Economic and financial market update

Insight

Today’s podcast Overview Rumours of inflation’s demise much exaggerated US CPI shocks to the upside: stocks, bonds take fright USD bounces back, AUD and NZD both down by more than 2% Next week’s Fed debate now seen to be between 75 and 100bps (83bps priced) German ZEW survey readings slumps while US NFIB Business Optimism […]

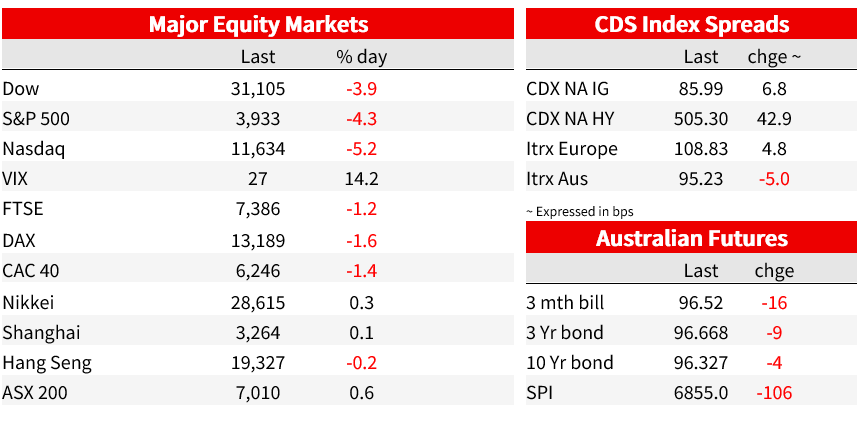

Rising expectations in the build up to last night’s US CPI inflation figures that not just headline but underlying inafltion will, if not now then very soon, be heading back down, have proved to be a figment of the market’s imagination. Core August CPI up 0.6% on the month for 6.3% y/y up from 5.9% in July has exacted very heavy tolls on markets, the NASDAQ off more than 5%, US 2-year note yields up as much as 29bps at one point (+18bps now) and the DXY index up 1.5% with AUD and NZD both down 2 ¼% on the day, AUD/USD back to the low 0.67s.

The combination of some positive developments in Ukraine either side of last weekend in terms of Ukraine forces recapturing parts of Russian occupied territory, news of European government plans to greatly soften the energy price blow being inflicted on households and hence the broader economy, plus various anecdotal reports of falling prices in the United States, had been seeing risk markets develop a head of steam and put the US dollar under the cosh. The narrative has suffered a rude awakening overnight, if only (so far) on one front. Market reactions have been dramatic

US Core CPI, instead of rising by an expected 0.3%, jumped by 0.6% to see the annual rise lift to 6.3% from 5.9% (vs the 6.1% consensus) and while headline CPI fell back to 8.3% from 8.6%, this compared to an expected drop to 8.1%. The Cleveland Fed’s trimmed mean inflation measure meanwhile and too the Atlanta Fed’s ‘sticky CPI’ index, both rose in annual terms, to 7.7%.

What is perhaps most disconcerting in all this is that the strength in core inflation is very much service sector led (items such as vehicle repairs, dental and hospital services), categories which are primarily driven by wage inflation. There will therefore be as, or almost as much, focus on incoming Average Hourly Earnings (and the unemployment rate) in forthcoming US employment reports as there will in the next set(s) of CPI figures.

Still on the wages subject, yesterday’s UK labour market data, as well as showing the unemployment rate dropping from 3.8% to 3.6%, saw Average Weekly Earnings on a 3-month yr/yr (ex-bonus) basis rise to 5.2% from 4.7%. Whatever magic wand the UK government is about to wave over household utility bills to bring headline UK inflation smartly down on what it otherwise would have been, the wages numbers will be troubling to the Bank of England when it holds its one-week delayed MPC meeting next week.

And as for inflation down here, yesterday’s NAB Business Survey, alongside positive reading on Conditions (+20 from 19) and Confidence (up to 10 from 8) hint that Q3 CPI could print as high as 2.0% q/q based on mapping from the various wage costs and price components of the survey. See yesterday’s Australian Markets Weekly for much more on this.

Finally on the incoming economic data front, last night’s US NFIB (Small Business) optimism survey showed a rise, to 91.8 from 89.9 (better than expected) and the German ZEW readings falling by much more than expected (Current Situation slumping to -60.5 from -47.6, and Expectations to -61.9 from -55.3). A shift in relative US/European economic performance is currently nowhere in sight

To markets , and in equities, the NASDAQ has ended the day down 5.2% and the S&P500 down 4.3%, losses for the S&P led by IT (-5.4%) Consumer Discretionaries (-5.2%) and Communications Services (-5.6%). Apple and Microsoft suffered their biggest one-day losses in a year. That’s the spectre of still higher interest rates for you and where the US money market has moved to price 83bps of tightening from the Fed next week, CPI shattering any illusion that next week’s decision could yet be between +50bps and +75bps. January 2023 Fed Funds futures now show an implied rate above 4% (4.04%) for the first time, up from 3.83% pre-CPI.

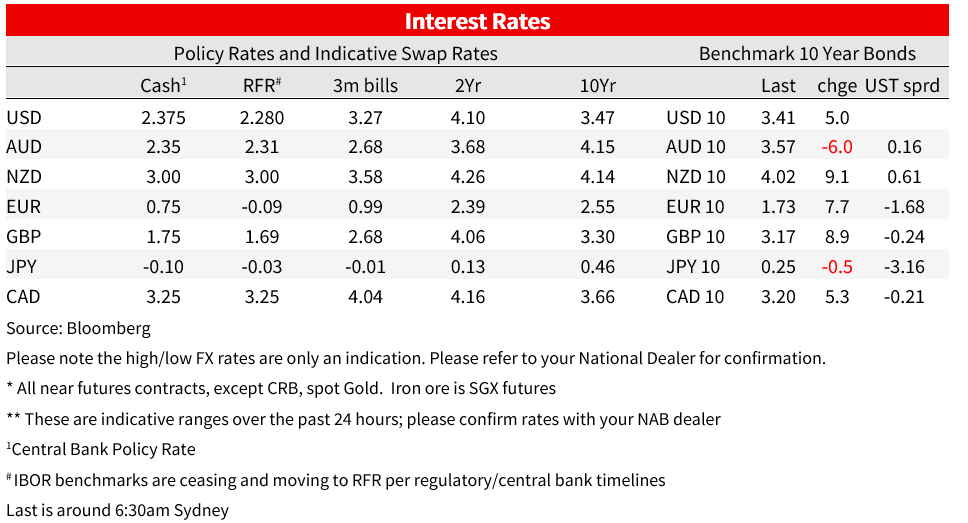

Bond markets see the 2-year Treasury note +18.5bps to 3.76% and 10s +5bps on the day to 3.41%, so taking curve inversion back out to -35bps (still above its most extreme in the cycle nearer -50bps a month ago). In Europe, 10-year Bund yields finished their day 7.5bps higher and UK gilts +9bps.

The FX market has seen a dramatic reversal in many of the moves witnessed since the middle of last week, no more so that in AUD and NZD, both 2.25% down on Monday’s New York close. NZD has (just) fallen back below 0.60 (0.5995 as of now) and AUD/USD to lows of around 0.6730, also where it is now. In EM FX, of note is that USD/CNH, having risen to within kissing distance of 7.0 to as low as 6.91 in recent days, is now back above 6.98. USD/JPY is rapidly reapproaching last Wednesday’s Y145 high. No pressure on the BoJ next week then. The DXY USD index has finished in New York +1.5% on the day. That’s some ‘outside day’ for the market technicians to ponder, as well as marking a more than 61.8% retracement of the fall since last Wednesday’s new 20+ year high.

Coming Up

Economic and financial market update

Insight

Online retail sales growth slowed in March

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.