NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

The lack of a starting QE gun alongside a strong message that there is a stricter test for rate hikes compare to QE tapering resulted in a risk positive reaction to the much-awaited Fed Chair Powell’s Jackson Hole speech on Friday. A QE tapering decision remains live, although now November looks more likely than September.

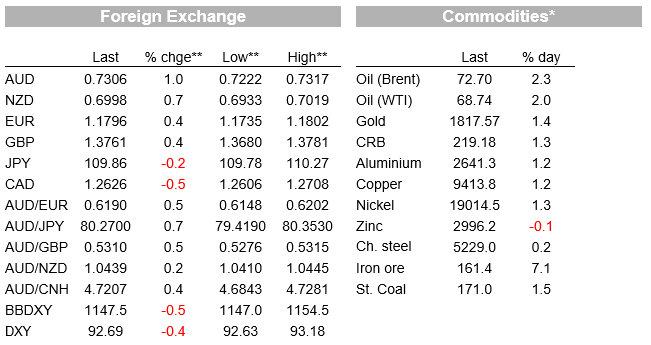

The lack of a starting QE gun alongside a strong message that there is a stricter test for rate hikes compare to QE tapering resulted in a risk positive reaction to the much-awaited Fed Chair Powell’s Jackson Hole speech on Friday. A QE tapering decision remains live, although now November looks more likely than September. US and EU equities recorded a positive end to the week, the USD was softer across the board with pro-growth currencies such as the AUD and NZD at the top of the leader board. AUD starts the new week with a 73c handle while NZD is testing 70c. The five-year part of the curve led Friday’s declines in the UST curve, but on the week the curve retained steepening bias. Oil and iron ore were the clear commodities winners on Friday and the week.

As widely expected, Fed Chair Powell’s Jackson Hole speech did not provide a definitive answer the QE tapering decision, but his dovish undertones on his views on inflation as well as the emphasis on decoupling the rate hike decision from QE tapering resulted in a risk positive market reaction . Consistent with his messaging from the July FOMC, Powell’s signalled the Fed could begin QE tapering in coming months with the incoming labour data and Delta dynamics determining the exact date. On this score, the Fed Chair acknowledged the strong July employment report for July, but balanced it against his concerns over the spread of the Delta variant.

This means Friday’s August nonfarm payrolls (see more below) will be important in framing tapering expectations and perhaps some reflections on Delta impacts . Last week’s Markit US PMI surveys for August noted the Delta variant had led to difficulties in hiring new staff, staffing levels rising at the slowest rate since July 2020, with only a marginal increase. A strong payrolls print (market expecting 750k) could instigate a debate for a September tapering start, but our sense is that in October the FOMC is likely to have a better sense of the state of the labour market following the end of the unemployment benefit closing in September, kids back at school as well as the impact from delta infections on the labour market.

On inflation, Powell reiterated that he still expects the inflation surge to prove temporary . He pointed to high inflation being narrowly confined to some specific sectors, such as car prices, which should see prices moderate in time as supply catches up, that there was little evidence of inflation pressures feeding through into wages at this stage, inflation expectations were anchored and global disinflationary forces weren’t going away anytime soon. Using history as a guide, the Fed Chair also noted that the that stabilisation policy in the 1950s had taught monetary policy makers not to attempt to offset what are likely to be temporary fluctuations in inflation . “Responding may do more harm than good”, given the policy influence may take after a lag of one year or more, by which time the need for that policy may well have passed.

Finally, and perhaps ultimately more important for market, Fed Chair Powell made a strong case at delinking the tapering decision from the rate hike one. Powell stressed that the criteria for rate hikes represented a “substantially more stringent test”, adding that tapering was not intended to provide a “direct signal regarding the timing of interest rate liftoff.” The Maximum employment goal is about achieving and sustaining a strong jobs market to win life-changing gains for marginalised groups and we are still a long way from that. Markets responded by reducing Fed rate hike expectations for late-2022 and 2023 by around 3bps. The first Fed hike is now fully priced by around March 2023.

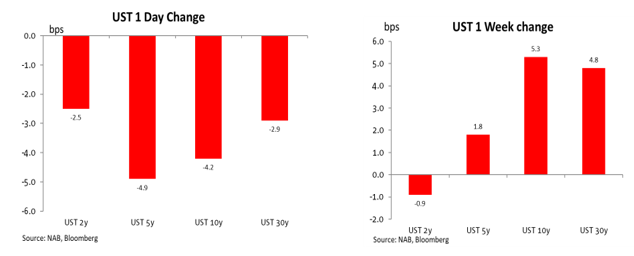

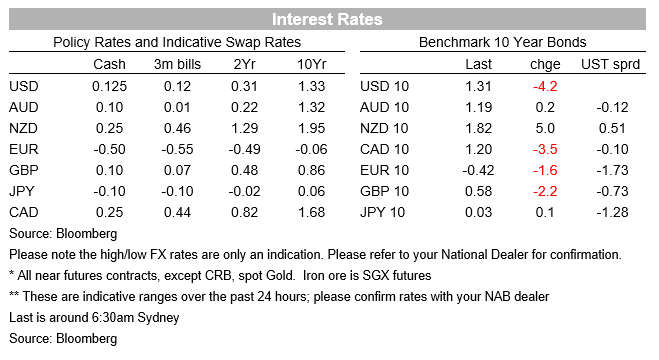

Looking at the US Treasury curve, the five-year part of the curve led the decline in yields on Friday, down -4.9bps to 0.80% on Friday while the 10y Note declined 4.2bps to 1.3070%. That said on the week the UST curve retained a steepening bias with the 10y and 30y tenors up around 5bps on the week while the 2y rate fell by 1bps to 0.217%.

UST yields changes on Friday and the week

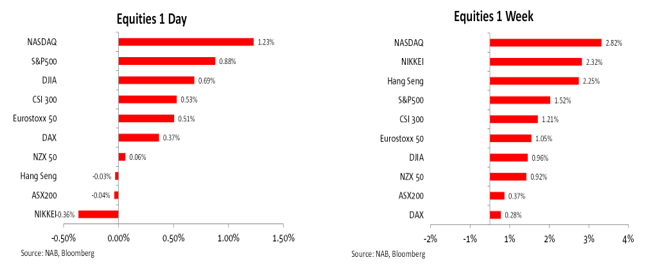

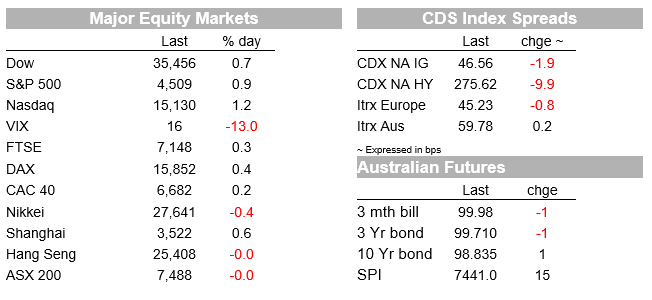

The dovish undertones from Powell speech’s was a music to the equity markets’ ears, QE tapering is coming soon, but the punch bowl will remain stimulated with no rate hikes within sight. The NASDAQ led the rise in US equities, ending the day +1.23 while the S&P 500 closed +0.88%. European equities also recorded gains on Friday although they were more modest in nature mostly between 0.3% and 0.5%. Looking at the week, the NASDAQ (+2.82%) managed to pip the Nikkei for the top spot while the Hang Seng also enjoyed a bit of a recovery, up 2.25% on the week. Germany’s DAX and our ASX 200 were the laggards with modest weekly gains of 0.28% and 0.37% respectively.

Equites performance on Friday and the week

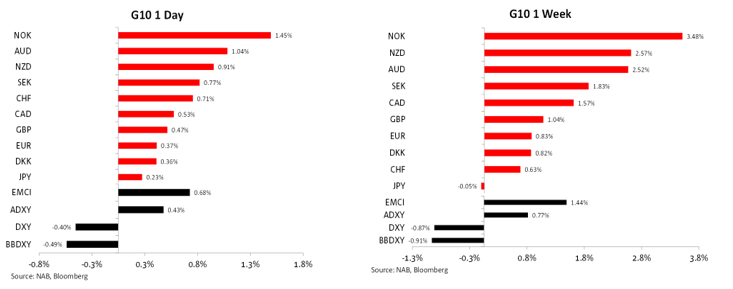

Moving on to the FX markets the broad improvement in sentiment alongside a decline in UST yields was big blow to the USD . In index terms the big dollar fell around 0.9% in BBDXY and DXY terms and was broadly weaker against G10 as well as Asia (ADXY +0.77%) and EM pairs (EMCI +1.44%). The AUD and NZD closed Friday closed to the top of the G10 leader board, up around 1% and only outperformed by NOK, up 1.45%. The AUD begins the new week with a 73c handle, looking a lot healthier than it did 10 days again when it was very close to dipping below 71c. From a technical perspective the bullish outside day reversal on Friday is very encouraging, the move above 73c also means the AUD‘s downtrend from its decline early in June may be coming to an end and the market will probably now look at the 50 day moving average at 0.7395 as the next test for confirmation the AUD recovery can extent. From a fundamental perspective we still expect the pair to embark on decent recovery over the coming months with Delta covid dynamics easing around the globe alongside an increase in vaccinations rates. This should be a positive story for the global growth recovery and commodities, all positive for the AUD.

The NZD, which was testing 0.68 only a week ago, closed Friday back above the 0.70 mark. It is now essentially back to where it was before the shock news of a community Covid-19 case on August 17th. This just goes to show that global factors remain far more influential on the NZD than local ones.

FX Friday and weekly performance

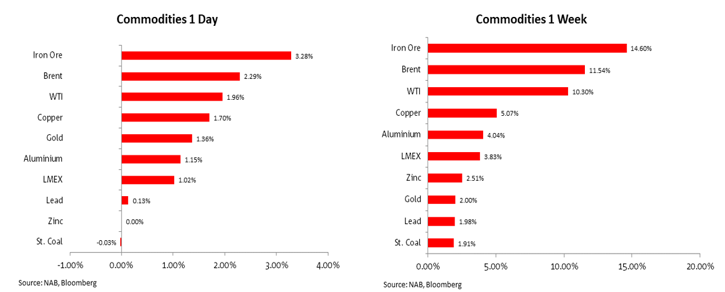

On the commodity front, worth noting that oil price were not the only ones to show decent gains on the day ( ~2.3%) and the week (~11.5%). Iron ore was the other outperformer, up 3.28% on Friday and just over 14% on the week. Metal prices and copper also had decent gains on the week up ~5% with Gold and coal up around 2% over the past five days.

Commodities Friday and weekly performance

Economic data was a sideshow given Powell’s speech and had little market impact . For the record, US personal spending was slightly weaker than expected in July (+0.3% m/m) and, given the Delta variant outbreak, consumption is likely to be much weaker in Q3 than the stimulus-fuelled surge in Q2. The final release of the University of Michigan consumer confidence index was confirmed at 70.3, a more than 13% fall from July’s level, suggesting some increased caution amongst households. The fundamentals for the US consumer still look strong though, with US household savings extremely high and the labour market strengthening. The US core PCE deflator, the Fed’s preferred inflation gauge, nudged up to 3.6% y/y, as expected, its highest level since the early 1990s. Year-on-year inflation is expected to remain extremely elevated for a few months yet before starting to ease back.

Coming Up

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.