0.4% with OPEC not able to decide on whether to extend production cuts – officials meet again today. This week’s focus will be on the much anticipated RBA meeting (see below for details), the FOMC Minutes for taper hints, and an ECB strategic framework meeting where expectations are the ECB will move closer to a symmetrical 2% inflation target.

First to Payrolls. Headline jobs for June was 850k, well above the 720k consensus and well up on the 583k last month. The gains to date though still leave the level of payrolls 6.8m below pre-pandemic February 2020 levels (or 4.4%) and at June’s pace it would take 8 months to get back to the pre-pandemic level of payrolls. Leisure and hospitality led gains, accounting for some 40% of jobs in the month, while government hiring was also very strong. It is worth noting that even with the strong gains in leisure and hospitality there are still 2.2m fewer jobs in this sector compared to February 2020. The goldilocks bit of this report was the unemployment rate which rose (not fell) to 5.9% from 5.8% against expectations for a fall to 5.6%, while earnings was in line with expectations at 3.6% y/y.

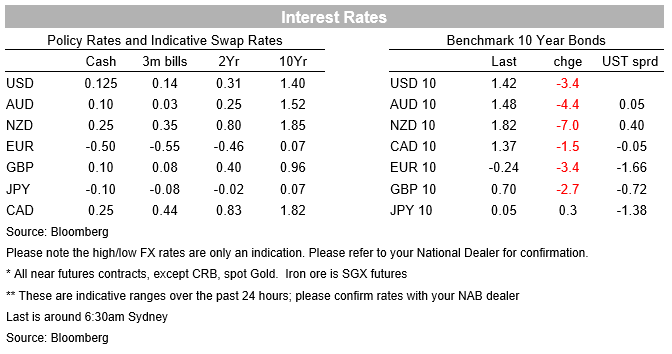

As for Fed implications, the goldilocks print suggests there is no need to accelerate the tapering timeline or the implied rate hike profile. A September taper announcement with actual tapering in Q4 still looks like a good bet. The Fed’s Harker late last week nominated tapering by $10bn a month, which would mean a full 12 month taper and reduce the chances of a 2022 rate hike given the Fed would not want to be hiking and tapering at the same time. Of course that tapering amount could be changed depending on the flow of data. The goldilocks report has also got some thinking that a taper more heavily weighted initially to MBS might be more appropriate and we would expect more Fed speak along this path. First up from the Fed to speak post payrolls will be Bostic on Wednesday, who only recently turned hawkish arguing for tapering and pencilling in a 2022 hike.

Yields fell in the wake of the payrolls report after the initial reaction subsided. The US 10yr fell -3.4 bps to 1.42% and for the week it is down some 10bps. The 30-year yield also fell 2 bps to 2.04% and is also done some 11bps for the week. With the a 2022 hike not being supported by the data, the 2-year yield eased 2bps to 0.24%, though markets continue to price the first Fed hike by December 2022. With the longer end rallying more, the curve flattened further over the past week with 5s30s -4.4bps to 118bps. The global bond rally was also seen across the pond with the German 10yr yield -3.4bps -0.24%. The ECB’s mooted strategy review meeting to be held this week is likely to keep the ECB dovish with expectations the ECB will move closer towards a symmetrical 2% target.

As for FX, the USD fell in line with yields and the risk-on tone with the USD (BBDXY) -0.5%. Commodity currencies outperformed after having underperformed against recent USD strength. The AUD rose 0.8%, NZD up by 0.7% and the USD/CAD was -0.8%. The EUR lagged the USD weakness up just 0.1%, while USD/Yen reversed some of its recent rise to be down 0.5% to 111.05. For the week the USD is up 0.4%. All focus for the AUD will be on the RBA on Tuesday and whether the RBA pushes back on market pricing which prices in a rate hike as early as November 2022 against the RBA’s most recent guidance of not until at least 2024 (more details below).

The highly anticipated RBA meeting on Tuesday dominates the week domestically. Governor Lowe is also holding a rare post-meeting press conference on “Today’s Monetary Policy Decision” (with Q&A), stoking expectations of a significant policy turn given the last post-meeting speech was in November 2020 when the RBA announced its QE program (see November 2020 speech ). At this meeting the RBA has foreshadowed it will be deciding on whether to roll its 3yr YCC Target from the April 2024 bond to the November 2024 bond, and also decide how it will calibrate its ongoing QE program. The meeting is also taking place while Sydney is in lockdown due to the Delta variant, illustrating that Australia remains vulnerable to outbreaks until vaccination rates lift sufficiently to 75-80%. Until that occurs snap lockdowns remain a risk to the outlook.

NAB’s view is the RBA will not extend its 3yr YCC target and we also expect QE to be tapered to $75bn for another six months. The consensus is also for YCC not to be extended, but for QE to be open ended on a weekly schedule, rather than for a defined window. Since a decision to not roll YCC effectively pivots the RBA to outcomes-based forward guidance (and away from calendar based guidance), there will be lots of interest on when the RBA expects to hike rates. We expect Governor Lowe to remain dovish and push back on market pricing which prices a hike as early as November 2022. Dr Lowe could push back by maintaining the conditions for a rate hike being “unlikely to be until 2024 at the earliest ”. Another speech pencilled in for Thursday titled “The Labour Market and Monetary Policy” also hints he could emphasise the RBA’s new maximum employment framework, where the RBA is going to wait until inflation is sustainably within the 2-3% band before hiking, rather than hiking on a pre-conceived notion of where NAIRU is.

Internationally it is a quiet week. The main data points to watch for are the FOMC Minutes on Wednesday and soundings from an ECB meeting that is likely to wrap up the ECB’s strategy review. For the ECB, a formal sift to a more symmetrical 2% inflation target is looking likely at this stage. Meanwhile the FOMC Minutes will be scrutinised closely for taper discussion, particularly if the possible pace and MBS v. Treasuries was discussed. Note the Fed’s Harker last week suggested tapering by $10bn a month which would mean a year-long taper schedule. China also has some top tier data including CPI/PPI on Friday and Aggregate Financing figures anytime from Friday.

Domestically we have Building Approvals and a final-read on Retail Sales. Neither are likely to be market moving ahead of the RBA on Tuesday (see above for details). Internationally it is very quiet with the US out on the Independence Day Public Holiday, while datawise there is only the final Services PMIs.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.